Hello,

Markets continuously evolve. It’s what they do. They eventually outgrow the product they were initially built for. What started as a Chicago butter-and-egg exchange in 1898 became the world’s largest derivatives market (CME). Amazon started by building warehouses and payment rails to ship paperbacks. Today, the same systems don’t care what they ship. Books are probably a footnote in Amazon’s revenue now.

This pattern stays relevant today. You start by building infrastructure for one thing, discover that it works for many other things, and then you keep expanding your business to absorb everything your infrastructure can support.

Crypto exchanges are living this moment.

The infrastructure they built to trade tokens works just as well for trading crude oil, silver, equity indices, pre-IPO stocks or event contracts. Non-crypto perpetual contracts accounted for 99% of all trading volume over the past seven months on a permissionless market that didn’t exist two years ago.

You can see this market playbook happening everywhere. Every exchange is racing to become a multi-asset brokerage, and blockchain rails are providing the cheapest path to get there.

Onto the story,

Prathik

The Cheapest Path

A perpetual futures contract or a prediction market contract doesn’t care whether the underlying is bitcoin or crude oil. All you need is a stablecoin-funded wallet to buy a futures contract on a memecoin or place a bet on the outcome of Apple’s quarterly earnings. The rails are asset-agnostic. Just as the internet and logistics networks were agnostic to what was traded on Amazon’s marketplace.

But why would traders abandon their current venues to trade silver and stocks on an exchange that has barely existed for a couple of years? The same things that drove people to choose online commerce: convenience and cost savings.

Amazon cut the intermediaries and allowed distant sellers to ship directly to buyers. This enabled the sellers to undercut their competitors by offering subsidised prices. It also allowed buyers to browse a host of options, add items to their shopping carts, and make payments from the comfort of their homes (or anywhere else).

Although the cost advantage that blockchains offer was originally built for crypto transactions, it applies equally to equities settlement, commodity clearing and cross-border stock access.

The 24/7 live markets on the blockchain also allow traders around the globe to price events at any time. We saw their impact on non-crypto assets multiple times in the past few months.

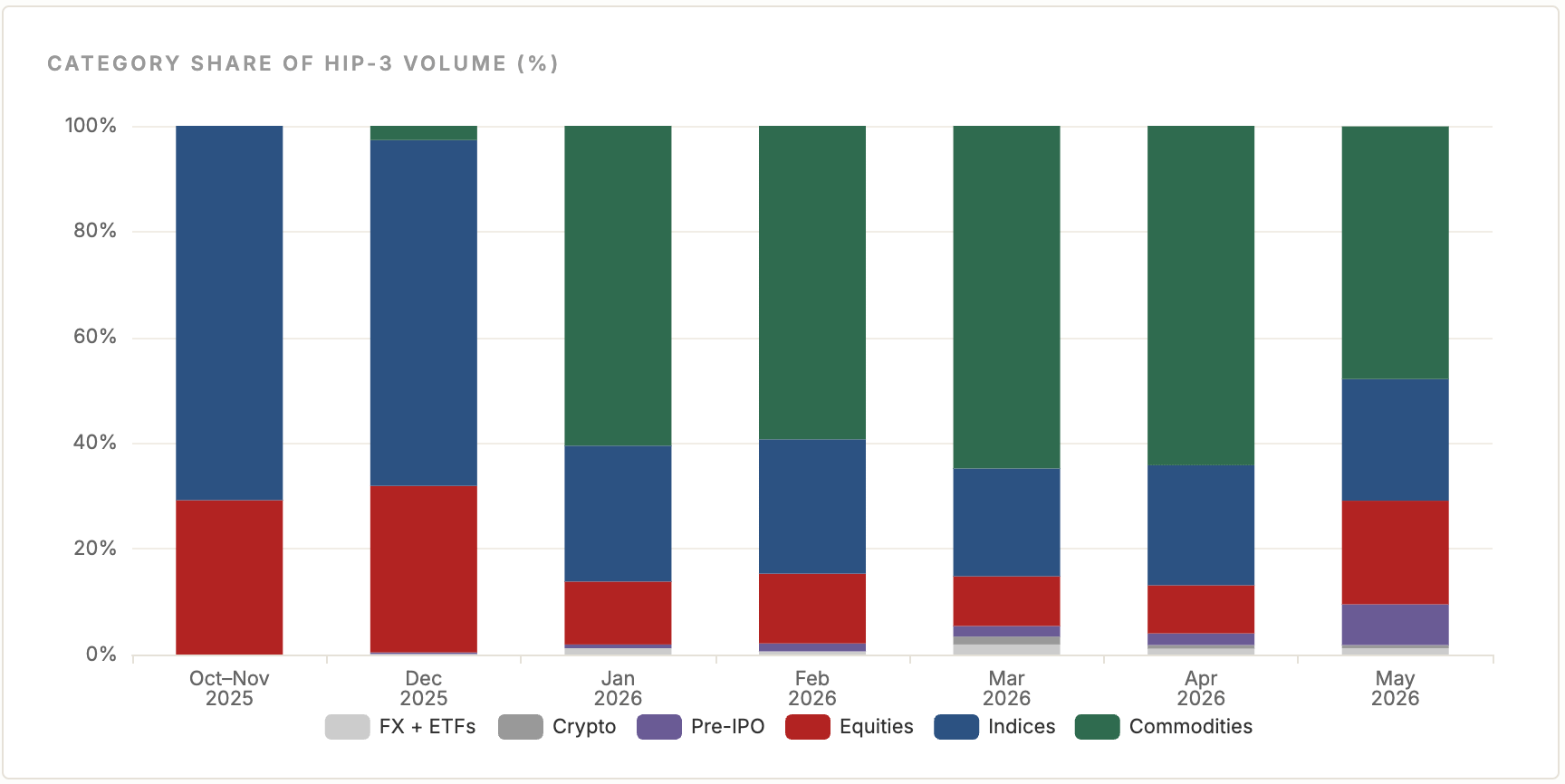

Since October 2025, Hyperliquid’s permissionless markets (HIP-3) have processed ~$270 billion across seven builder-deployed venues. Of this, 99% of trading came from commodities, equities, FX, equity indices, and pre-IPO contracts. Crypto stayed below 1% throughout. And the asset mix continues to diversify each month.

When the US-Israel conflict with Iran escalated over the last weekend of February this year, the world’s largest commodity exchange (CME) was closed. Hyperliquid’s WTI perpetual wasn’t. Trading volume on the platform surged from $25 million to over $550 million in three weekends. Hyperliquid had priced in roughly 80% of the subsequent WTI crude move before CME reopened on Monday, according to a recent report by TD Securities.

Even the perpetual contracts on silver hit nearly $1 billion in daily volume during the precious metals rally earlier this year. Trading on blockchain-enabled venues continued even when traditional markets were shut.

This isn’t limited to perps. The same behaviour is seen in equities trading.

US equities represent more than 60% of global equity market capitalisation. For most of the world’s investors, buying them requires intermediaries, foreign exchange conversion, minimum balances, and restricted account types.

Everyone wants a taste of the world’s largest economy and a place in its growth story. This explains why almost every crypto exchange wants to let its traders buy and sell U.S. equities or derivatives with U.S. equities as the underlying.

On June 1, Binance announced zero-commission access to 7,000 U.S.-listed shares and fractional ownership starting at $5 for all its 300 million registered users. The vast majority of them are outside the U.S. and can now gain exposure to U.S. equities using their stablecoin-funded wallets.

Kraken’s xStocks has already shown how tokenisation can impact access to public equities. The platform has tokenised over 100 public equities, generating $25 billion in trading volume with 80,000 on-chain holders.

Blockchains also unlock pre-IPO price discovery for traditional markets. SpaceX is preparing what could be the largest IPO in history by raising roughly $75 billion. On June 1, Anthropic confidentially filed its IPO papers. OpenAI is likely to follow. Before these companies go public, price discovery is opaque and restricted to accredited investors.

In Pricing the Private, I explained how the market is interested in pricing assets that behave like public companies.

Companies like OpenAI and Anthropic have brand recognition, revenue at scale, and hundreds of millions of users. They have everything a public company has except public shareholders. Their marketing has ensured that everyone has an opinion about them. In fact, there has never been a wider gap between everyone having an opinion on SpaceX, and yet almost nobody being able to price it.

Blockchain enables multiple tools to let the market price these private companies.

For instance, many platforms that started as crypto exchanges now offer pre-IPO perpetuals, prediction-market contracts, and tokenised IPO access for companies that have yet to go public.

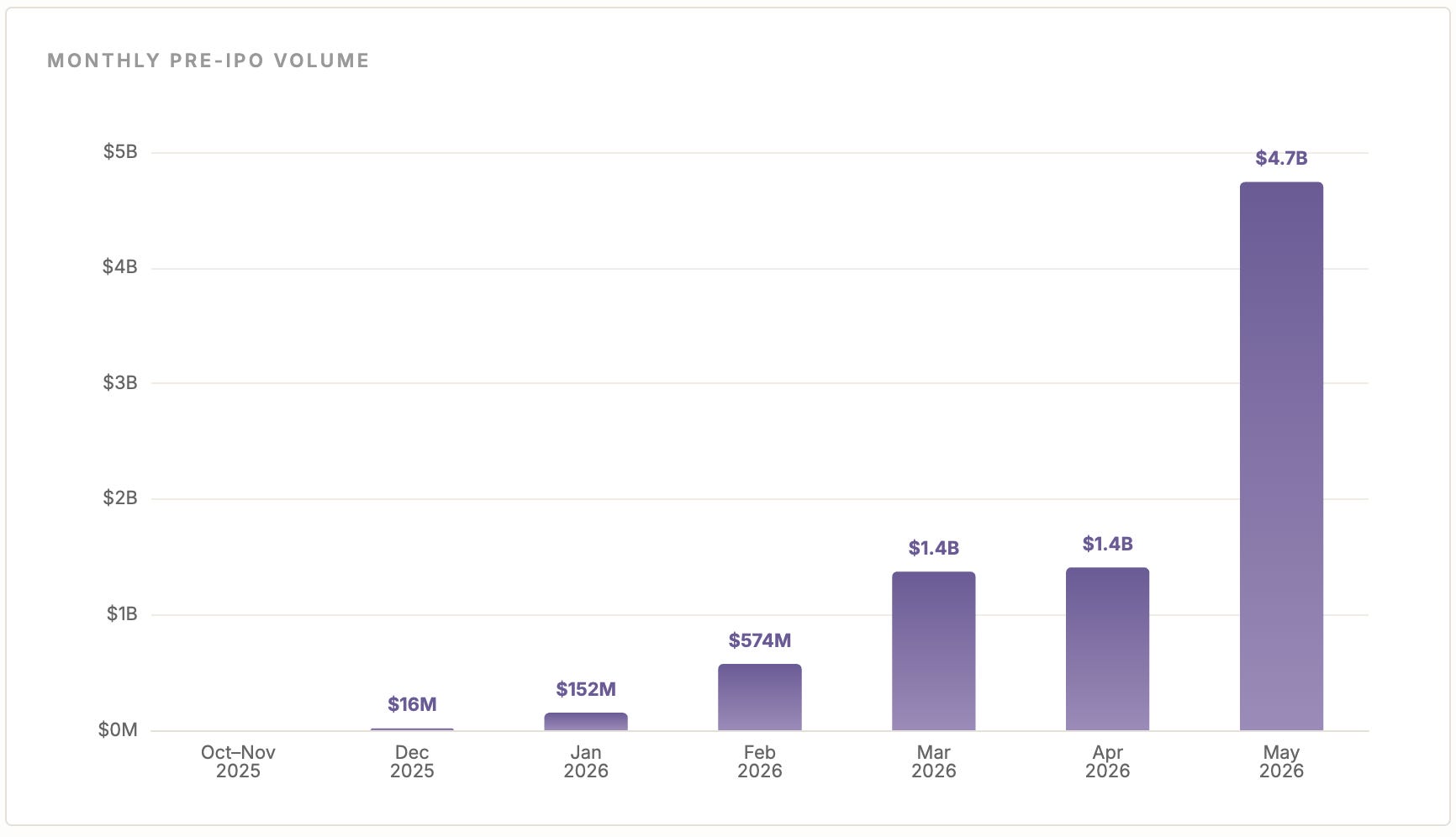

Multiple market makers have offered perpetual contracts on Hyperliquid for companies such as SpaceX, Cerebras, and Anthropic. The trading volume on these contracts has jumped about 300 times over the last six months, from $16 million to $4.7 billion. The perp contracts on pre-IPO stocks accounted for 7.7% of all HIP-3 activity in May, up from 0.2% in December 2025.

These venues are not just always on and cheaper, they also provide deep liquidity traders can trust.

During the Iran escalation, Hyperliquid’s WTI contract handled hundreds of millions in daily volume at tight spreads. Between January and April 2026, the open interest in a WTI Oil perp contract rose from $1.8 million to $560 million.

Traditional exchanges can also offer users cross-margin and deep liquidity by tapping into their user deposits. Binance offers its users access to pre-IPO stocks through its integration with PreStocks, while Payward (Kraken’s parent firm) allows its users to invest in tokenised IPO.

Less than 24 hours ago, Coinbase also joined Kraken and Binance by launching perp contracts on pre-IPO stocks, starting with SpaceX.

Building a Full-Stack Fintech

The convergence of traditional finance and crypto from both directions is creating a full-stack fintech platform for many of these companies. While crypto-native platforms are adding traditional asset classes, traditional exchanges are rapidly adopting blockchain infrastructure.

On the crypto side, Kraken spent over $2.7 billion on acquisitions in the past 12 months to turn into a multi-asset brokerage. In March 2025, it bought NinjaTrader for $1.5 billion — the largest deal ever to secure a CFTC-registered futures commission merchant.

It followed that up by acquiring Backed Finance to control xStocks issuance, trading and settlement in-house. Its product grew from 60 tokenised equities to 100 by early 2026. Five more acquisitions followed across payments, clearing and automated trading infrastructure.

It then launched Krak, a payments app supporting 300+ assets across 160 countries, that helps users spend, send and earn yield on their crypto.

Coinbase has lined up a similar stack.

At its December 2025 product event, Coinbase launched commission-free stock trading across all 50 states and prediction markets via Kalshi.

In August 2025, it acquired Deribit for $2.9 billion, giving it control of the largest crypto options market. Coinbase is now positioning USDC and its Layer-2 chain Base as settlement rails for everything from agentic payments to equity trades.

Each of these platforms entered finance through crypto and now boasts a distribution network that incumbents spent decades building. Binance has 300 million registered users. Kraken serves 15 million clients across 190 countries. These user bases are their biggest moats as they expand into multi-asset brokerages.

When Binance adds 7,000 US stocks, it doesn’t have to build demand from scratch. Access to these equities and pre-IPO stocks is being offered to people who have already topped up their wallets with stablecoins multiple times and have verified identities. The marginal cost of adding equities to an existing crypto brokerage is a fraction of what a traditional broker spends to acquire a single new customer.

The traditional incumbents are also adapting aggressively to stay relevant.

The same day Binance launched US stocks, the CME Group, the world’s largest derivatives exchange, announced 24/7 trading for all its crypto futures and options.

DTCC, which custodies $114 trillion in assets, will pilot tokenised securities this July and move to full production in October. The pilot covers Russell 1000 stocks, major index ETFs, and US Treasuries. More than 50 firms joined the effort, including BlackRock, JPMorgan and Circle.

NYSE partnered with Securitize to build a 24/7 tokenised stock venue. Nasdaq received SEC approval in March to trade tokenised equities within its existing rails.

It’s an interesting convergence. CME and other legacy institutions are adopting 24/7 operations because crypto has shown markets don’t need to close. Crypto exchanges are adopting traditional assets — oil, silver, indices — because users have shown that demand will shift to any platform that offers deep liquidity and a cheaper way to price information.

Blockchains are serving as a common bridge between the two.

Crypto’s Evolution as Fintech

As with any technology, online forums have defaulted to binaries about crypto’s use case. They expect crypto to either build a new, separate financial world or crumble under its own weight. But crypto is evolving in the area in between. The same happened with the internet.

While people were busy either writing it off or celebrating it as a new world, the internet, over time, became commoditised to the point where it is now invisible. Pretty much the entire world runs on it. Nobody argues anymore about the internet’s use case. It has become the common denominator enabling newer technologies on top of it.

This is exactly what I see unfolding for crypto. The technologies that come with crypto may not be achieving what the founding cypherpunks expected. I doubt most of them would even care; at least I don’t.

While the endogenous markets are busy debating BTC cycles and downturn narratives, a parallel exogenous side to the market is steadily expanding across multiple layers of the finance stack. Payment infrastructure, agentic commerce, integrated price discovery platforms, and now multi-asset brokerages. These businesses are thriving independent of whether BTC is at $60,000 or $100,000.

Hepworth Iron Capital’s Charlie Booth explains the endogenous-exogenous market evolution beautifully in his guest op-ed on Token Dispatch last week.

What interests me the most here is that a technology built to trade tokens is being used to give a retail investor $5 worth of access to Apple stock on a Saturday, settled in stablecoins with sub-cent fees, on infrastructure originally built for memecoins.

These possibilities happen only when the new infrastructure is significantly better than what it replaced. We all know old habits die hard. And the world is discovering blockchains as the magic pill to make finance work better. In some cases, by lubricating the legacy financial systems; in others, by altogether replacing the old, dilapidated systems. There is no wisdom in resisting change for the sake of it.

It’d also be suicidal for any industry run by humans to resist change that improves how existing systems work. That’s because of humans’ innate desire to improve inefficient systems. Things that make inefficient systems efficient are always adopted. No matter how new and how radical they might seem. Blockchains have evolved in a space with plenty of room to reduce such inefficiencies. The fact that legacy institutions and markets like Nasdaq, NYSE, and CME are adopting blockchain technology is a testament to blockchain’s evolving role in the future of finance.

Every exchange is a brokerage now (or will soon become one). Not all would have planned it, but that’s what they want to become. But what unfolds next? Who wins when every platform offers stocks, derivatives, prediction markets and crypto on the same app? It will come down to how well they integrate these assets across their platforms and enable their users to carry out some of the most fundamental tasks in the world of finance: spending, sending, receiving, and earning money.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.