Hello,

According to Defillama, crypto-collateralized lending reached a record $90 billion in Q4 2025. On-chain lending now accounts for approximately two-thirds of this total, up from less than half during the 2021 peak. On the other hand, private credit markets have more than doubled their market cap over the past year, increasing from $10 billion in February 2025 to $25 billion today.

DeFi has grown into a credible credit market, but institutional capital from asset managers, pension funds, endowments, and sovereign wealth funds accounts for only 11.5% of DeFi’s total value locked.

The gap between DeFi’s infrastructure maturity and its institutional adoption is the defining tension of this cycle.

In the last piece I wrote, we explored how DeFi’s vault ecosystem scales through open, verifiable infrastructure - blockchain’s trust layer replacing the human verification costs that make traditional asset management expensive to unbundle. That same property is what makes the next evolution possible.

When risk parameters, curator actions, and liquidation logic are all on-chain and auditable, it becomes possible to build a risk management infrastructure that would be too opaque or costly to coordinate in traditional finance.

Curated vaults were the first expression of this. However, institutions require more than curation; they need risk isolation across markets, fixed-rate instruments, and structured credit. This piece delves into the broader risk stack now emerging across DeFi.

Sygnum Bank, one of the few regulated digital asset banks, published a blunt assessment in mid-2025: stating that while DeFi protocols function, permissioned pools exist, KYC frameworks are live, and tokenised real-world assets are operational - no major institutional decision-maker will allocate to crypto until legal enforceability and regulatory risk are, in their view, fully resolved.

Sygnum added that nearly all inflows continue to come from asset managers, hedge funds, or crypto-native firms with higher risk tolerance. KYC-gated vaults and permissioned lending pools, often presented as institutional breakthroughs, have not attracted meaningful institutional flows.

The demand for DeFi exposure is real. A January 2025 survey of 352 institutional investors by EY-Parthenon and Coinbase revealed that 83% plan to increase crypto allocations, with 59% intending to commit more than 5% of their AUM. Yet only 24% currently engage with DeFi.

The concerns are valid. When these companies were asked why they don’t engage, regulatory uncertainty ranked highest at 57%. That’s a real barrier - but it’s also one that’s actively being dismantled. The GENIUS Act was passed. MiCA is being enforced across Europe. The SEC closed investigations into Aave, Uniswap, Ondo, and others without enforcement action.

What’s even more revealing are the other barriers the survey surfaced: compliance risk at 55% and lack of internal expertise at 51%. These aren’t about whether DeFi is legal, but about whether institutions can operationalize DeFi exposure within their existing risk frameworks. Can a compliance team map a lending position to an internal mandate? Can a risk officer isolate exposure to a specific type of collateral? Can a portfolio manager delegate allocation to a professional curator with defined parameters?

Today, in most of DeFi, the answer is still no. However, the on-chain risk dynamics are changing.

The Missing Layer

The reason behind this is structural to crypto. Institutional investors allocate approximately 41% of their portfolios to fixed income, according to Fidelity research. Insurance companies, pension funds, and endowments don’t do this because they lack risk appetite; they do so because their mandates require predictable cash flows to match long-dated liabilities.

The infrastructure that enables this - interest rate swaps alone represent $469 trillion in notional outstanding, per BIS data - is fundamentally about one primitive: risk segregation - splitting exposure into fixed and variable components so that different participants can take the side that matches their mandate.

DeFi’s first cycle omitted these risk-segregation primitives. The design philosophy of 2020–2021 focused on shared pools, uniform risk parameters, governance-voted collateral decisions, and variable rates.

Every depositor had the same exposure.

For crypto-native capital - hedge funds running basis trades, yield farmers chasing incentives - this model worked. DeFi lending grew from a few hundred million to tens of billions. But the architecture imposed a ceiling. When there’s no mechanism to segregate risk, no way to isolate exposure to specific collateral types, or no way to delegate risk decisions to a professional curator, the capital managing $130+ trillion in global fixed income has limited entry points.

What’s Changing

Across several major protocols, a structural shift is underway.

The common thread among them is the introduction of risk management tools, allowing institutions to customise experiences according to their compliance and risk appetite.

Risk isolation

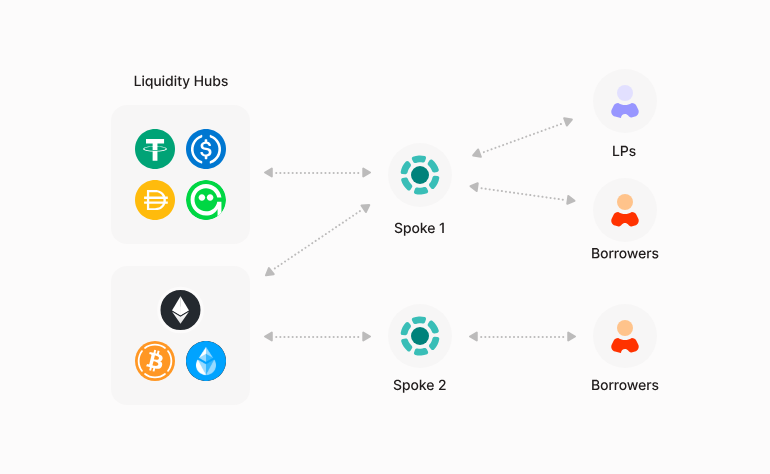

In Aave V3, each lending market is a self-contained pool - its own liquidity, its own assets, and its own risk parameters. Creating a new market for a different risk profile entails bootstrapping liquidity from scratch, which is costly and yields thin pools with higher rates.

Aave V4, currently on the public testnet and with a mainnet launch targeted for early 2026, splits the system into two layers. A central Liquidity Hub holds all assets per network, while user-facing Spokes define their own risk rules, collateral types, and access controls.

Spokes draw liquidity from the Hub rather than maintaining their own. Thus, in this new model, liquidity is shared, but risk is segregated. An RWA Spoke where institutions borrow stablecoins against tokenized treasury bills can set its own LTV ratios, liquidation parameters, and access controls - completely independent of a high-beta crypto Spoke operating next door.

Both tap the same deep stablecoin pool, but a liquidation cascade in one doesn’t contaminate the other.

Aave’s Horizon platform, which operates a similarly permissioned RWA market, surpassed $550 million in net deposits, with Kulechov targeting $1 billion by 2026 through partnerships with Circle, Ripple, Franklin Templeton, and VanEck.

Delegated risk curation

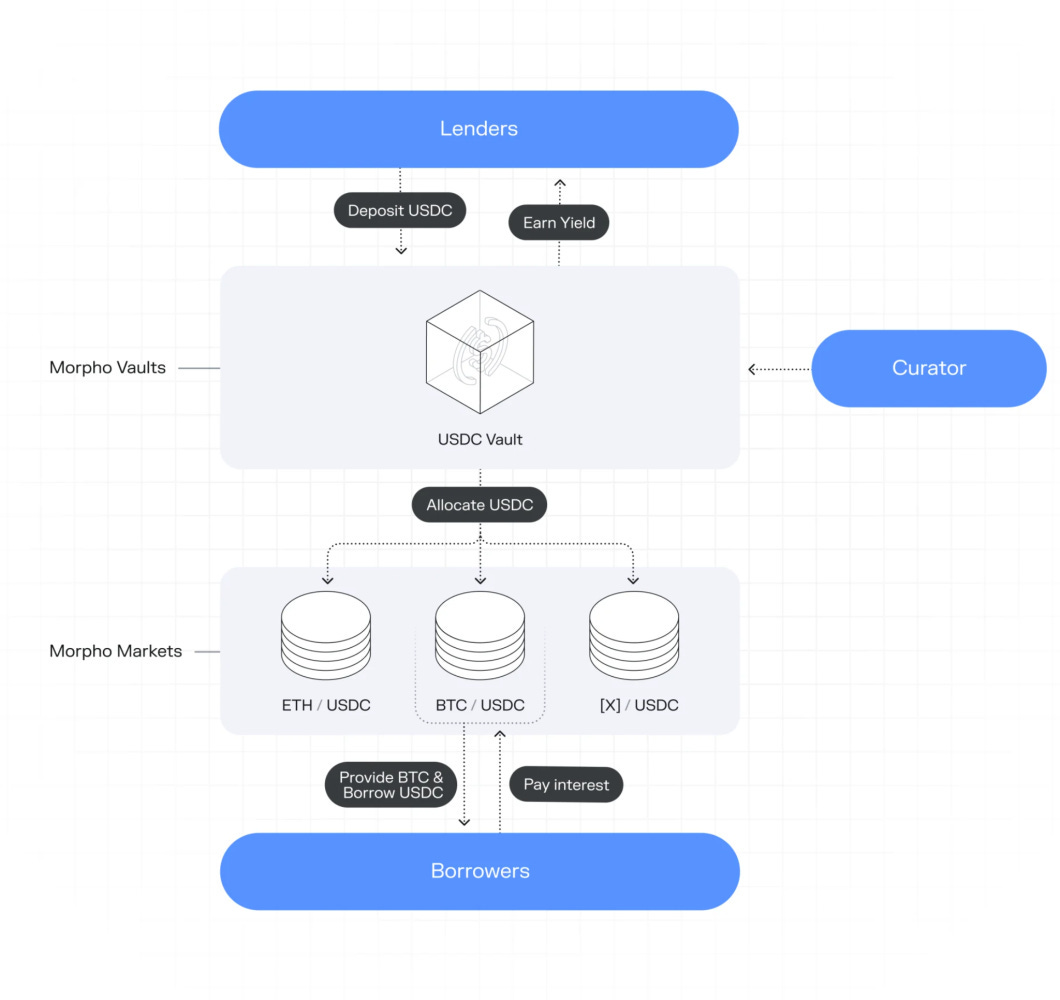

Morpho may have built the UX fix for the institutional on-ramp to DeFi lending. Remember the institution’s ‘lack of internal expertise?’ Morpho vaults might be the solution. Its vault system separates liquidity provision from risk management by introducing professional curators - independent teams that define collateral policies, set exposure limits, and allocate capital on behalf of the capital provider across lending markets.

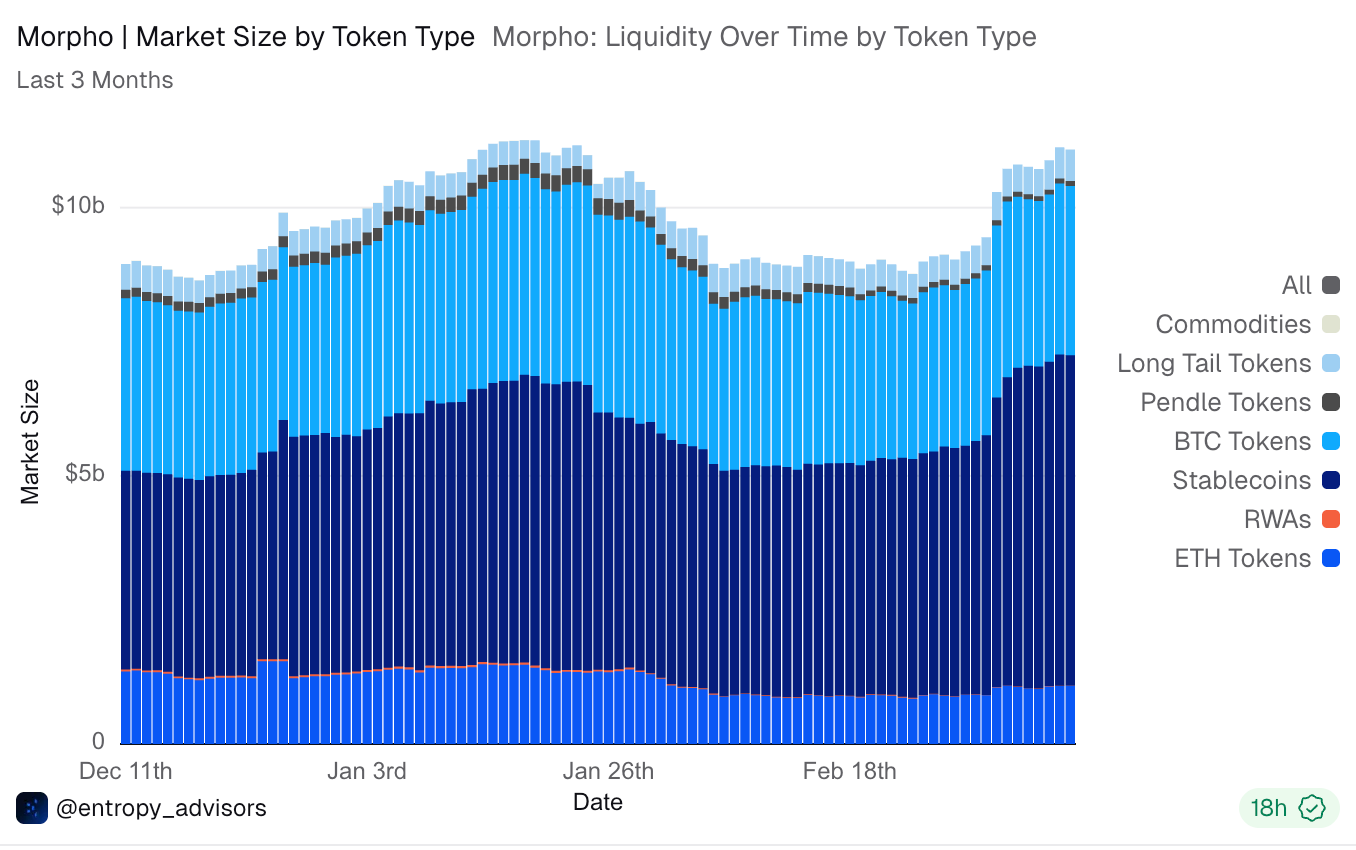

More than 30 curators now operate on Morpho, with total deposits increasing from $5 billion to $11 billion and active loans reaching $4.5 billion.

Morpho provides an optimal balance between generating passive yields and managing risks, and institutions are beginning to see its benefits.

In January 2026, Bitwise, a registered asset manager with over $15 billion in client assets, launched its first non-custodial vault on Morpho, with a dedicated portfolio manager overseeing strategy and risk management.

Anchorage Digital, America’s first federally regulated digital asset bank, now provides institutional clients direct access to Morpho Vaults with custody of the resulting vault tokens.

Coinbase integrated Morpho to power its crypto-backed lending product, supporting over $960 million in active loans. Société Générale Forge, Gemini, and Crypto.com have built similar integrations.

For a deeper look at how the vault stack’s unbundled architecture - protocol, curator, distribution - scales through blockchain’s trust cost compression, check out my last week’s piece, DeFi’s Capital Aggregator.

Yield predictability

One of the fundamental mismatches between DeFi and institutional capital is the rate structure. DeFi lending rates are variable by default, fluctuating with pool utilization, sometimes swinging from double digits to single digits within days.

For a pension fund or insurance company that needs to match predictable cash flows with long-dated liabilities, this is infeasible. You can’t commit to a 7% payout to beneficiaries if your yield source might drop by 5% next month.

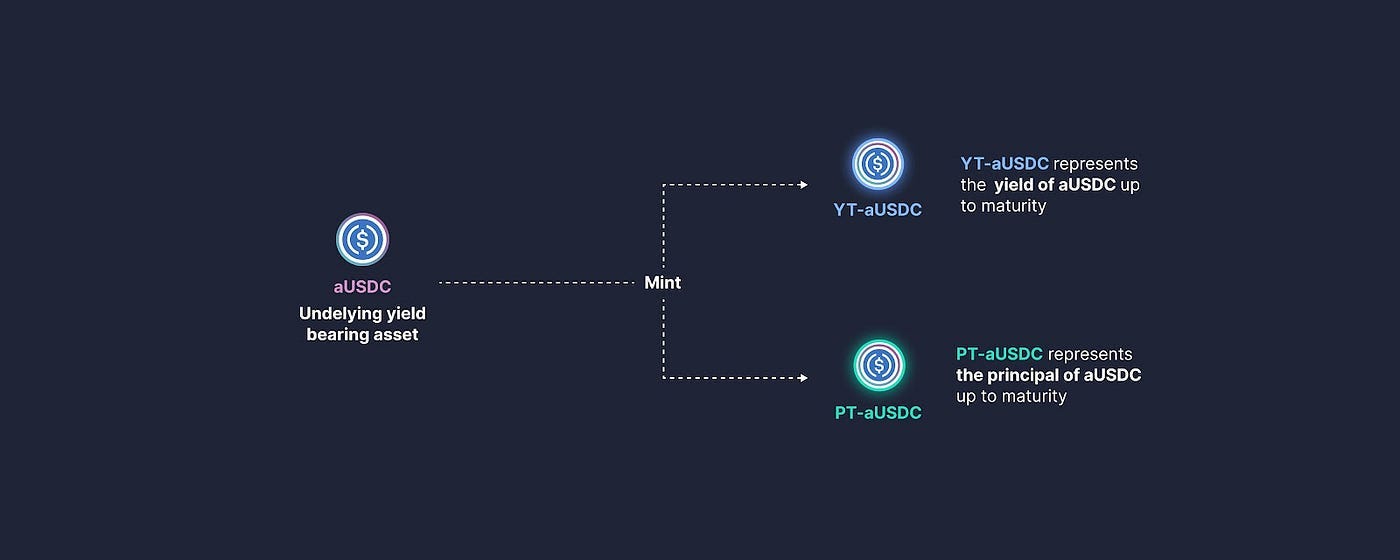

Pendle addresses this by splitting yield-bearing assets into two tradable tokens: a Principal Token (PT) that represents the underlying asset and is redeemable at maturity, and a Yield Token (YT) that captures all variable yield generated up to that maturity date.

This separation mirrors traditional fixed-income instruments; the PT functions like a zero-coupon bond. At the same time, the YT isolates floating-rate exposure for those who want to speculate on or hedge against rate movements.

An institution that buys the PT locks in a fixed return, whereas a trader who buys the YT leverages exposure to variable yields. Both sides get what they need from the same underlying position.

Pendle settled $58 billion in fixed yield in 2025, a 161% year-over-year increase, and generated over $40 million in annualized protocol revenue.

Its Boros platform, launched in early 2026, extends this into funding rate derivatives - allowing institutions to hedge or gain exposure to perpetual futures funding rates, a market with over $150 billion in daily volume that previously had no on-chain hedging tool.

On-chain credit diversification

Most DeFi lending protocols generate yield from one source: overcollateralized crypto loans with variable rates. When markets cool, utilization drops, rates compress, and yield drops.

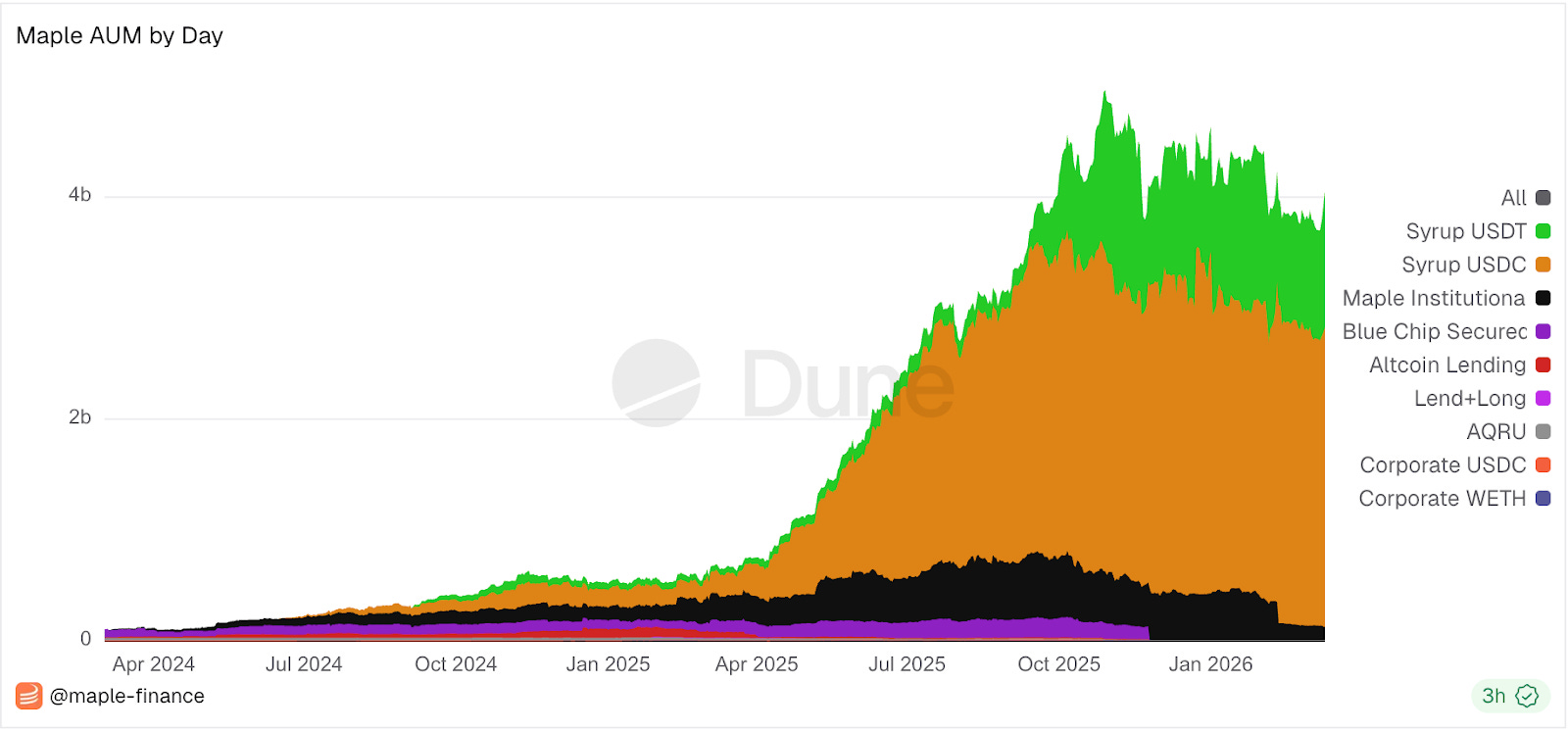

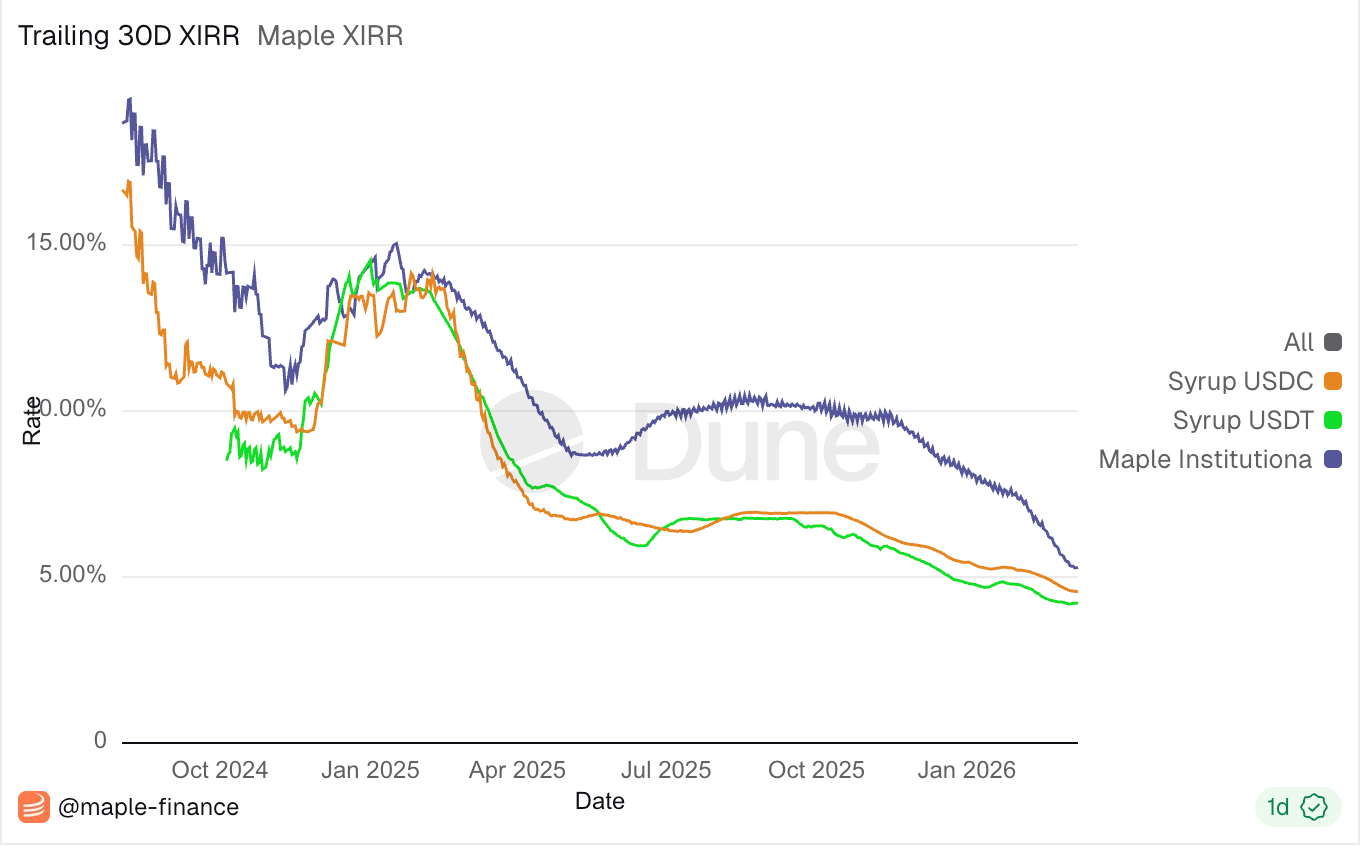

Maple Finance has been diversifying its return generation. Its core product underwrites overcollateralized, fixed-rate loans to institutional borrowers - trading firms, market makers - with real-time on-chain visibility into collateral. Currently offering a 5.3% 30 day APY.

Beyond that, it launched a BTC Yield product in early 2025, generating Bitcoin-denominated returns, and a High Yield Secured Pool that delivered 9.2% in Q2 2025 through active credit underwriting.

Its syrupUSDC token - a liquid receipt of lending pool participation - integrates with Aave, Morpho, Spark, and Pendle, allowing depositors to compose yield across protocols or lock in fixed rates via Pendle’s yield tokenization. The result is a multi-strategy credit platform rather than a single lending pool.

Maple’s AUM scaled from $516 million to $4.59 billion through 2025, with outstanding loans growing eightfold and Q4 annualized revenue reaching $30 million.

CEO, Sid Powell, has signaled ambitions to push into structured credit - securitization and asset-backed products. In practice, this would mean taking a pool of on-chain loans and slicing it into tranches: a senior slice that is paid first and carries lower risk, and a junior slice that absorbs losses first but earns a higher return.

This is the mechanism that enables traditional credit markets to scale from billions to trillions; it makes the same pool of loans investable for both a conservative pension fund and a yield-seeking hedge fund simultaneously. These products are not yet live, but the direction signals diversification of their on-chain credit offerings to accommodate all risk profiles.

The Pattern

The individual protocol details matter less than the structural pattern they reveal. DeFi is rebuilding TradFi’s risk management primitives - risk isolation, curation, tranching, fixed rates, compliance gating - in a programmable, transparent, and composable form.

This distinction is important. The smart contracts are auditable. Settlement is real-time. Vault allocations are visible on-chain. Curator actions are time-locked and observable.

None of the opacity that characterises traditional risk infrastructure is necessary. What’s being imported is the functional architecture - the separation of concerns that allows different types of capital to coexist within shared infrastructure.

The vault ecosystem is where this convergence is most visible. Bitwise’s 2026 outlook described on-chain vaults as “ETFs 2.0” and predicted their AUM would double this year. Morpho believes its vaults are the savings account layer that follows the success of stablecoins as the checking account layer: stablecoins brought money on-chain; vaults put it to work.

As more institutions, fintechs, and neobanks embed vault-powered yield products into their offerings, the end users may not even realize they’re interacting with DeFi infrastructure.

The crypto-collateralized lending market is healthier than it has ever been. Galaxy’s research noted that the current leverage cycle is built on collateralized, transparent structures, replacing the opaque, uncollateralized credit that defined 2021.

However, scaling beyond crypto-native capital requires a risk layer that aligns with institutional mandates. The protocols building that layer - through modular risk isolation, professional curation, fixed-rate infrastructure, and on-chain structured credit - are the ones positioned to capture the next order of magnitude in capital.

Whether they succeed depends less on their TVL and more on whether institutions come to trust that these on-chain risk controls are as reliable as the ones they already operate within. That question remains open. But, for the first time, the architecture to answer it exists.

Until then, stay safe.

Nishil

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.