Hello,

The RWA tokenisation market (excluding stablecoins) has grown roughly tenfold, in the past three years, from about $5 billion in 2022 to $47 billion today. The BCG report projects that the broader tokenised asset market (including stablecoins) will reach $18.9 trillion by 2033.

The current primary RWA markets include Private Credit, with $20 billion tokenised, and $10 billion in Tokenised Treasury Bills.

However, as I wrote a couple of weeks ago, Hyperliquid has shown that there is strong demand for stocks, ETFs, and metals as well. Perp markets for equity and stocks account for 10-15% of Hyperliquid’s daily volume.

Yet, the tokenised equity market has not grown as significantly. While the total issuance of tokenised Treasuries stands at roughly $9.3 billion, the tokenised equity market is only at $1 billion— an approximately tenfold gap.

Ironically, this relationship reverses when viewed through the lens of traditional market size. The U.S. stock market is estimated at $68 trillion in market capitalisation, while the outstanding stock of the U.S. Treasuries are closer to $30 trillion.

Globally, stock markets are roughly twice the size of government bond markets. Why then has the tokenised stock market not grown as rapidly as the tokenised U.S. Treasury market so far?

For U.S. Treasuries, the characteristics of the assets and their yields are relatively standardised, making on-chain liquidity and tokenisation management easier.

A 6-month T-bill yields roughly the same thing regardless of which platform tokenises it - the underlying asset has a fixed maturity and a credit risk profile that is identical across every issuer because the borrower is always the U.S. government. The asset behaves predictably, and that predictability simplifies everything downstream.

For the tokeniser, this means there is no need for real-time oracle feeds updating every second - a T-bill’s value moves in small, predictable increments based on time to maturity and the prevailing interest rate. Liquidation parameters on lending protocols are straightforward to set because the collateral value doesn’t shift.

For the buyer, standardisation means fungibility across issuers. OUSG from Ondo, BUIDL from BlackRock, and BENJI from Franklin Templeton. While these products differ in fee structure and legal wrapper, the underlying economic exposure is nearly interchangeable. That makes comparison shopping easy and switching costs low.

Stocks, on the other hand, are idiosyncratic. TSLA and AAPL have completely different volatility profiles, dividend schedules, liquidity characteristics, and corporate action risks. Each tokenised stock requires its own oracle feed, its own risk parameters for lending, and its own liquidity pool.

Moreover, the tokenised equity models are fragmented, and there is no one clear answer to the solution as of yet. The uncertainty surrounding the asset class indirectly hinders adoption and development.

On-chain Equity Gradient

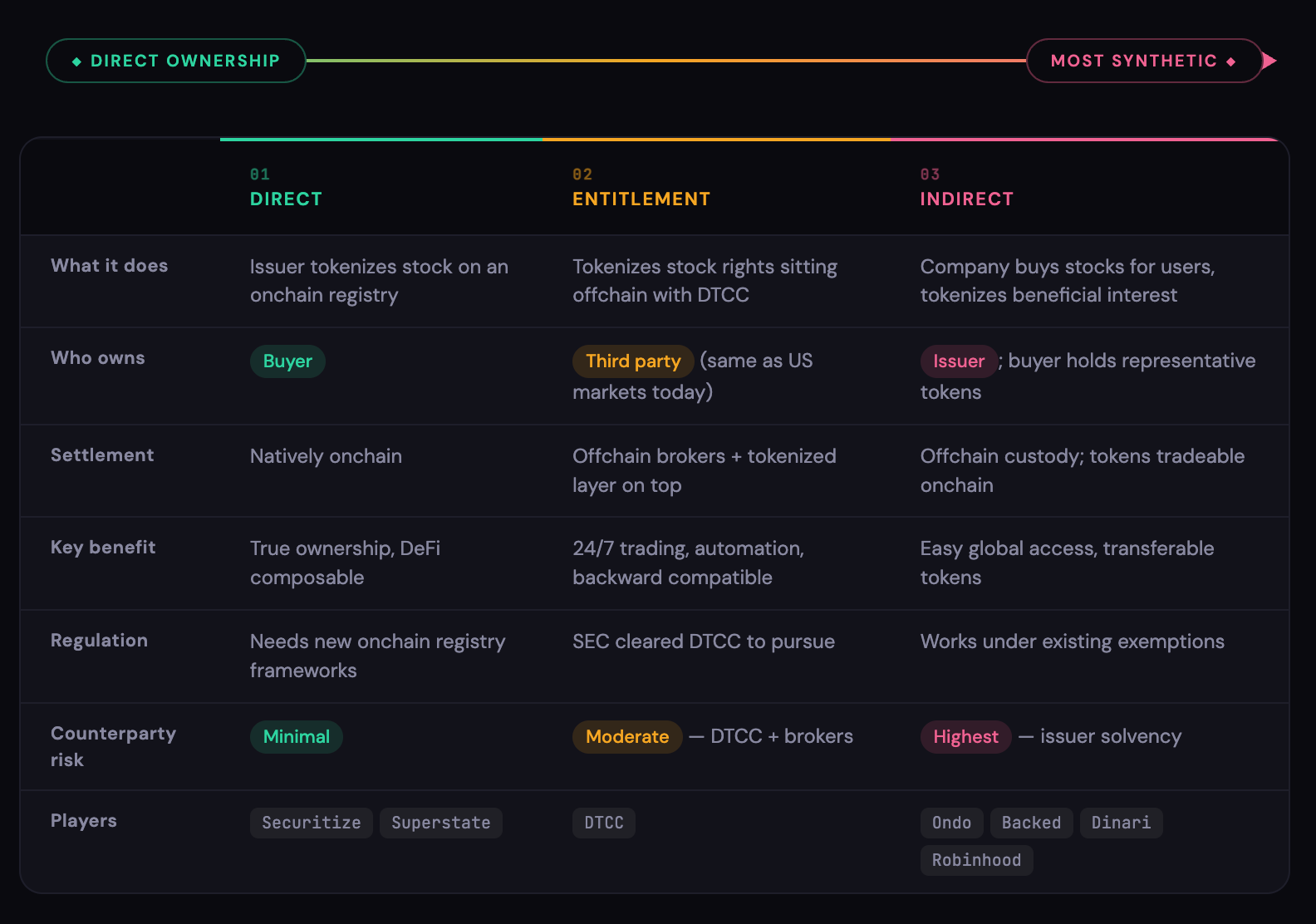

Today, based on the model of issuance, tokenised equities can be put in three different brackets:

Direct Tokenisation: In this model, the issuer directly tokenises stock ownership. The issuer of the token maintains an on-chain registry to demarcate the ownership of the stock. Securitize and Superstate are the companies doing this today.

Entitlement Tokenisation: A method that tokenises stock-related rights that currently sit off-chain with DTCC (Depository Trust & Clearing Corporation). In this, the stock orders still go through a traditional route of off-chain brokers, and the stock ownership lies with a third party instead of the buyer, as happens today in the U.S. stock market. It will improve operations, introduce 24/7 trading and improve the current workflow. DTCC recently got clearance from the SEC to pursue this.

Indirect Tokenisation: In this model, a company buys and holds stocks on behalf of users and tokenises the beneficial interest in them. The representative tokens can be traded and transferred, but the stock ownership lies with the issuer. Companies like Robinhood, Backed Finance, Ondo, and Dinari are currently using this model.

The first two methods, including direct tokenisation through transfer agents like Securitize or Superstate, are tightly coupled to existing U.S. equity issuance infrastructure. That coupling gives buyers something valuable: actual ownership of the underlying shares, complete with voting rights and regulatory protections. But it also imports the constraints that come with U.S. securities law.

For example, selling tokenised U.S. shares to non-U.S. persons would face several restrictions - KYC/AML requirements, broker-dealer licensing in the investor’s home jurisdiction, and geographic gating that limits who can buy and where. While direct tokenisation is legally more robust, that is also precisely why it has a smaller addressable market.

Meanwhile, indirect tokenisation, the model used by Ondo and xStocks, trades away the legal robustness for reach. These tokens don’t represent ownership of the underlying stock. Instead, they’re structured notes issued by an offshore SPV that holds the shares as collateral and passes through the economic exposure, price movements and dividends.

The buyer trusts that the issuer maintains sufficient off-chain collateral to back every token minted on-chain. There’s no guarantee of ownership, no voting rights and no shareholder protections. What the buyer does get is access.

Indirect tokens can be sold on-chain without the restrictions that bind direct issuance. For a non-U.S. retail investor who wants exposure to U.S. equities without a brokerage account, this is currently the most accessible path - and the only one that lets them simultaneously earn dividends and deploy that exposure across DeFi platforms.

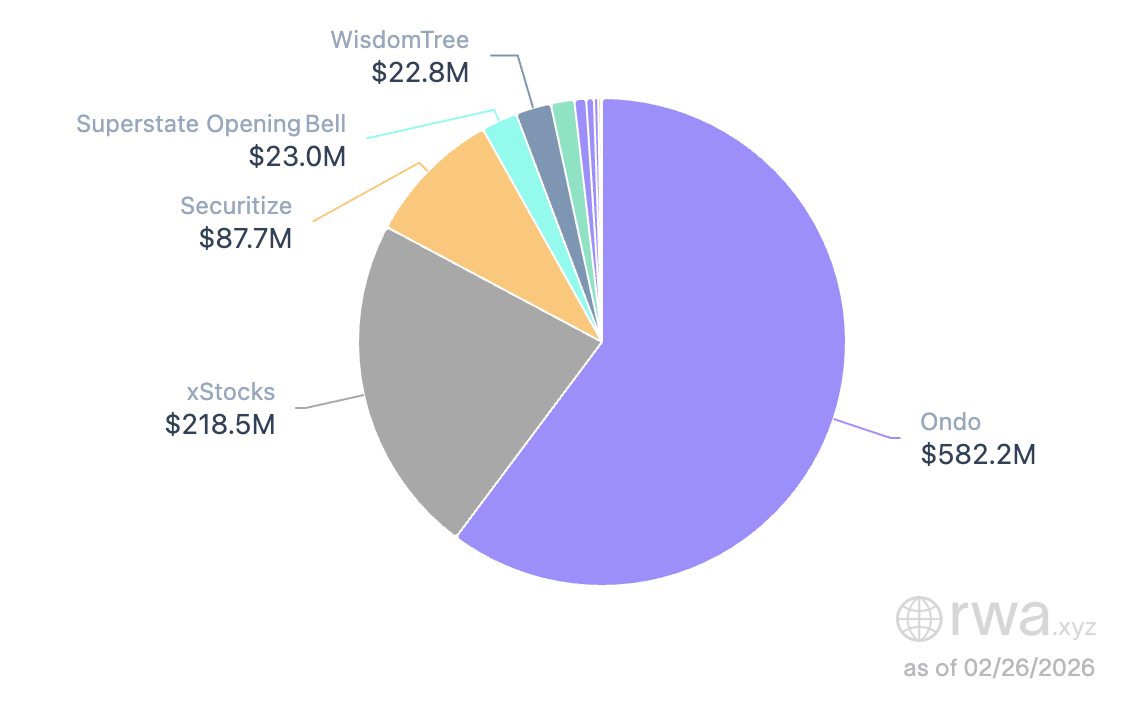

The numbers reflect this dominance: indirect tokenisation controls the majority of the market, with Ondo and xStocks together accounting for over 95% of all tokenised stock value.

Indirect issuers - Ondo and xStocks - together command over 80% of tokenised equity market share today. While these dynamics may shift as regulations clear the path for direct ownership models, Ondo has capitalised on the interim gap, capturing more than 60% of the total market cap alone.

Ondo leveraged two important go-to-market levers to capture the majority market share. First, its infrastructure enables better execution price on-chain and second, its distribution. And that’s what we’ll look at today!

Fast Stocks

The primary distinction between Ondo and xStocks lies in what happens when these tokens drift from the price of the underlying stock.

Market makers ensure tokenised stocks stay pegged to their real-world price through arbitrage. If TSLAon trades at a premium, a market maker mints fresh tokens and sells them into the secondary market. If it trades at a discount, they buy tokens and redeem them.

The economics of this process differ dramatically between the two platforms. Backed charges a 0.50% fee on every mint and redemption. While Ondo doesn’t charge a fee, instead captures a spread - the difference between the price quoted to users and the price at which it executes in the underlying market.

This difference reshapes market maker behaviour. On Backed, an arbitrage opportunity is only profitable when the premium or discount exceeds 50 basis points, the cost of minting or redeeming. And on Ondo, even a 10 basis point deviation is worth closing. This results in tighter spreads, less slippage, and prices that more closely track the underlying asset.

Tighter spreads, in turn, attract more capital, and deeper liquidity makes the tokens more attractive as collateral, which is beneficial for DeFi integrations. It’s a flywheel effect.

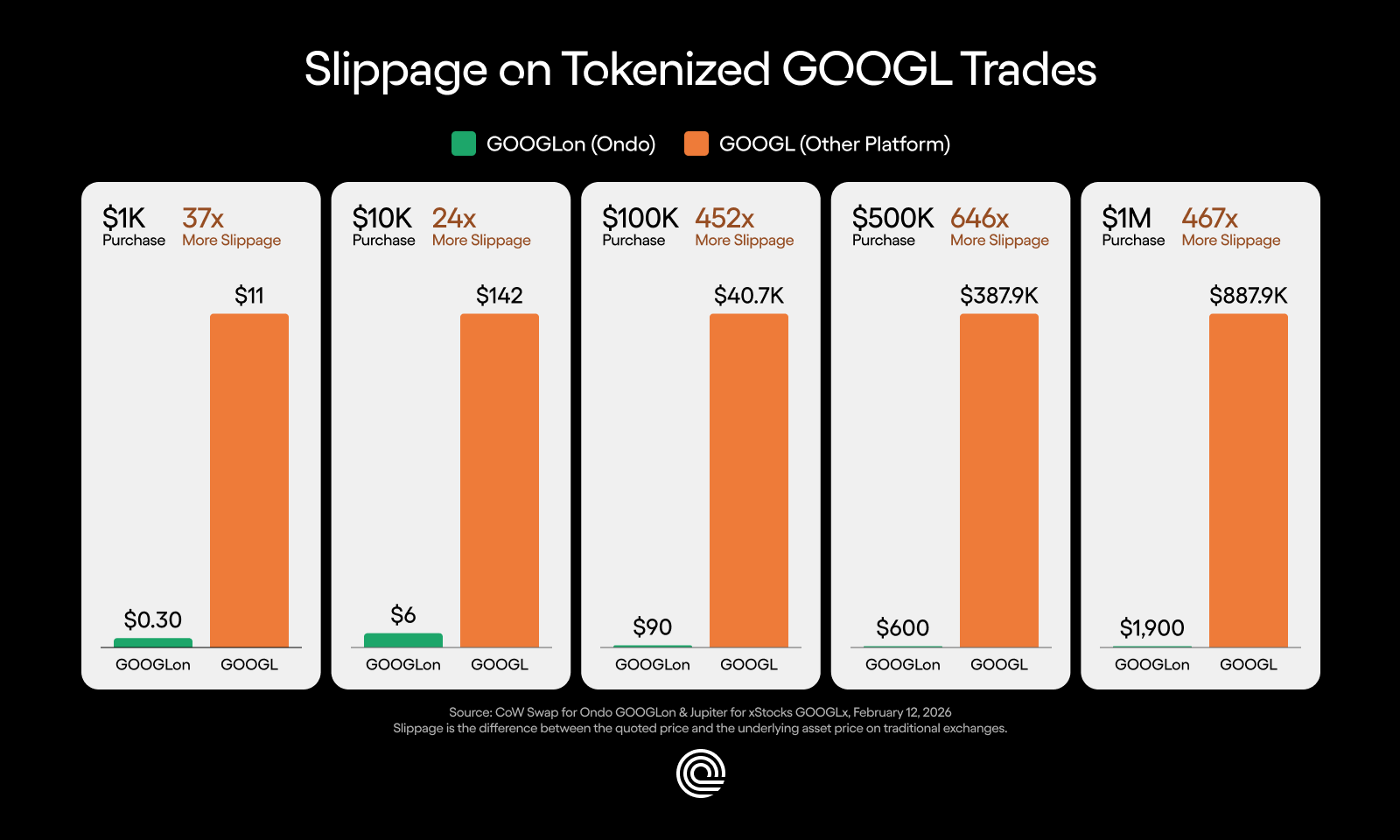

The effects of liquidity and tighter spreads are clear in the graphic posted by the Ondo team, which shows the massive differences in slippage between a GOOGL buy on Ondo’s stock on CowSwap and xStocks on Jupiter (Solana).

Ondo also provides atomic mint and burn functionality for its stocks. The buyer can send USDC and receive tokens in one transaction. While Backed’s process runs through a Jersey-based SPV with settlement up to T+3. For a market maker rebalancing in real time, a latency of 3 days can be deterring.

This helps with on-chain DeFi integrations. As Ondo’s tokens settle instantly, they are much more useful as collateral in DeFi. If a loan is liquidated, the protocol can burn the token and settle the transaction instantly.

Taking it to Retail

Ondo’s other moat is in its distribution strategy. The platform grew to $600 million in TVL within seven months of launch. For context, USDT took approximately three years to reach that milestone, and USDC about eighteen months. What made this possible was an aggressive, multi-surface distribution strategy.

It starts with breadth. Ondo currently offers 200 tokenised stocks across three chains - Ethereum, BNB Chain, and Solana. In comparison, xStocks offers 75, with over 90% of its TVL concentrated on Solana alone.

The breadth of Ondo’s catalogue matters more than it might seem: the top 20 Ondo stocks account for roughly $530 million in TVL, but the remaining 180+ tokens hold another $170 million. That long tail almost matches xStocks’ entire top 20 TVL of $210 million. Investors who arrive for TSLAon stay to build diversified on-chain portfolios; asset selection acts as a capital magnet.

So, where is this TVL concentrated, and who are the traders?

Currently, CEXs account for $8.8 billion of Ondo volume against $2.5 billion on DEXs. Exchanges clearly dominate the trading layer.

BNB has been the core driver for its DEX volumes. Amongst the DEX volumes, BNB Chain drives over 85% of all DEX volume, with 1inch capturing 90% of that flow. The BNB dominance in trading volume is especially interesting as its TVL share is significantly lower.

Ethereum commands 66% of Ondo’s TVL, BNB Chain around 30%, with Solana at a relatively small 3%. Ethereum carries institutional credibility; the lower volumes and higher TVL on Ethereum imply that holders are parking capital, minting stocks and holding long-term equity exposure.

This Ethereum TVL is also the result of Ondo’s existing USDY and OUSG enterprise client TVL on the chain, who just need to click a few extra buttons on the Ondo dashboard to access these assets.

Meanwhile, BNB Chain gives access to Asia’s retail base, with 3.4 million daily active addresses. On BNB, users are rotating in and out of tokenised stocks at high frequency, using 1inch to optimise execution on swaps.

Diversifying across chains has helped Ondo tap into distinct capital pools with varying investor profiles. Ondo’s partnerships help capture these two diverse user populations.

For Ethereum holders, recent integrations have made Ondo stocks a more productive asset class. The team partnered with Chainlink to activate dedicated price feeds for SPYon, QQQon, and TSLAon.

This matters because lending protocols need a reliable, real-time source of truth for any asset they accept as collateral. Without a trusted price feed, a protocol can’t calculate how much a borrower can safely take out against their deposit, or when to liquidate a position that’s gone underwater.

The integration has opened the door for Morpho and Euler partnerships, two of Ethereum’s prominent lending markets, to accept Ondo tokens as collateral. In practice, this means a holder can deposit their SPYon into a Morpho vault, borrow USDC against it, and deploy that USDC elsewhere, all without selling their equity exposure.

It’s the on-chain equivalent of a margin loan: you keep your upside on the stock while unlocking liquidity from it.

For the BNB and Solana retail traders, the partnerships are distribution-oriented. 1inch upgraded its swap API specifically to enable jurisdiction-aware access to Ondo tokens. Tokenised securities carry geographic restrictions; Ondo stocks can’t legally be sold to U.S. persons, for instance. Traditionally, enforcing those restrictions on-chain meant gating access at the platform level: whitelisting wallets, requiring KYC before any interaction, or restricting which frontends could display the tokens. That approach works, but it limits distribution to permissioned environments.

Now, by building jurisdiction awareness directly into its swap routing, 1inch can serve Ondo tokens to eligible users across its entire ecosystem, while filtering out restricted jurisdictions at the infrastructure layer.

Through this 1inch upgrade, Ondo gets the reach of a permissionless DEX aggregator without sacrificing the geographic restrictions that keep the product legally viable.

Additionally, Ondo has also tapped into CEXs and wallets to reach retail traders. MetaMask (30 million MAUs), Trust Wallet (200 million+ users), OKX Wallet, Bitget Wallet, and Ledger were all integrated at or near launch. And recently, Binance Alpha was added, giving Ondo’s token access to the world’s largest exchange ecosystem.

Looking Ahead

Ondo has been building defensibility for its stack through its atomic mint/burns and a broader DeFi integration, however the tokenised equities space is relatively new. The direct tokenisation models are yet to evolve. Securitise has only tokenised one stock so far, Exodus, which holds $95 million in TVL today - higher than any other tokenised stock.

It’ll be interesting to see how the competition between direct and indirect tokenisation will play out in the future. I predict that institutions will prefer the direct ownership model, which they can’t find anywhere else, and non-U.S. retail will keep buying indirect ownership stocks until regulations push them in a different direction.

Nonetheless, there is over $67.999 trillion in stocks left to be tokenised, and how that unfolds is something I look forward to witnessing.

Until then, be curious.

Nishil

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.