“F*ck you, pay me” - Ray Liotta in Goodfellas.

That’s how this dismantles any romanticised vision of mafia honour, like The Godfather, and shows the world the ugly, cold, and parasitic nature of organised crime.

Let me do you the honour of applying the same (or similar) logic to big tech.

Capture the margin, and you capture the value. To accomplish this, you need neither a protocol nor a project. It’s a war for the margins, and there are no rules.

But we can’t blame Coinbase, or Stripe, or Kraken for choosing that.

What they did, in the most fundamental, basic sense, was make a good real estate move. They got to distribution first. Now, they can look down and say, “Who has the leverage here?”

Coinbase built a blockchain, and Stripe bought infrastructure for $1.1 billion that it could have rented. Kraken built a derivatives trading platform for $1.5 billion. Apple built an App Store. You let someone else build the market, take the early risk, and you swallow the infrastructure once it becomes too profitable to avoid.

This is a piece about what happens when distribution no longer has value.

Coinbase has 110 million verified users. For years, the lending product it offered those users ran through Morpho, an open protocol, which kept the protocol fees.

Then, Coinbase built its Layer 2 blockchain, Base. Morpho deployed on Base because Coinbase’s users meant volume. Every transaction processed on Base now generates a sequencer fee that goes to Coinbase, instead of Morpho.

Read: Morpho Is Becoming the Backend - by Thejaswini M A

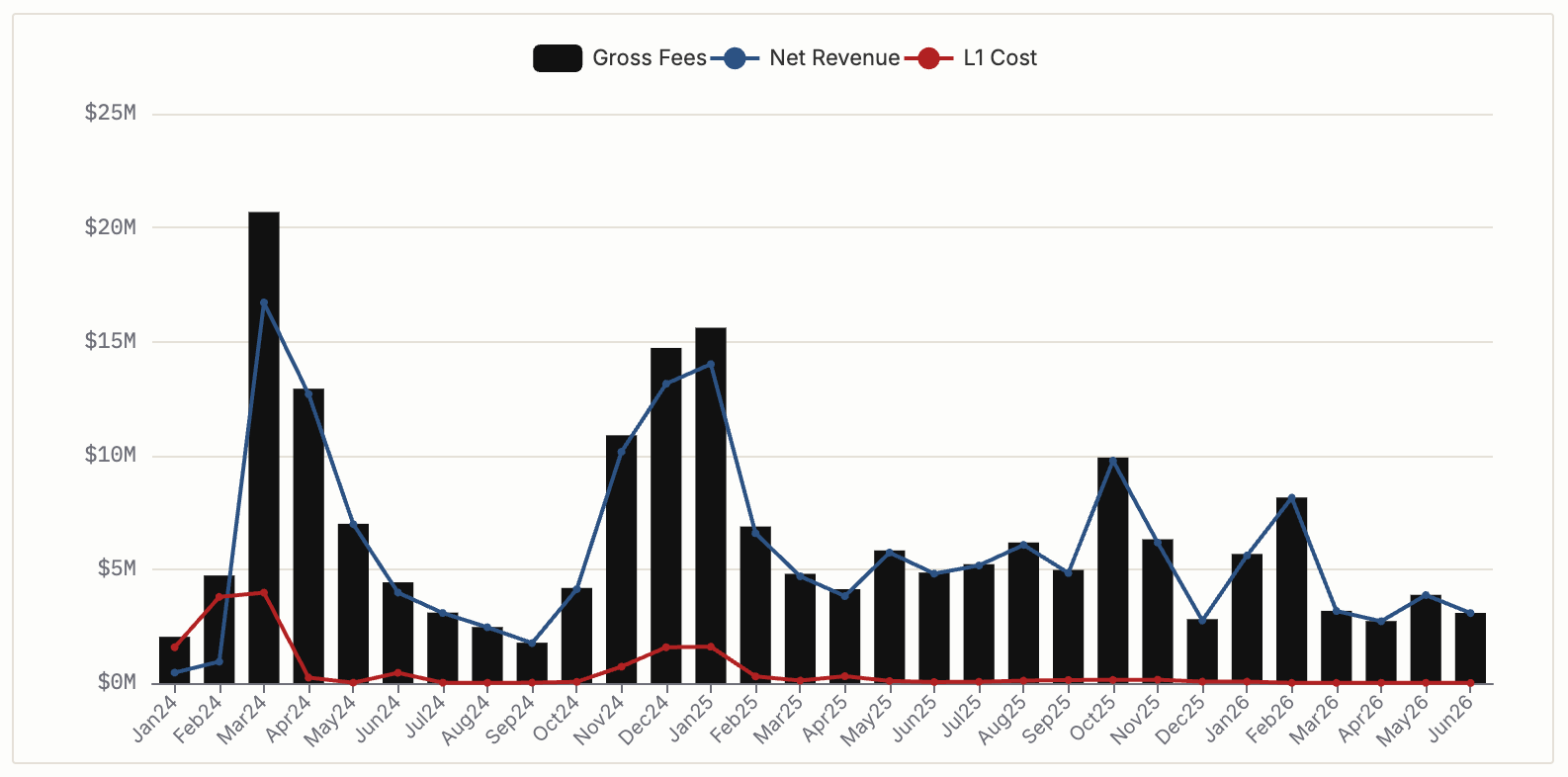

Base generated $76 million in net sequencer revenue in 2024 and $74 million in 2025. Up until February 2026, they had to hand a chunk of that over to Optimism under a licensing deal. But Coinbase eventually cut the cord, moved to their own stack, and now they pocket the full $64 million. Meanwhile, Morpho is still right there on Base, doing great and managing $2.5 billion in TVL. But a cut of every single transaction Morpho processes goes directly into Coinbase’s pockets.

Coinbase built its $300 million bitcoin-backed loan product directly on Morpho infrastructure. cbBTC, Coinbase’s own wrapped bitcoin product, is the single largest collateral type on Morpho, representing 38% of all assets locked in the protocol. This makes Coinbase simultaneously Morpho’s biggest customer and the company that takes a toll on everything Morpho does. Morpho has leverage over Coinbase’s product. Coinbase has leverage over Morpho’s revenue. Neither can easily walk away.

In Stripe’s case, in early 2025, it paid $1.1 billion for Bridge. Before that, Stripe routed its stablecoin operations through Circle’s infrastructure. But with that, Circle controls the stablecoin issuance and captures the reserve float on the backing assets. When Stripe moved through Circle, it was a billion dollars generating yield for Circle. Bridge redirects that. It has USDB, its own stablecoin backed by BlackRock money market funds. By switching to USDB, Stripe keeps that massive reserve yield entirely inside its own ecosystem. When you process $1.4 trillion in annual payment volume as Stripe does, renting the yield engine from a competitor is worth hundreds of millions of dollars a year.

Patrick Collison called stablecoins “room-temperature superconductors for financial services.” Spending $1.1 billion was the price of owning that superconductor outright, rather than paying someone else’s toll to use it.

As a basic spot exchange, Kraken has a natural ceiling where users can only trade a few hundred tokens. However, the institutions and serious retail traders Kraken wants to attract run their books on futures and cleared derivatives. Operating that kind of business requires CFTC registration, NFA membership, broker-dealer credentials, and compliance frameworks that take years to establish. Even if you try to build everything from scratch, the government can still deny your application for reasons entirely outside your control.

This is why Kraken looked at NinjaTrader. The $1.5 billion acquisition in January 2025 bought them 1.7 million funded accounts, but more importantly, it secured the broker-dealer licenses Kraken couldn’t build fast enough organically.

By purchasing those readymade permission slips, Kraken eliminated its dependency on outside partners. They no longer have to rely on anyone else or wait years for government approval because they now own all the technology and licenses themselves.

So big company eats small protocol. Big deal, what’s new?

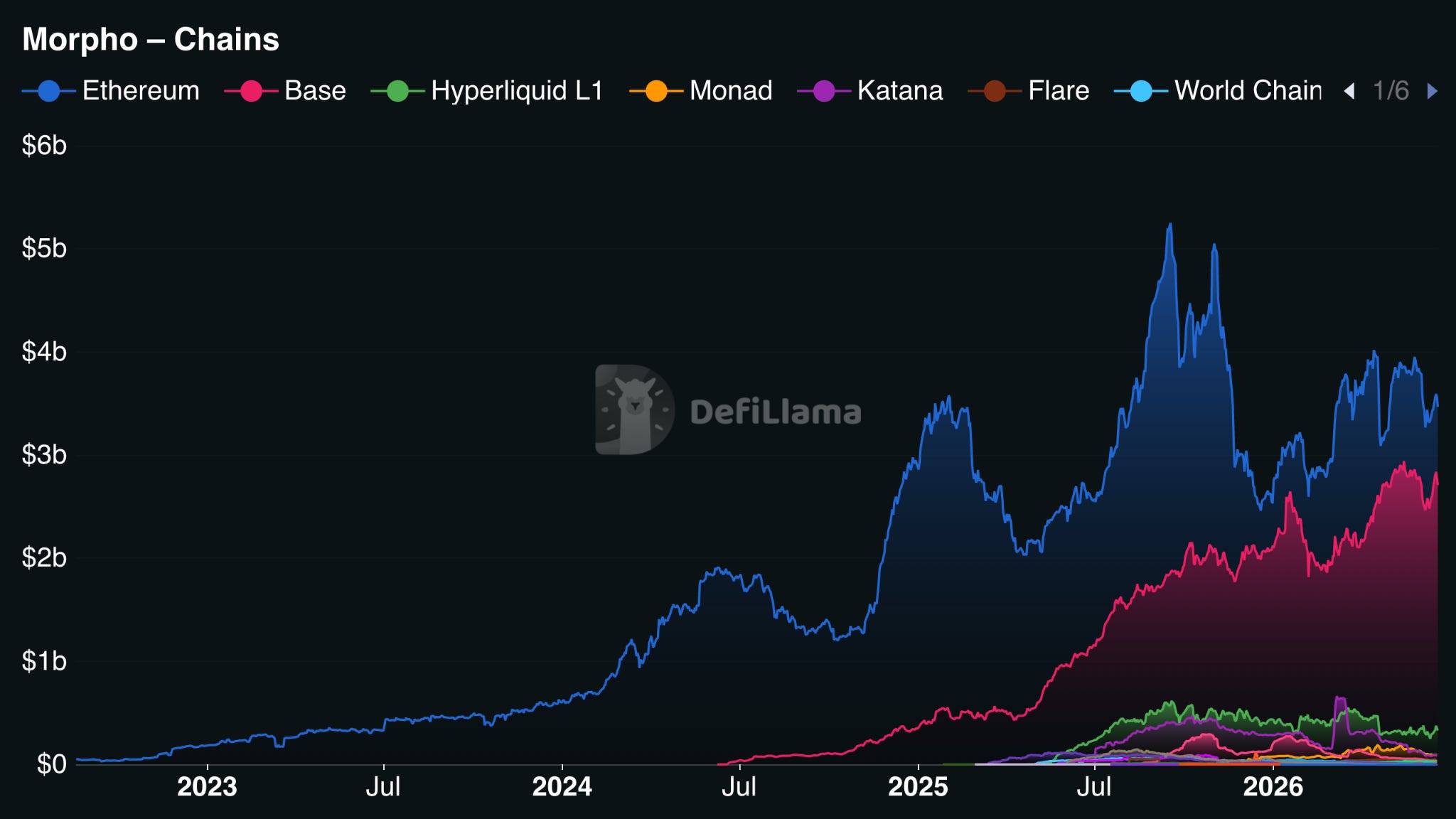

Morpho’s total value locked stands at $6.4 billion. Of this, $3.308 billion is on Ethereum, and $2.488 billion is on Base. If Coinbase decided to remove Morpho from Base in favour of their own lending protocol, Morpho would lose 39% of its TVL, but would maintain 52% on Ethereum and, along with its growing positions on Hyperliquid L1, Monad, Arbitrum, and many other chains, would continue to thrive.

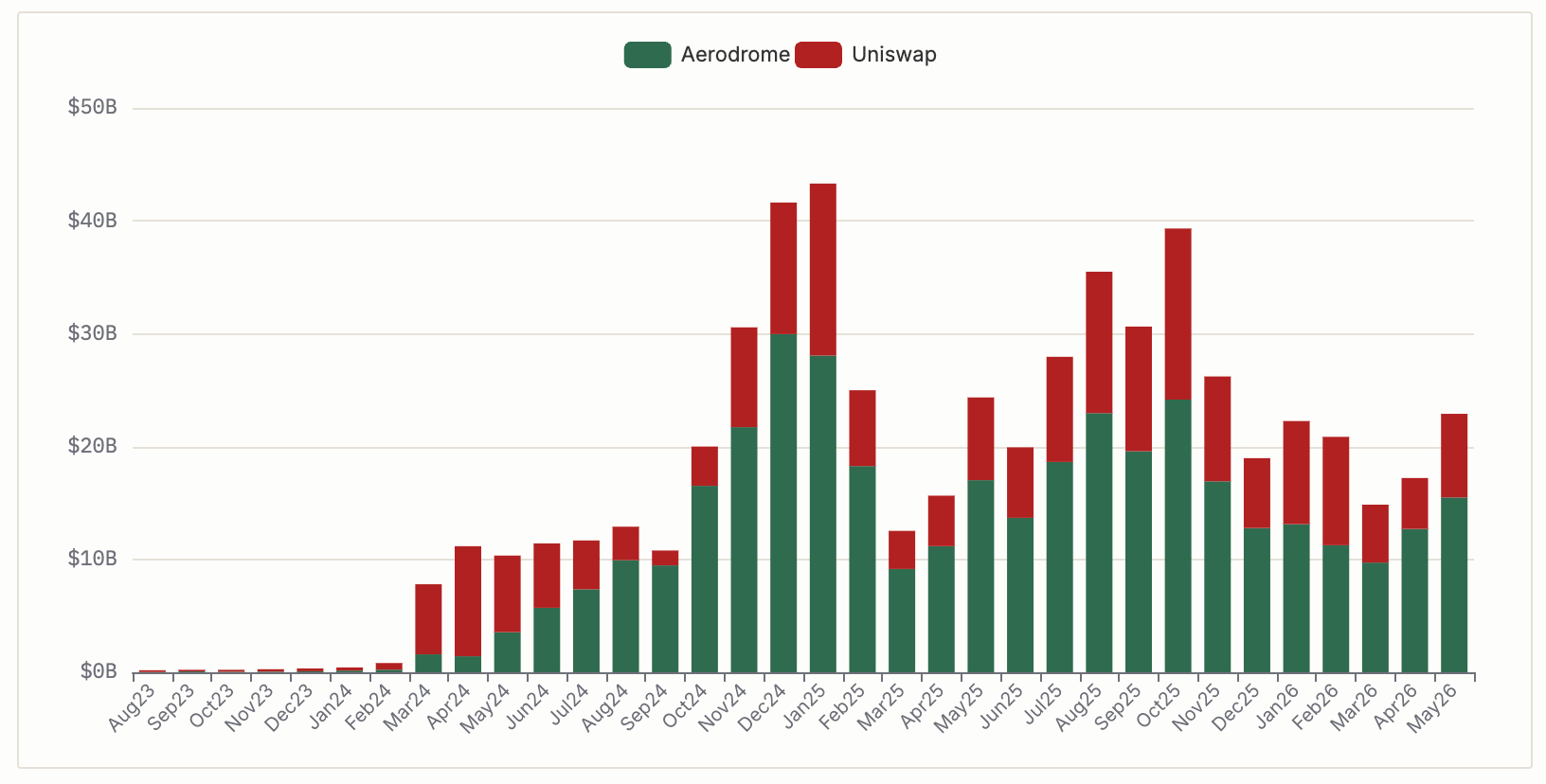

Aerodrome on Base shows the effects when a chain operator sponsors one of their own competitors. Aerodrome launched Base’s native DEX and was optimised for Base’s architecture. Coinbase Ventures has approximately $20 million in AERO, its largest liquid token investment, and votes with locked AERO to direct liquidity to Coinbase’s products, including the cbBTC liquidity pools. Aerodrome processed approximately 51% of the Total DEX volume on Base, peaking at 77% in September, 2024. Uniswap, which runs on 44 chains, is the second DEX on Base, processing 30% of Base DEX volume. Uniswap has not ‘died’, as it lost dominance on one chain, while processing Base’s $212 billion in 2025 volume and estimating $73 billion monthly across all chains.

In this case, being multi chain is actually protection. A protocol that focuses on a single chain is at the mercy of the single chain operator if that chain’s operator then favours a competing protocol. A protocol that engages with multiple chains loses only one market segment, but retains the rest. Morpho watched Aerodrome capture Base’s DEX volume from Uniswap and quickly deployed across multiple chains. The massive distribution companies can go downward. The systems can extend horizontally.

If you depend on an infrastructure layer you don’t own, you don’t own your business. The entity controlling that layer has massive leverage over your profit margins. They dictate your product experience. Ultimately, they control your operational stability. At the scale these companies operate, that dependency costs real money every single day. This is not an insight unique to crypto. Amazon did this with AWS, Apple saw how Intel’s chip roadmap dictated the direction of every Mac and spent years developing its own custom silicon.

Anyone can track exactly how much Coinbase earns from Base sequencer fees or view Morpho’s total value locked across different chains. This value extraction is visible in real-time, in a way that Amazon’s internal infrastructure margins never are.

If the future is a few massive companies like Coinbase, Stripe, Kraken, and a couple of banks own everything.

They have all layers from protocol to card, with open source protocols only filling the gaps that the companies have not occupied. This is a legitimate potential FinTech scenario. Open-source tech won’t be this grand, free frontier anymore. It’s just going to be the duct tape used to fill the tiny cracks that the mega corporations haven’t figured out how to monetise yet. ‘Oh, look at that lovely little open-source protocol... let’s build a Starbucks over it.’

My optimistic side view is that the outcome is less likely than it looks from the current deals. The protocol layer is hard to own, the way distribution is owned. Morpho can deploy on a new chain in weeks. The switching costs for replacing an embedded, battle-tested lending protocol are high, even when they’re invisible from the outside. Coinbase’s $300 million bitcoin loan product runs on Morpho because rebuilding Morpho’s security model from scratch would take years and introduce risk Coinbase doesn’t want to carry.

The protocols poised to survive this wave are those that achieved multi-chain ubiquity before the distribution giants started building their own networks, embedding themselves so deeply into corporate backends that replacing them becomes economically prohibitive. Even a distribution powerhouse like Robinhood chose to integrate Lighter for its trading infrastructure. Lighter is a third-party zk-rollup perp exchange, and started routing users there. Robinhood Ventures backed Lighter’s $68 million raise. Vlad Tenev sits close enough to the project to call it personally.

If distribution alone were the only moat that mattered, Robinhood would have built in-house the way Coinbase did. It didn’t, because verifiable zk-proven matching at CEX speed is a hard, narrow problem that took Lighter’s team over a year to solve, and Robinhood decided buying access to that expertise was cheaper than rebuilding it.

Morpho currently occupies this dual strongpoint, and Uniswap was its pioneer. Velocity of institutional encroachment versus the speed of protocol proliferation. The result of that can tell us what is what.

The layer below each of them big names (Stripe and Coinbase) is still open source. For now, that’s enough. Ask again in two years.

I will come back in two days, until then…

Stay tuned.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.