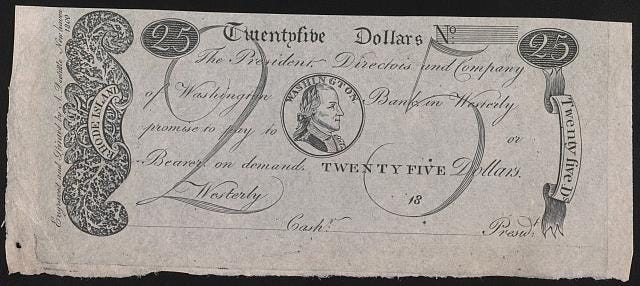

In 1840, a shopkeeper kept a book under the counter. When you paid with a banknote, he pulled out the book and checked what your money was worth that day.

A ten-dollar note from the Bank of Cincinnati was not worth ten dollars everywhere. Maybe nine. It can be any number. Maybe nothing, if the bank had failed and the news hadn’t reached his county yet. The most famous of those books came out of Philadelphia, Bicknell’s Counterfeit Detector, a price list for money itself, reprinted on a schedule because the worth of a dollar changed depending on whose name was on it.

That was America from 1837 to 1863. Any bank with a state charter printed its own notes, and getting that charter was easy. Michigan kicked it off in 1837 by letting you open a bank with barely any requirements, no act of the legislature needed. Thousands of different notes ended up moving around the country at once. Around a third of the paper in circulation was outright counterfeit.

Each note was a bet on the bank behind it. The system died during the Civil War, when the government printed one national dollar, partly to fund the war, but also because trusting eight thousand private dollars had worn the country out.

On June 22, the Senate overwhelmingly voted the 21st Century ROAD to Housing Act (85 to 5), and the House passed it the very next day. Hidden inside this housing bill is a rule that bans the Federal Reserve from creating a CBDC for the public until 2030.

That is why we are looking back, digging up the ghosts of the Free Banking Era.

The dollar in a Venmo balance is a promise from a bank to hand you one, and if that bank dies, your money is at risk past the FDIC line. A CBDC (Central bank digital currency) cuts the bank out. It allows the holder to possess state money directly, digitally.

The Senate killed that idea for two reasons.

A government digital dollar could track every cent you spend and freeze your wallet on command, the way China’s digital yuan already does.

Secondly, the banks fought it hard because money sitting directly at the Fed is money that will never be in their deposits. They’d lose the float their whole business runs on.

Now, even the man holding the pen looks unsure about what he’s signing. On June 24, an hour before the signing, Trump cancelled the ceremony and demanded a voter-ID bill the Senate had already killed. The ban likely becomes law anyway.

Fine, the government won’t mint a digital dollar. At the same time, it hands the job to private firms instead. That means 1840 walks back in the door.

Even now, with the GENIUS Act signed in July 2025, the bar is mostly about reserve quality, rather than hard gatekeeping. More than a dozen firms are lining up for charters to print their own dollar. Every fintech wants a branded coin.

The market is about $312 billion now. Tether’s USDT and Circle’s USDC are roughly 80% of it. Then PayPal’s PYUSD, Ripple’s RLUSD, and Paxos minting white-label coins for whoever wants one. Each one says the same thing the Bank of Cincinnati said. Trust us, it’s backed.

It’s not 1840, and Jim Carrey is out here struggling to prove he isn’t his own clone. We believe in nothing. Do we? Which is good and bad. The distrust is what makes issuers prove their backing, and also what they’re counting on staying shallow, since a crowd that suspects everything but verifies nothing is exactly the crowd you can hand a private dollar to.

A wildcat bank said its notes were backed by silver in the vault. The vault was often a barrel of nails parked in the woods where no inspector could reach it. A stablecoin backs its tokens with US Treasuries and posts the receipts every month. On the collateral, that is a big difference, and it runs in the stablecoin’s favour.

Leave the collateral part aside, and then we have a problem. A dollar equals a dollar because everyone agrees on three things at once. The issuer is good for it. The reserve is real, and you can reach it. And if the thing starts to tip, someone catches it. Hold all that together, and a dollar is just a dollar, and you stop thinking about it.

When one of them wobbles, money gets priced issuer by issuer, the way it was in 1840. It is how money works.

Even the checking account works on the same principles. The government underwrites all three at once, so you don’t see it. Stablecoins are where you can watch the machine with its cover off.

Tether is the largest issuer in the world and the least transparent. Its reserve reports have been picked apart for years. It settled with the New York Attorney General in 2021 and admitted it did not always fully back its reserves the way it claimed. It had been lending billions of its backing to affiliated companies. Circle is the good guy, the regulator’s pet. It is audited monthly and has been public since 2025. But then what happened in March 2023? Circle had $3.3 billion of USDC reserves frozen inside Silicon Valley Bank when SVB collapsed. USDC dropped to 87 cents over the weekend until the government backstopped SVB’s deposits. Good reserves, and yet, one dollar was worth 87 cents for about 60 hours. Because what cracked was the belief that it was reachable.

Every name in payments now wants its own dollar. PayPal has PYUSD. Ripple has RLUSD. There’s USDG, run by a consortium, plus a wave of bank tokens coming from the likes of JPMorgan and Western Union. In December 2025, the OCC handed trust-bank charters to Circle, Paxos, and three other crypto firms, and the line behind them is long. Tether, shut out as a foreign issuer, spun up a separate US coin called USAT just to get back through the door.

Read: Charters, Keys, and Control 🔐 - by Prathik Desai

Read the words on the tin, though. These are “trust bank” charters, not insured-bank charters. The Fed is holding out stripped-down accounts for them that don’t have overdrafts and don’t have access to the emergency lending window, which is the thing that actually saves a bank when the run starts.

And the names you’re handing the money to have records.

Paxos, the company issuing PYUSD and a half-dozen other branded coins, was ordered by New York’s regulator to stop minting Binance’s stablecoin back in 2023. Some of the newer tokens aren’t even backed by cash. Ethena’s USDe leans on a derivatives trading strategy to hold its peg.

The Act bars these issuers from paying you interest, so they route around it. Coinbase pays “rewards” on USDC. PayPal dangles 3.7% on PYUSD. The yield reels your money in. Unlike standard bank accounts, which are backed by FDIC insurance, this money has zero safety net.

Since stablecoins back their tokens with US Treasuries, Washington still sets the money supply. The interest on those Treasuries flows to the issuers. Tether cleared around $10 billion in profit in 2025 with about 100 employees and holds more US Treasuries than Germany does.

But if it all goes bust, the loss is all yours. A run is when everyone leaves at once through a door meant for a trickle. Stablecoin redemption is a narrow door. Most people can’t redeem with Tether at all. They sell to a handful of arbitragers, and Tether averages around six a month, with a $100,000 minimum to redeem at the source.

If Tether breaks tomorrow, a hundred billion in tokens reprice to 0. Tether owns so many of the Treasuries that when it panics and dumps them, it shakes the Treasury market itself.

Washington steps in because the alternative is a coordinated credit and liquidity freeze.

And the government doesn’t even need a global meltdown to do it. It saved Lockheed in 1971 with a $250 million loan guarantee, over a tie-breaking vote, to protect 60,000 jobs and the Pentagon’s biggest supplier. An admiral watching it happen called it “a new philosophy where we privatise profits and socialise losses.”

When Penn Central, the country’s largest railroad, collapsed in 1970, the government let the company die and then spent public money building Conrail to absorb the tracks anyway, because the trains had to run.

A dollar token used as money by 250 million people clears that bar with ease. The state has a long history of refusing to guarantee private risk right up until the private risk threatens to disrupt public infrastructure.

There are ways to close this. What if, instead of a bank like SVB, which can collapse, they make the reserves of the issuers park directly at the Fed? The risk of a run largely disappears because the Fed can’t fail like a regional bank can. Or make them buy real deposit-style insurance, funded by the issuers, so the backstop is paid for before the crisis.

The government could try to tax the yield on the Treasury they earn on public debt and return it to the public that bears the risk.

But we would hate all of these, wouldn’t we? Reserves at the Fed mean the Fed is now the backstop. Insurance means a government insurer standing behind it, the way the FDIC leans on the Treasury when things get bad enough. Taxing the yield means treating these firms as public utilities. We don’t want to drag the government back into the middle of the money. That’s why the ban on CBDCs in the first place.

Going back to human history again, in the Athens marketplace around 375 BC, the city paid a public slave to sit among the bankers’ tables and decide whether your silver was real. He cut the plated fakes in half and handed the good coins back. He even waved through foreign knockoffs of the Athenian owl, as long as the silver was solid, and a law forced every merchant to take whatever he approved.

Twenty-four centuries later, have we arrived right there? The pleasing answer is that big shifts always come with holes, which get filled with time. Maybe give it a decade for the reserves to get cleaner, the rules get teeth.

But the trade-off here is what you want to look at.

Look at what you’d be giving up. Right now, your dollar sits behind FDIC insurance and a Federal Reserve that can print its way out of a panic. It is slow and one of the most backstopped things you will ever hold. The bank lent it out the day it landed. The Fed dropped reserve requirements to zero in 2020, so by law your bank doesn’t have to keep a single cent of your money on hand. What stands behind it is FDIC insurance, and that fund holds about $154 billion against the country’s insured deposits. Round it out, and that’s roughly a penny and a half set aside for every dollar it promises to cover. It still cannot handle a synchronised, systemic panic. If the fund is wiped out, the FDIC must immediately activate its backup line of credit with the U.S. Treasury or coordinate with the Federal Reserve to print emergency liquidity.

In a single month of 2023, three of the biggest bank failures in American history hit at once, Silicon Valley, Signature, First Republic. To stop the run, regulators tore up their own $250,000 insurance cap and made every uninsured depositor whole, the exact emergency move they’d run for a stablecoin. It cost the fund about $20 billion.

Stablecoins are cheap and fast. They are open all night, and the reserves sit in Treasuries you can watch on-chain, and the best issuers post the receipts every month, which is more than the bank reveals about where the deposit went.

Would you swap the first for the second?

I would, without thinking twice. Maybe you would too. You read this article, you already live in this stuff, you know what a depeg is and where to look when one starts. But the test is on normies. The person is getting paid in USDC because it’s the easiest dollar they can hold. The shop is taking PYUSD because the fee is lower. Most people never read the risks behind an easy system.

After all, the convenience spreads faster than the understanding does.

Your money is only as good as its issuer, and the issuer is only as good as the state that agrees to stand behind it.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.