Hello,

For most of financial history, moving money was the hard part. The friction was in making the payment from point A to point B, involving a chain of banks, each of which took a cut. Sometimes it involved moving money across a border.

In the past decade, crypto and stablecoins promised to minimise these frictions through crypto apps and wallets. But these fast, low-cost transfers are of no good if that money is not usable in the broader economy. A dollar stuck in some crypto wallet is worth less than a dollar. This is why crypto is now assuming the role of better infrastructure for moving existing traditional assets.

This convergence of the old and new financial worlds has created a new orchestration layer, in between, where the value accrues. In today’s piece, I explore who captures value in this new layer.

On to the story…

The Need for Web 2.5

The crypto industry has spent over a decade convincing people to download wallets, bridge assets between blockchains, and hold their money in new apps. But people don’t leave the systems they’ve known and used for decades just for something new. No supplier would want to receive their payment over blockchain just to see it sit in their wallets while they figure out how to swap it back into dollars in a bank account that they can actually use for general purposes. Moving money from a wallet to a bank account costs a fee and requires a compliance check in most cases.

The problem was never crypto’s ability to move money in seconds. It was that the crypto’s architecture expected people to leave the systems they already used, like their bank accounts, credit cards and payroll, and switch to a new system altogether. On-ramps, off-ramps, and bridging solutions are frictions meant to be hidden beneath the surface and not features to be flaunted. People will always adopt new technologies that move the money they already have faster and cheaper, in the accounts they already use.

An ideal infrastructure is one in which crypto serves as an efficient, invisible enabler and substrate for traditional finance. We call that sweet spot ‘Web 2.5’. Although the term might sound clumsy, the idea behind it is to have the best of both worlds. We retain the good parts of traditional finance. Think regulations, licence, verification and the UI & UX that people already trust and use. We then marry it with the cheap, programmable, always-on settlement that crypto enables. Neither side has to become the other. The bank stays a bank, while the crypto offers a facelift to the old, dilapidated infrastructure that moved money at a snail’s pace.

But if crypto becomes an invisible substrate and traditional finance stays the familiar surface, where does the value now accrue in this new world of Web 2.5?

The layer that connects two large financial systems has historically been worth more than most of the institutions it connects. Visa earned $24 billion in operating margin last year (FY ending September 2025) by charging just a fraction of a per cent on every transaction that it processed on its network. That’s still a 60% operating margin. The Depository Trust & Clearing Corporation (DTCC), which is now building its own on-chain settlement chain, earned $2.9 billion in 2025 on $4.7 quadrillion worth of securities transactions it processed.

The Layer in Between

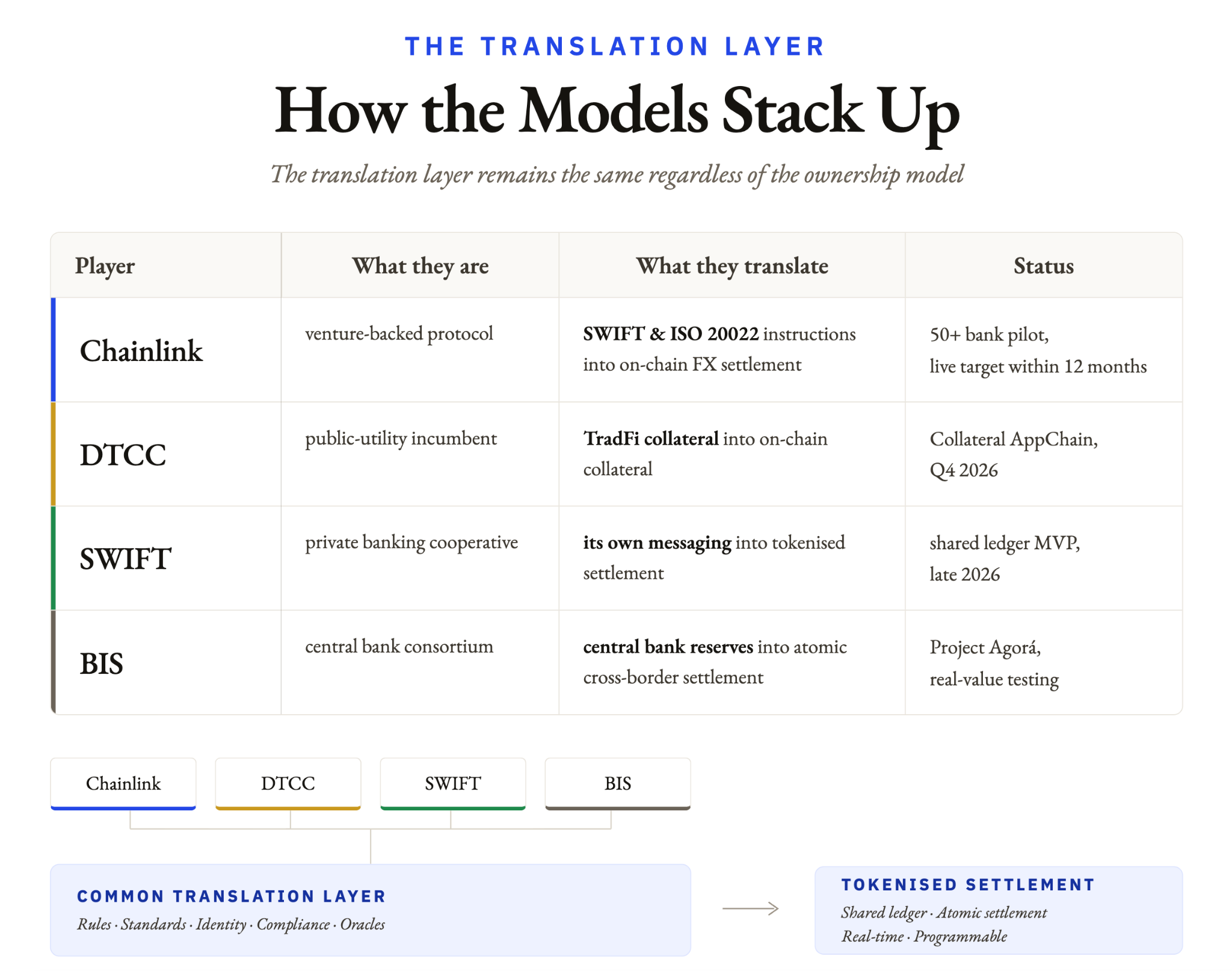

Institutions on both sides are now building translation layers that let banks keep their infrastructure while converting ISO 20022 instructions into on-chain settlement.

On June 23, Chainlink and a consortium of more than 50 European and Korean banks, with roughly $10 trillion in assets among them, announced Project Pangea to test the real-time settlement of foreign-currency trades.

The aim is to transition the FX settlement infrastructure from a traditional T+2 cycle to a real-time T+0 model.

Chainlink’s Runtime Environment (CRE) serves as the orchestration layer, connecting blockchains and other external payment systems without requiring manual routing or bridging. It takes each conventional instruction, turns it into an atomic on-chain swap, and hands back the result that the bank’s systems can read.

Chainlink is a relative newcomer. Yet the DTCC, the 50-year-old institution at the centre of American markets that processed approximately $4.7 quadrillion in securities transactions last year, chose the same Chainlink runtime to power its Collateral AppChain.

On the legacy institutional front, there is SWIFT. By every early crypto prediction, SWIFT is the institution that blockchain was supposed to kill. Many predicted the stablecoins would route around the messaging monopoly. Eight years back, the same global messaging network for banks had called blockchain “not ready for mainstream use”. Instead, SWIFT is building its own blockchain-based shared ledger with more than 40 banks.

This is not a replacement for SWIFT’s network but an orchestration layer that sits on top of it. Money moving on-chain was never the threat. For SWIFT, the concern was being cut out of the layer that decides how money moves on-chain. As long as it has a presence and a say in deciding how that happens, it remains in the game. So it is building that layer itself.

Even sovereign players are rushing to capture value on this layer. The Bank for International Settlements (BIS) has convened Project Agorá with seven central banks and over 40 private institutions to test atomic settlement using tokenised central bank reserves.

Read: Meet Me at the Agorá

But what’s really the value in orchestrating the layer between two financial and/or banking giants?

The Value of the Bridge

The translation layer that merely lets the parties on both sides talk to each other could very well prove more valuable than the players themselves.

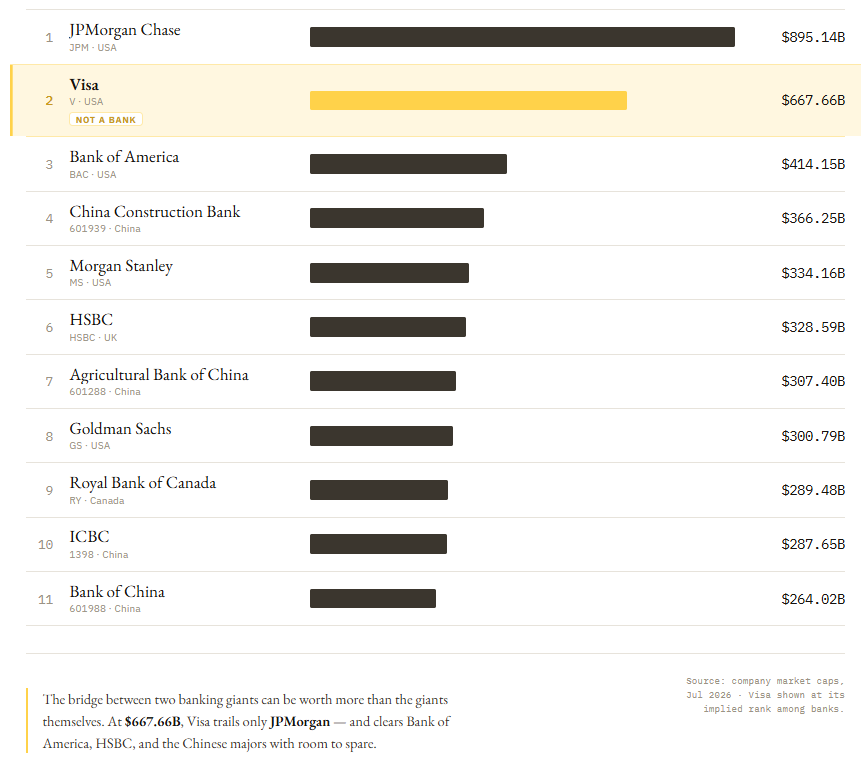

Visa and Mastercard began as routing networks between banks and merchants. Even today, they hold no deposits, don’t issue any cards and underwrite no risk. Yet, Visa is worth more than every bank on earth except JPMorgan.

Operating the translation layer offers more than just monetary value. Those who decide how the money flows can also decide when to shut that route.

SWIFT began in 1973 as nothing more than a way for banks to send each other standardised messages. Fifty years later, it is as powerful to impose sanctions on nations. In the past decade, SWIFT has assumed its role in economic warfare by imposing sanctions on Russia for its war in Ukraine. It even imposed EU sanctions on Iranian banks to counter the country’s nuclear programme and consequently relaxed them after developments around the nuclear agreement took place.

The addressable pool for real-time settlement of foreign exchange transactions that Chainlink is now piloting with Project Pangea is significant.

Cross-border payments range between $150-$190 trillion annually and are projected to cross $250 trillion by 2030. If Chainlink can capture even 1% of these projections along with the consortium of 50 banks it has collaborated with, then it could imply a total addressable market (TAM) of over $1.5 trillion. Even a 0.1% fee on this TAM could translate to $1.5 billion in income by simply orchestrating the layer between traditional finance and on-chain settlement.

But there’s a caveat here. Both SWIFT and Visa became the dominant single standard in their respective layers, where the whole system eventually had to adopt them. It was a case of one winner in each layer, reinforcing its position over decades.

Now, we have four different models - a protocol, a market utility, a banking cooperative and a central bank club, racing for the same single translation layer that bridges the financial worlds of Web 2.0 and Web 3.0.

Permission and Float

The economics driving value beneath this layer are old. When technologies that move money improve, processing transactions always becomes a commodity. As it becomes cheaper to move money, the value to capture then pools in two different places. The first is permission, which lies with those who decide whether a transaction may proceed and under what conditions. The second is float, which is the interest earned on balances sitting idle while they wait to move.

We have written about how this plays out when AI agents pay each other, here and here. The same logic now scales up to settlement between banks.

This is what makes the orchestration layer in between worth fighting for. It develops a two-sided network effect. The more banks plug in on one side, the more attractive it becomes to settlement venues on the other, and vice versa. Every institution that joins raises the cost of leaving for everyone already inside. While individual banks and blockchains compete with each other, the one that orchestrates the translation layer serves them all and earns a fee from each.

Stripe followed this exact playbook on card payments. It hid an ugly tangle of processors, acquirers and payment networks by allowing businesses of any size to easily accept and manage online payments through a simple, developer-friendly set of APIs. It then charged all its users a fee to remove the friction and tuck it away in the background.

This is what makes the connecting layer a hot target for acquisitions. Once someone builds this layer, others would rather buy it than rebuild from scratch. We saw it more than five years ago when Visa agreed to pay $5.3 billion for Plaid. Although the deal was thwarted by an antitrust suit from the Justice Department, the intent behind the attempted deal is well documented. Visa was attempting to buy a position in the market where Plaid operated the layer that wired thousands of fintech apps into bank accounts.

The New World of Web 2.5

The world of Web 2.5 is more promising than the utopian vision of a decentralised-only Web 3.0 alternative because it doesn’t ask capital to flee incumbent players in search of what crypto offers. Instead, it uses crypto as the underlying, more efficient infrastructure to move money and assets within the existing ecosystem.

Although the bank-side projects, including Pangea, DTCC’s AppChain, and Agorá, are still in pre-production, what makes us bullish is the direction that players like Chainlink have taken. For a long time, the echo chambers of crypto kept arguing about how to build a better crypto app to move users away from their traditional alternatives. Builders kept arguing over which blockchain offered the lowest gas fees and which token was best for parking funds. Web 2.5 makes this argument redundant by stripping away all the jargon and hiding the infrastructure in the background.

The internet we use is just data packets of information transmitted over a global network of computers. This is a nice-to-know fact, but not knowledge worth flaunting when all you want to do is use the internet. Nobody cares whether the technology powering the lightning-fast, low-cost transactions underneath is crypto or otherwise.

Blockchains are getting commoditised as an interchangeable, invisible, low-margin part of a transaction. The value now pools one layer up in the business of making money spendable in new places and having a say in whether and how that money should move.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.