Hello,

For over a decade, Bitcoin miners faced a lot of flak in the energy and technology world. Their humongous power consumption drew congressional hearings, ESG downgrades, and sustained public criticism. The same facilities are now signing 15-year lease deals with the likes of Microsoft, Google, and Anthropic. Little about the sites has changed. In fact, if there’s one thing consistent with these miners in the past decade, then it’s the crisis. So, what happened?

There’s an interesting quote on crisis: ‘The best opportunities often come from the worst crisis.’ That’s what has happened with Bitcoin miners. Between July 2016 and April 2024, they faced three halvings. Each one cut block rewards in half and forced operators to chase cheaper electricity across increasingly remote corners of the American grid, including West Texas, rural Georgia and the plains of North Dakota.

The weak ones died. Some pivoted at the right time. Others learned the lesson later.

In today’s story, I will explain how the surge in AI infrastructure investment coincided with miners’ growing power and processing capabilities, helping them find a new lease of life.

Onto the story now,

Prathik

Halving - The First Pivot

BTC miners’ first test of survival came in April 2024 with the most recent bitcoin halving. Every halving event is a stress test. But with each one, the rewards get halved, and the struggle doubles.

The April 2024 halving cut block rewards from 6.25 to 3.125 BTC. In a week after the most recent halving, hashprice had fallen from $0.12 per terahash to $0.047. Hashrate is the revenue miners expect to earn per unit of computing power. By Q1 2026, it hit a five-year low of $0.023 per terahash per day.

The average cost to produce one bitcoin currently stands at ~$81,000. The all-in cost of mining each BTC will go far above $115,000 once you include other non-production costs that these listed miners have to spend to keep the lights on. Bitcoin is trading at $70,760. Its price has never crossed $80,000 in the last three months. You do the math.

The BTC mining industry is left chasing lower mining costs for a commodity whose price it has no control over.

The financial statements of the miners that made most of their revenue by pocketing the difference between mining a BTC and selling it in the open market suddenly went into the red. So they switched to mining and holding the mined BTC. The idea was to wait for the price to appreciate enough for them to make a positive return on the same.

That strategy worked until the bitcoin price rallied. But markets move in cycles. Every bull rally will have its bear phase and correction. Crypto has its cycles, too.

10/10 - The Second Pivot

October 10, 2025: the dreaded date in the crypto industry, which witnessed the largest crypto liquidation ever recorded. With the cryptocurrency prices seeing record-level drawdowns since that event, the bear cycle began. That led to the unravelling of miners’ ‘mine and hold’ strategy.

Some were left second-guessing whether to change their strategy. But others announced pivots within 24 hours of the liquidation event.

On October 11, Bernstein published a report that reframed Bitcoin miners not as producers of hashrate but as holders of gigawatts of secured grid access. The analysts called the miners “key in the AI value chain”. They named IREN (formerly Iris Energy) as their top pick to make a successful pivot from BTC mining to an AI-focused cloud infrastructure provider.

Galaxy Digital, a digital assets leader and AI infrastructure provider, announced it had raised $460 million to convert its Helios mining facility in Texas into a high-performance computing (HPC) campus for CoreWeave on a 15-year lease, with projected annual revenue exceeding $1 billion.

Read: From Volatility to Predictability 💰

What followed the 10/10 event was a systematic liquidation of the balance sheets that had defined the sector’s identity with a ‘mine and hold’ strategy. Miners had spent at least 18 months accumulating BTC as a treasury asset, treating unsold BTC as a signal of confidence.

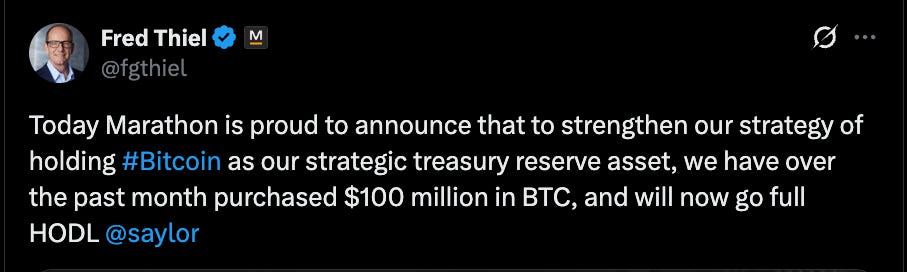

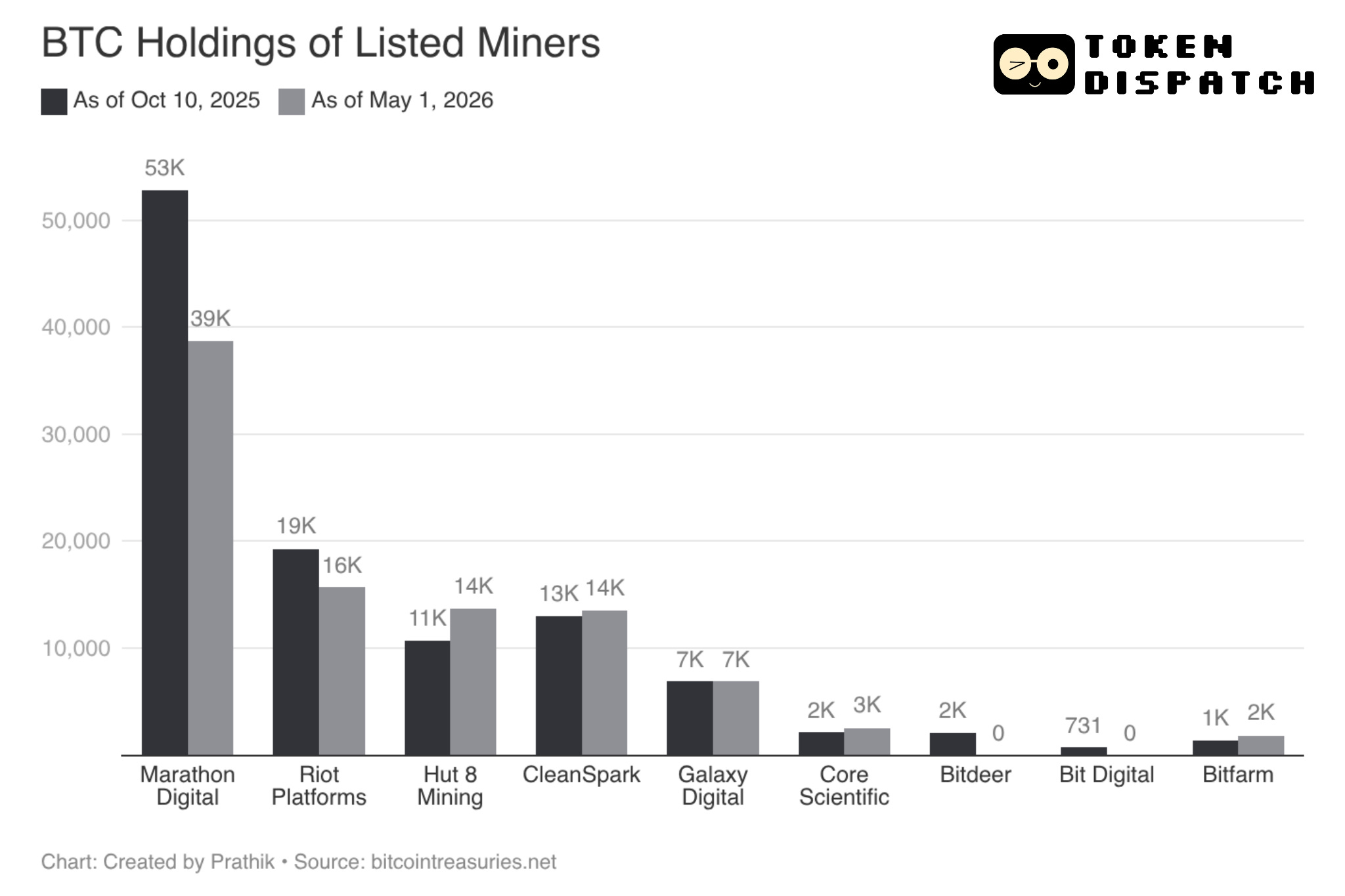

That stance was cracking under the weight of a bear market that saw BTC’s price fall ~40% from its all-time high of ~$126,000 in 45 days. Listed miners who had never sold BTC before started doing so. Marathon Digital (MARA), the third-largest listed BTC holder in the U.S., broke its streak of holding BTC by selling 15,133 BTC in three weeks.

This is the same company whose CEO consistently supported and took inspiration from Strategy, the largest corporate BTC treasury. Less than two years ago, MARA’s CEO and Chairman, Fred Thiel, announced that BTC would be their strategic treasury reserve asset.

Just last month, the Fred took a 180-degree turn and admitted that the selling of BTC “enhances financial flexibility and increases strategic optionality as we expand beyond pure-play bitcoin mining into digital energy and AI/HPC infrastructure.”

I wouldn’t blame him, though. Tough times call for tough calls. And MARA isn’t the only one to make such a pivot away from holding BTC forever as their strategy asset.

Although some added more BTC to their treasuries after the liquidation event, others reduced the pace of BTC additions or made public comments indicating they no longer treated BTC as their strategic treasury asset.

Bitfarms’ CEO was straightforward in admitting, “We are no longer a Bitcoin company.” Ben Gagnon added that Bitfarms will focus on “building the infrastructure for the compute of the future.” CleanSpark took a different approach, treating its 13,000-plus BTC as productive capital and layering covered calls against it.

Even if BTC was not vanishing off their balance sheets, they were identifying it as a resource to strategically fuel their infrastructure pivot.

A Blessing in Disguise

Repurposing a BTC mining site to AI-ready infrastructure is not a simple affair. It costs $8–11 million per megawatt, including new liquid cooling systems, Tier-3 power redundancy, high-bandwidth fibre, and the networking overhauls that GPU training clusters demand.

Yet, mining infrastructure, including cooling, power, and compute capabilities, came closer than any other industry to meeting the requirements of the AI and data centre industries. Bernstein analysts wrote in their note that miners’ existing infrastructure could cut deployment timelines by up to 75%.

It wasn’t just analysts who felt so. This is evident in the deals these miners were able to close over the last few months.

IREN signed a $9.7 billion contract with Microsoft for GPU cloud hosting at its Childress, Texas campus, making it the largest single hyperscaler deal by any miner. Hut 8 landed a $7-billion deal with Google-backed Fluidstack and Anthropic. Cipher Mining bagged $8.5 billion worth of contracts with AWS and Fluidstack. By Q4 2025, Core Scientific’s AI colocation (the space rented out for IT equipment in data centres) went up to 39% of its total revenue, up from 9% just four quarters earlier.

The Surprise Moat

But why are hyperscalers paying mining companies, of all people, for data centre space?

Time is the secret sauce. To survive each halving, miners had to chase cheaper electricity. So they did what they had to do to survive. They negotiated long-term utility agreements, acquired industrial land in low-cost energy corridors, built private substations and secured direct grid interconnections. A modern mining facility is equipped with dedicated high-voltage transformation equipment, redundant power feeds, and thermal management systems built to run at full load, around the clock.

Maybe it wasn’t planned, and you’d say the miners just got lucky. But who minds getting lucky and striking gold while struggling for survival?

Public miners now hold approximately 6.3 GW of operational sites with another 2.5 GW under construction. Data centre interconnection queues in the U.S. run 5 to 7 years in most markets. Microsoft’s internal forecasts show its data centre crunch persisting into 2026 and beyond.

This is why hyperscalers are ignoring mining companies’ lack of expertise in AI infrastructure. Instead, they are paying for the substation, the land-use permits, the utility relationships, and the grid connection, all of which take years to secure elsewhere.

There are incremental gains a miner can make by deploying their existing equipment for AI applications. MARA recently announced a $1.5 billion acquisition of energy infrastructure that will bring its total power capacity to over 2.2 GW. This allows it to convert an already-depreciated facility for AI infrastructure with a cost basis that no other AI builder can replicate.

CEO Fred Thiel called the assets ready-made infrastructure that would have taken up to 10 years and $2bn–$3bn to assemble independently. “Power is the scarce input in AI and, with the planned addition of Long Ridge Energy, we are gaining control of a highly efficient, contracted energy platform,” he said.

The Closing Window

There’s a catch in this story. Every megawatt of energy diverted from Bitcoin mining to AI infrastructure subsidises the economics of whoever remains behind in BTC mining. It reduces the difficulty of mining, making it cheaper for BTC miners to mine a block.

There might still be those who choose to swap or reserve some of their equipment for BTC mining when it does get cheaper. But that’s exclusive for those who can afford to swap or set aside equipment for mining. It won’t be everybody’s play. That’s also because those who repurpose their mining equipment for AI infrastructure won’t be able to swap it back and forth repeatedly. Mining is an interruptible process. You can shut it down when the electricity charges are high. You cannot do the same for AI and high-performance computing. Once you lease out or commit your computing power, you cannot back out of the deal temporarily to use the equipment to mine some bitcoins.

However, for most miners, this is not an option. They have a short window to make the shift. And they won’t get lucky too often.

The timing of how well everything lined up for them is almost unbelievable. The halving squeezed mining economics to the breaking point. Then came the 10/10 liquidation event, forcing miners to confront the reality that holding BTC through a bear cycle is not a feasible strategy. But the AI infrastructure boom arrived at the exact moment when miners had both the motivation to pivot and the assets to execute the pivot.

This will likely not repeat. The miners signing the contracts today will bear the fruit of a decade of economics that will not be available to whoever comes late to this party.

That’s it for today. I will be back with another deep dive.

Until then, stay curious!

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.