Are monopolies for structures built by men? I want to convince you that it’s laws of nature. Black holes, in which the mass creates gravity, density pulls in surrounding matter, and eventually the system becomes entirely inescapable.

We look at a giant in any industry and see a failure of antitrust law. That view is shallow. Midnight brainrot, maybe, but look at it like gravity, functioning perfectly.

A massive system creates an inevitable pull. In physics, matter attracts matter. In markets, volume attracts volume. This is why tearing down a monopoly by force rarely works. You can partition the entity and declare the market free, but you cannot legislate away the physics. The broken fragments still feel the original pull. They float in the same space under identical economic pressures, destined to fuse back together.

How do you destroy a black hole? The gravity remains. Yeah, I just watched Interstellar for the 9th time.

Standard Oil controlled 91% of US oil refining by 1904. The government broke it into 34 companies in 1911. Within a decade, several of those pieces, such as Standard Oil of New Jersey and Standard Oil of New York, had grown back into giants on their own.

Exxon and Mobil, two of the biggest companies in the world, a century later, both trace directly back to that breakup.

Sometimes breaking a monopoly just creates the conditions for new ones to grow in its place.

Monopolies in finance and infrastructure are notoriously hard to dent, let alone end. AT&T’s 1984 breakup split the company into seven regional providers. By 2005, AT&T had reassembled most of itself through acquisitions. ‘In 2005, one of the Baby Bells, SBC, absorbed AT&T Corp itself, taking back the brand. The economics had never changed. High startup costs and user networks kept the original monopoly intact.

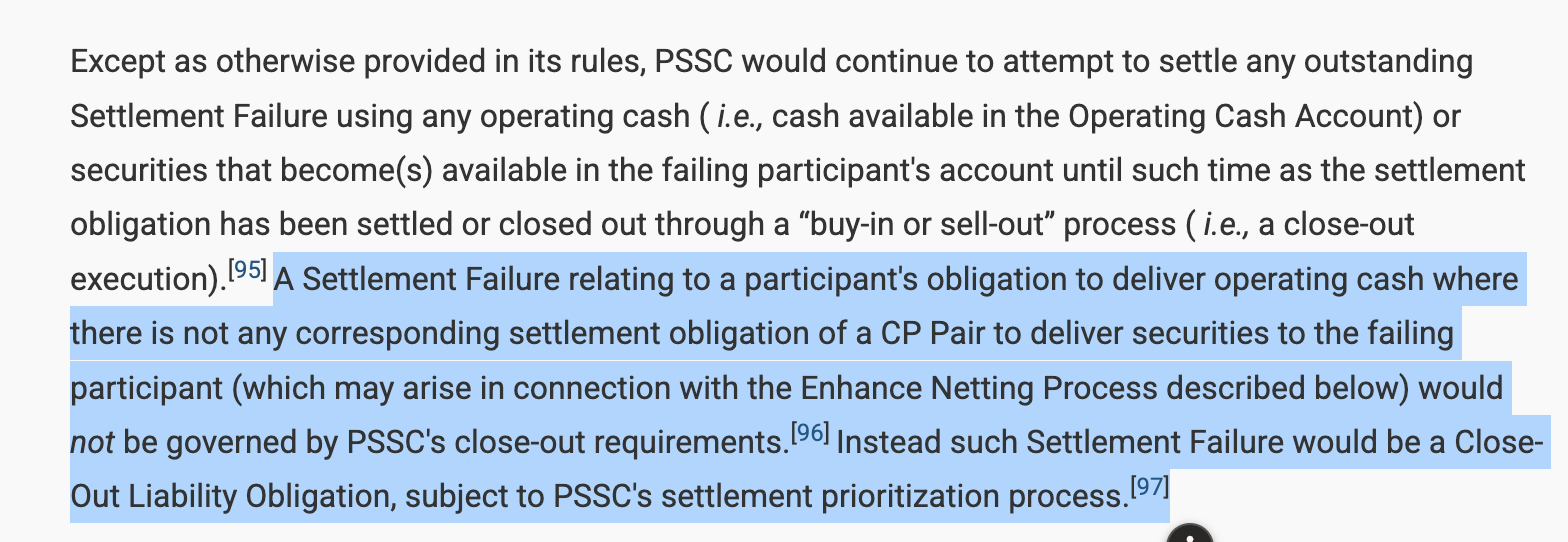

On May 27, 2026, the SEC approved Paxos Securities Settlement Company as a clearing agency. DTCC, through its NSCC and FICC subsidiaries, has been the only securities settlement utility in the United States since the 1970s. The first blockchain-native firm ever approved to provide clearing and settlement services as a central securities depository in the US.

Before we say “monopoly broken.” Now that I’ve read Tim Wu’s The Age of Extraction, I believe that it’s rarely true. How platforms that look unavoidable usually stay that way even after the legal barriers come down, because the barrier was not always the legal ones.

What does Paxos need to actually compete?

The fight comes down to netting. I’ll explain it like you are dumb.

You owe X $100. X owes Y $100. Y owes you $100. Without netting, three payments happen. $300 moves. When we apply netting, everyone realises it’s circular. The net effect is that nobody owes anybody anything, and nothing needs to move.

DTCC does this at the scale of the entire US stock market. Thousands of brokers and banks generate millions of trades per day. If Goldman Sachs buys 10,000 Apple shares and sells 9,000 shares on the same day, DTCC completely ignores those 19,000 individual movements. Goldman is a net buyer of 1,000 shares. Only that final balance settles, because… netting.

DTCC’s equities clearing arm processes 214 million broker-to-broker transactions daily, worth $2.08 trillion. DTCC’s own language is blunt about the alternative. Without netting, the company says, ‘trillions of dollars in cash and securities must move through the financial system on a continual basis throughout the trading day.’ Multilateral netting is what prevents that. DTCC’s own white paper calls it one of the ‘enormous benefits’ that any move toward faster settlement has to preserve.

That’s where atomic settlement, the thing Paxos is built on, runs into this.

Atomic settlement means every individual trade settles instantly and all at once. This eliminates counterparty risk because there is no delay between trade and settlement.

But if every trade settles instantly, there’s no chance to net anything. Each trade is a complete transaction, so full value changes hands every time. For example, if Goldman buys 10,000 Apple shares and sells 9,000 instantly, that counts as two transactions. 10,000 shares worth of capital moves one way, then 9,000 shares worth move back. This contrasts with DTCC, which nets the same activity down to 1,000 shares worth of actual movement.

The capital that must be set aside for the total amount, rather than the net amount, cannot be used for anything else. It can’t be lent, invested, or deployed in other ways. For a single trader making a few trades, this is just a minor issue. For a large broker-dealer processing thousands of trades each day with hundreds of counterparties, that idle capital requirement turns into a high cost, even if each individual trade settles more quickly.

Speed per trade versus capital efficiency across the whole book. Different optimisations, and for the big players in the market, the second one might matter more. That’s where they go back to the monopoly.

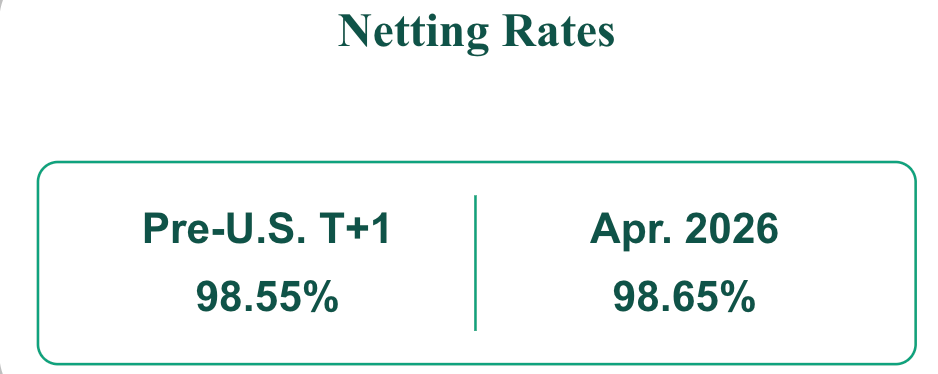

Paxos is well aware of this, too. Multilateral netting is part of their design. In fact, the company has built the platform to support it across any settlement cycle, from T+2 down to intraday. The constraint right now is scale.

Right now, Paxos only nets trades between two direct parties. Multi-party netting (what DTCC does) across the entire market will come later. The SEC’s approval caps initial operations at 10 participants. DTCC nets across thousands. Netting requires a massive volume to work. If only five banks trade with each other, they rarely owe each other matching amounts. Five hundred banks trading together create endless overlapping debts that cancel out perfectly. The big firms that need this efficiency are already hooked on DTCC’s massive network. They hardly have any reason to switch first.

For Paxos to build the netting efficiency that would attract those broker-dealers, it needs the broker-dealers. For broker-dealers to come, netting efficiency needs to already exist.

To make matters more complicated, PSSC’s registration is temporary. It lasts 18 months. Operations will start about 10 months after approval, which means the earliest live activity will be around Q1 2027. The target launch date for the DLT-based clearing agency is “March 2027 at the earliest.”

Can you expect DTCC to remain passive? They raised formal concerns in a comment letter regarding PSSC’s proposed netting plan and its overall recovery strategy. That’s what monopolies do.

Separately, DTCC partnered with the Stellar Development Foundation to put real-world assets on a public blockchain. They plan to tokenise US Treasuries and major stocks, including Russell 1000 equities, on Stellar’s network by the first half of 2027. As the incumbent with a net moat, DTCC is now also building blockchain infrastructure.

So what actually has to go right for Paxos?

Participant count needs to grow well past the initial 10, and it needs broker-dealers with real volume, not just pilot participants testing the rails. Multilateral netting needs to go from “planned” to “live” within that 18-month window, because a temporary registration that can’t demonstrate its core economic claim won’t be renewed. And Paxos needs all of this to happen while DTCC is simultaneously building its own blockchain rails on Stellar.

None of this is impossible. We will see if Paxos can actually break the cycle, or if DTCC’s gravity pulls them right into the centre.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.