Hello,

Tokenisation is stitching together two contrasting worlds: the always-on, permissionless DeFi protocols where prices move every few seconds, and traditional funds where settlement follows administrative time blocks for a set of permissioned holders.

Bringing the two together involves an unenviable orchestration. But it comes with a value to capture for those who can pull it off. In today’s piece, I will explore who is orchestrating the layer connecting the two worlds and who captures the value it provides.

On to the story…

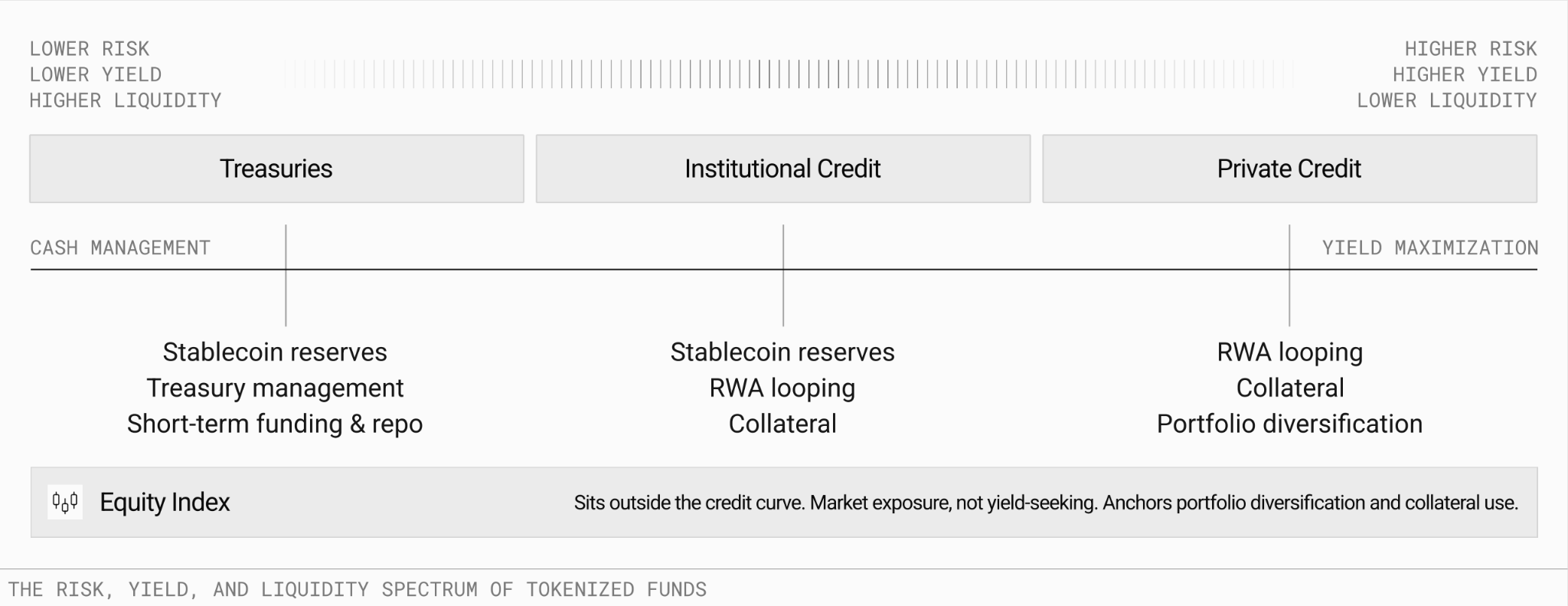

The tokenised real-world asset (RWA) pool sits above $33 billion, with tokenised US Treasuries accounting for roughly $15 billion. Interestingly, though, its share has slipped from 55% to less than 45% in just a year. There’s been a rise in other tokenised funds, including institutional credit (eg: Apollo’s ACRED) and private credit (eg: Janus Henderson’s JAAA).

This coming-of-age of tokenisation has opened up a spectrum of options across risk profiles for a treasurer or a CFO managing corporate cash. Those seeking lower risk, lower yield, but higher liquidity can opt for treasury funds, while those seeking higher yield and greater programmability can pursue riskier options. The safety of the yield is no longer the problem it once was. These are Treasury-backed instruments audited by the same firms that audit their traditional cousins.

This is the strongest pitch for why tokenisation of real-world assets is ready to blow up among institutional investors.

If someone asked me what separates off-chain money from on-chain money, I’d say composability. It is what lets a dollar do much more across many avenues, helping it compound more. Instant redemption and the ability to make your money work harder make it look like funds on steroids.

Traditional finance made us pick between yield, liquidity, and mobility. Tokenised funds, if managed well, let us keep all three.

But the “managed well” part isn’t as easy. Composability with a fund involves an engineering problem.

Stitching Two Contrasting Worlds

Blockchains bring speed, cost efficiency and fast settlements to tokenised RWAs. But a tokenised money market fund is still a fund, not a stablecoin. It still has to update the NAV once per business day, according to the fund administrator’s clock. It still has to maintain a KYC’d set of holders. For example, BlackRock’s BUIDL has a minimum investment threshold of $5 million, and Circle’s USYC is limited to non-US persons. It still has to honour redemption cutoffs because the T-bills underneath settle on the off-chain infrastructure that closes at 5 pm Eastern Time.

This is the legal substance of the product that cannot be eliminated. If you kill the NAV daily strike, then it isn’t a money market fund anymore. If you do away with the whitelist, then the SEC will come knocking on your door with questions.

So how do you let a fund keep its clock, its holder set, and its redemption windows, while the token representing a share of that fund moves at internet speed? Funds need purpose-built infrastructure that maintains the NAV at period-end, supports epoch-based settlement, and upholds strict legal boundaries when moving assets across blockchains. It’s a tricky coexistence problem to solve.

A recent joint report from LayerZero and Centrifuge describes how they solve it.

Solving the Conflict Points

Three points of conflict determine whether the coexistence works. If the orchestration layer gets them right, the fund can move at internet speed without violating legal boundaries.

First is the price.

What is the token worth between NAV strikes? Some issuers freeze it at yesterday’s mark and accept the staleness. A frozen price is easy to game when interest rates move mid-day. A continuous price is harder to game but harder to reconcile with the fund’s actual accounting.

Second is the compliance factor.

Where does the whitelist verification layer run? If it runs on every transfer, the token can’t touch open DeFi and can move only between approved wallets. If the layer moves into a vault wrapper, the vault holds the regulated share and issues a freely-circulating receipt token to holders who have cleared KYC once. This receipt becomes composable via DeFi, with compliance embedded in the vault rather than checked on every transfer. Centrifuge’s deRWA framework is a good example of this.

The third conflict arises while moving assets cross-chain.

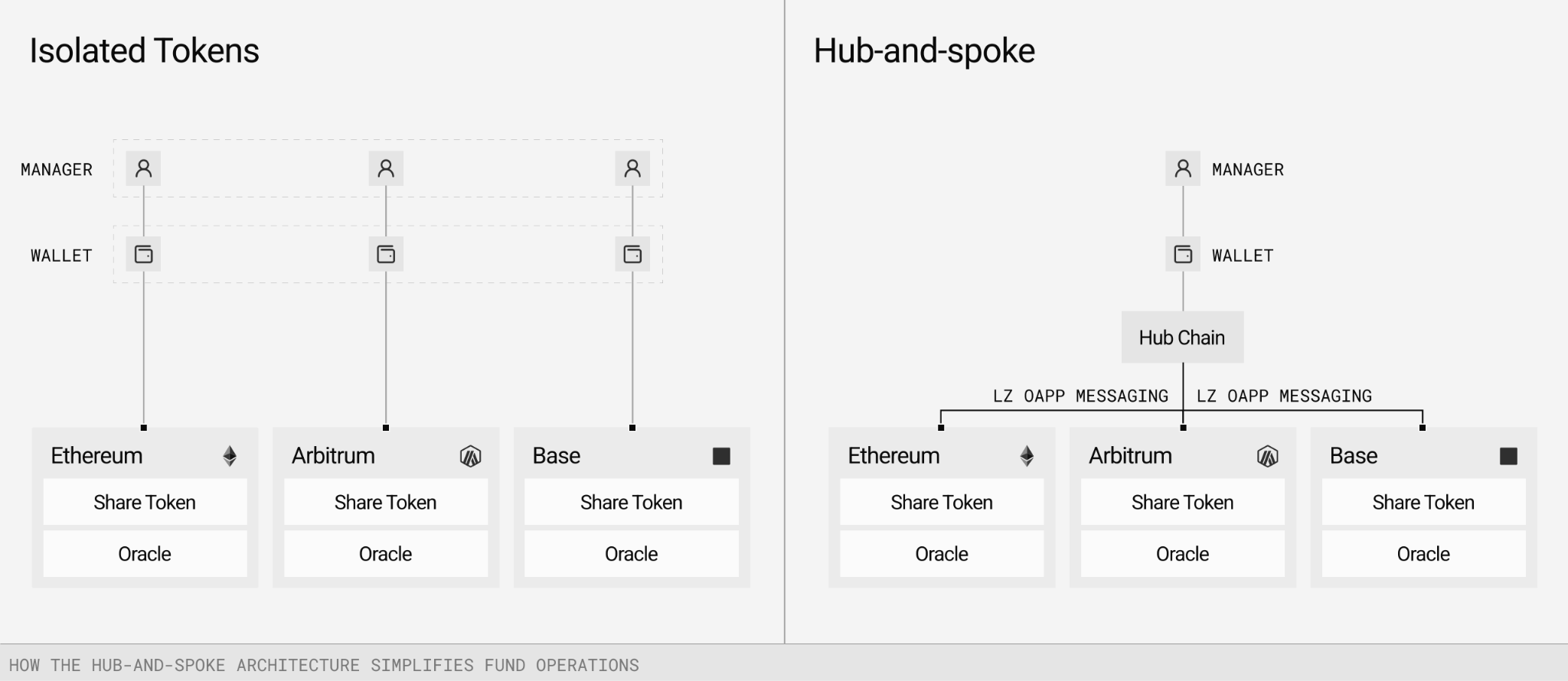

When a tokenised fund is deployed across nine chains, you need a single source of truth for who owns what and what it’s worth. Although on-chain infrastructure can be updated in real time, it still requires updates and reconciliation across nine chains in the event of discrepancies. The more points of failure there are, the more likely an error is to creep in.

LayerZero and Centrifuge addressed this by building a hub-and-spoke model. In this, a single authoritative chain covers NAV, accounting, and compliance. A messaging layer, orchestrated by LayerZero in this case, pushes those updates to the spoke chains where the token actually gets used.

Centrifuge’s V3 architecture is built on this model, in which each pool selects a hub chain as its source of truth, spokes serve as distribution endpoints for deposits, and DeFi composability is enabled. LayerZero carries the operational data between them that ensures NAV updates, compliance instructions, and cross-chain balance state.

It’s this unenviable orchestration that I was referring to earlier, one that accrues value to those who can carry it out. Whoever runs the infrastructure that keeps a fund’s authoritative state consistent across chains becomes hard to replace. While the fund administrator still holds the clock and the chain holds composability, a single player in the middle has to make both possible at once.

The most fragile part of moving assets is accounting for assets in flight.

When an asset is moving between chains, it can temporarily fall outside the fund’s visible balance sheet. Centrifuge V3 issues tokenised acknowledgements for in-flight assets, so the fund’s balance sheet remains continuous even while the underlying token is in transit. It’s the on-chain equivalent of trade-date accounting. Although boring, but essential.

Why should an institutional investor consider tokenised funds despite these conflicts?

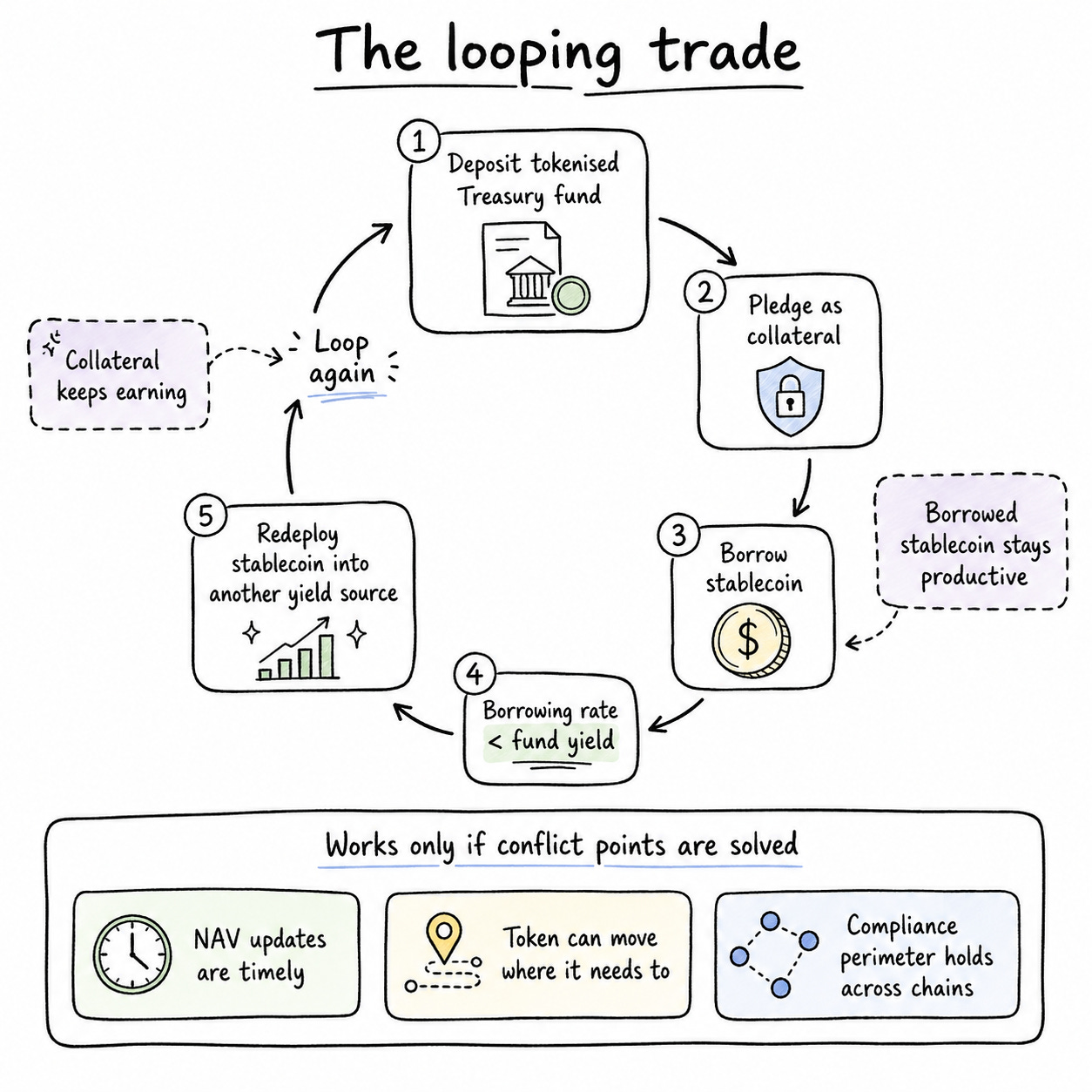

One of the biggest optimisations of idle cash via tokenisation is the looping trade. A treasurer can deposit a tokenised Treasury fund and pledge it as collateral to borrow stablecoin. If the borrowing rate is below the fund’s yield, the position pays the treasurer to hold it. They can then redeploy the stablecoin funds into another yield source and repeat the cycle.

The entire looping trade works only if the above conflict points are addressed. That’s the next challenge facing those building the infrastructure for tokenisation. These points of conflict have been exploited in the past. For instance, if the on-chain NAV price remains stale on smaller tokenised products for even two to four hours and lags the underlying asset, it creates arbitrage opportunities before the next NAV strike.

Redemption-gate collisions can happen when off-chain NAV triggers a liquidity limit, while independent on-chain smart contracts attempt to process token redemptions instantly. This could leave smart contracts holding “orphaned” or unexecuted token transactions that attempt to continuously execute simultaneously against the off-chain cap.

Giant private credit funds and business development companies (BDCs) are currently experiencing this. Two weeks ago, Apollo Global’s $26 billion private credit fund, Apollo Debt Solutions (ADS), had to curb redemptions at 5% of its shares after investors sought to withdraw approximately 16.8% of the total. If such an instance occurred for a fund with a tokenised version trading simultaneously, a redemption-gate collision would be hard to dismiss. In the second quarter, investors requested $15.6 billion in withdrawals from widely held private-credit funds, up from roughly $13.9 billion in the prior quarter.

Cross-chain messages can fail mid-flight, leaving positions half-settled. Trust from institutional allocators will have to be earned when each of these failure modes is monitored and accountable to someone with a licence.

If tokenisation needs to scale to the potential it shows, this is what it will have to deal with. It’s not merely about putting US Treasuries on a blockchain or creating a new asset class. Those building the infrastructure will have to end the archaic rule that forces investors to choose among yield, liquidity, and mobility. If tokenisation offers a way to make a dollar do more than one job at once without compromising on the credibility that comes with the guardrails, then the institutions running billions in cash are definitely going to notice.

I wrote last week about how SWIFT, as an orchestration layer today, is more valuable and powerful than the parties on both sides of the network it serves. How Visa is more valuable than every bank it serves worldwide, except J.P. Morgan.

Read: Who Captures Value in Web 2.5?

This is the incentive for being the orchestration layer in the evolving world of finance. It offers the player a seat at the table for the next decade of capital markets. Centrifuge is defining what the fund side of that seat looks like, and LayerZero is laying its hands on the connective layer between chains.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.