Hello,

Last week, Hyperliquid’s HIP-3 markets launched a perpetual futures (or perp) contract on SpaceX. It opened at $150 per share and pegged the company’s implied valuation at $1.78 trillion, less than the $2 trillion valuation that SpaceX has targeted for its IPO. Within hours, traders pushed its price on Hyperliquid to $216. The implied valuation crossed $2.5 trillion. On its second day, the perp price touched $230.

Retail traders on a decentralised exchange had priced Elon Musk’s rocket company over 25% above its own IPO target before a single share had been listed.

Two days later, Polymarket launched prediction markets on private company milestones in partnership with Nasdaq Private Market. Now, you can bet on various events, such as IPO timing and valuation thresholds, for companies that are not yet publicly listed.

Individually, these perp markets and event contracts around private companies do little. Combined, they let the market provide SpaceX with a continuous valuation and an IPO probability. But how reliable is this price before a single share of the company has been issued to the public?

In today’s deep dive, I will explain how crypto has built a parallel pricing infrastructure for private companies and what that means for these firms.

Onto the story,

Prathik

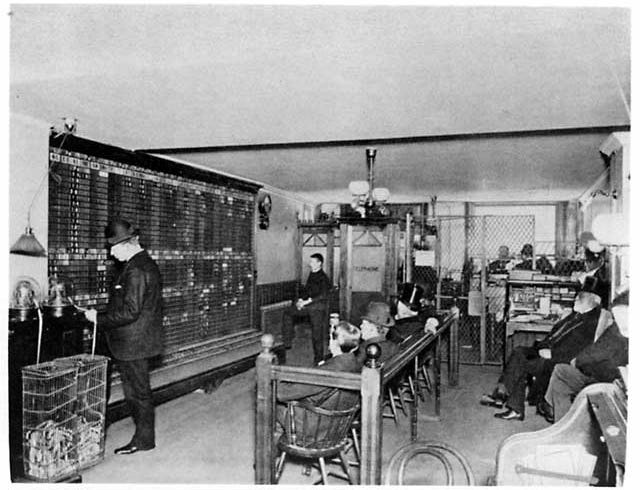

In the 1880s, establishments called “bucket shops” appeared across American cities. From the outside, they passed for bootstrapped brokerage offices. They too had ticker tapes that showed live stock prices and counters where customers placed orders. Except they weren’t legal.

Nasdaq still defines these “bucket shops” as illegal brokerage firms that accept customer orders but do not execute them immediately.

Bucket shops let working-class Americans wager on stock price movements with tiny margins, sometimes as little as a dollar. The operator took the other side of every bet. If a customer wagered that US Steel would rise, the operator paid out when it did. If it fell, the operator kept the margin. No shares changed hands, and no ownership was transferred.

The establishment despised them. The regulators argued that these shops degraded public trust, and the states outlawed them one by one. In 1921, New York’s Martin Act effectively finished them off.

The very shops they had killed, the same ones the regulators had tagged as “gambling dens”, had created an appetite for real shares. America’s stock ownership surged between 1900 and 1922 because of the retail interest these shops had cultivated.

Despite their illegality, bucket shops became highly popular because they separated ownership from pricing. A century later, crypto has developed a similar mechanism for pricing some of the most valuable private companies. However, it contrasts with bucket shops in terms of legality and transparency. A bucket shop was a black box. The operator set the price, took the other side of every trade, and settled in cash with no audit trail. If the operator went bust, so did your money.

On-chain perps are structurally different. Every trade on Hyperliquid is recorded on-chain. Funding rates are public. Settlement is automatic and verifiable. Open interest, liquidation thresholds, and counterparty exposure can be traced in real time by anyone. The pricing layer that crypto has built strips out ownership in the same way bucket shops did, but it replaces opacity with transparency.

A Price for Everything

Polymarket’s partnership with Nasdaq Private Market (NPM) enables it to issue contracts covering IPOs, timing, valuation thresholds, and secondary market activity for companies like OpenAI, SpaceX, Kraken, and others.

The pricing these contracts enable will be nothing like what bucket shops of the 19th century enabled. That’s because this time, traditional players have partnered with the crypto infrastructure. NPM’s resolution data for these event contracts will be pulled from actual corporate-sponsored tender offers and structured secondary auctions.

In an event contract that bets on OpenAI surpassing a $1 trillion valuation at IPO, the resolution will be anchored to cleared institutional trades. This is the first time a regulated secondary market data provider has licensed proprietary pricing data to a crypto prediction protocol.

But these event contracts will just scratch the surface. They form just one layer in what has become a full, parallel pricing stack around private companies. Each tool in this stack can price a different dimension of the same company.

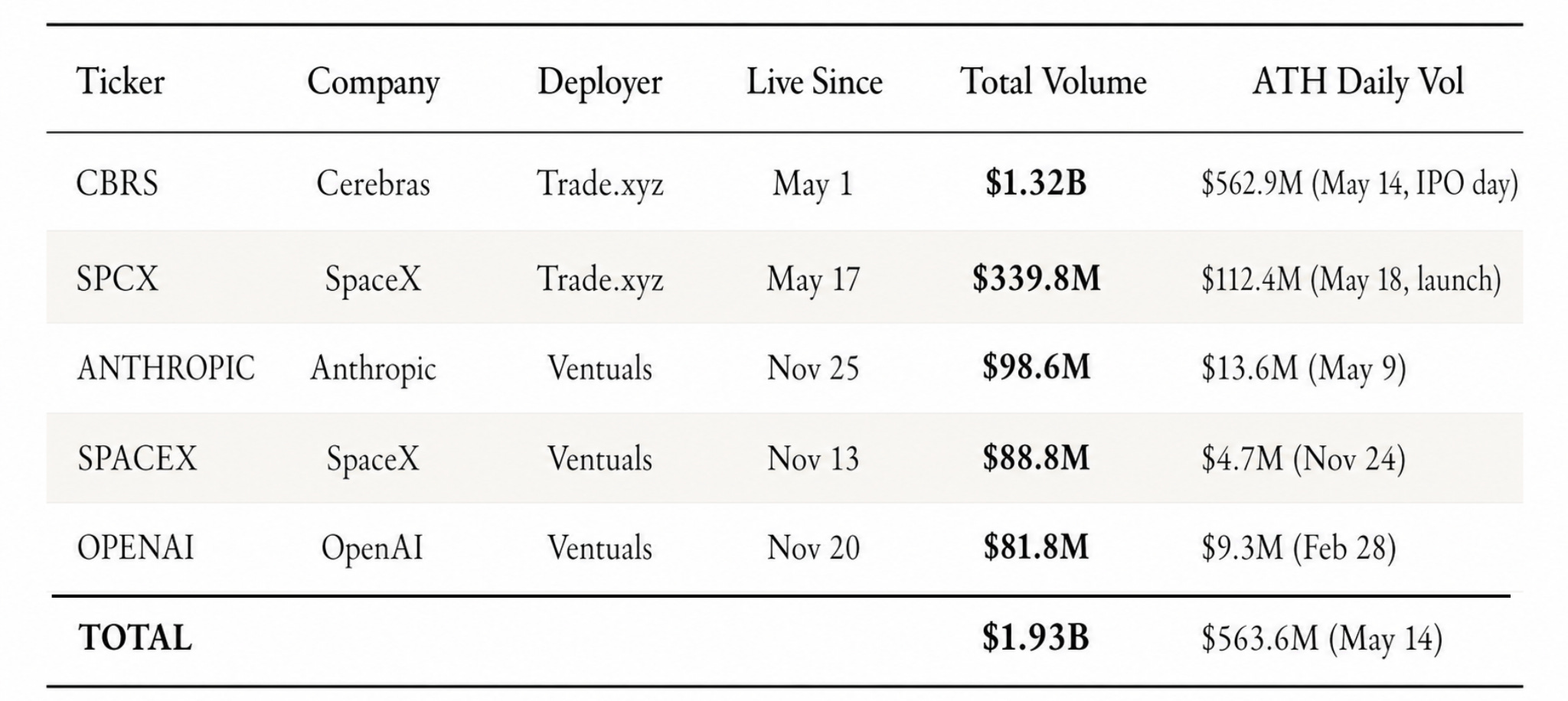

While event contracts can price the probability and timing of the IPO, pre-IPO perpetual futures can continuously price changes in valuation sentiment in the run-up to the debut listing. On Hyperliquid, market makers like Trade.xyz and Ventuals run perps that track SpaceX, Anthropic and other private companies. These trade 24/7 and produce a rolling mark-to-market on companies whose official valuations otherwise update once a quarter or through sporadic funding rounds.

On Hyperliquid, the cumulative volume traded across just five tickers tracking Anthropic, SpaceX, OpenAI and Cerebras touched $1.9 billion in the last six months. Out of this, more than $1.6 billion was traded in May 2026 alone.

There’s a third layer that goes beyond the synthetic pricing of private companies.

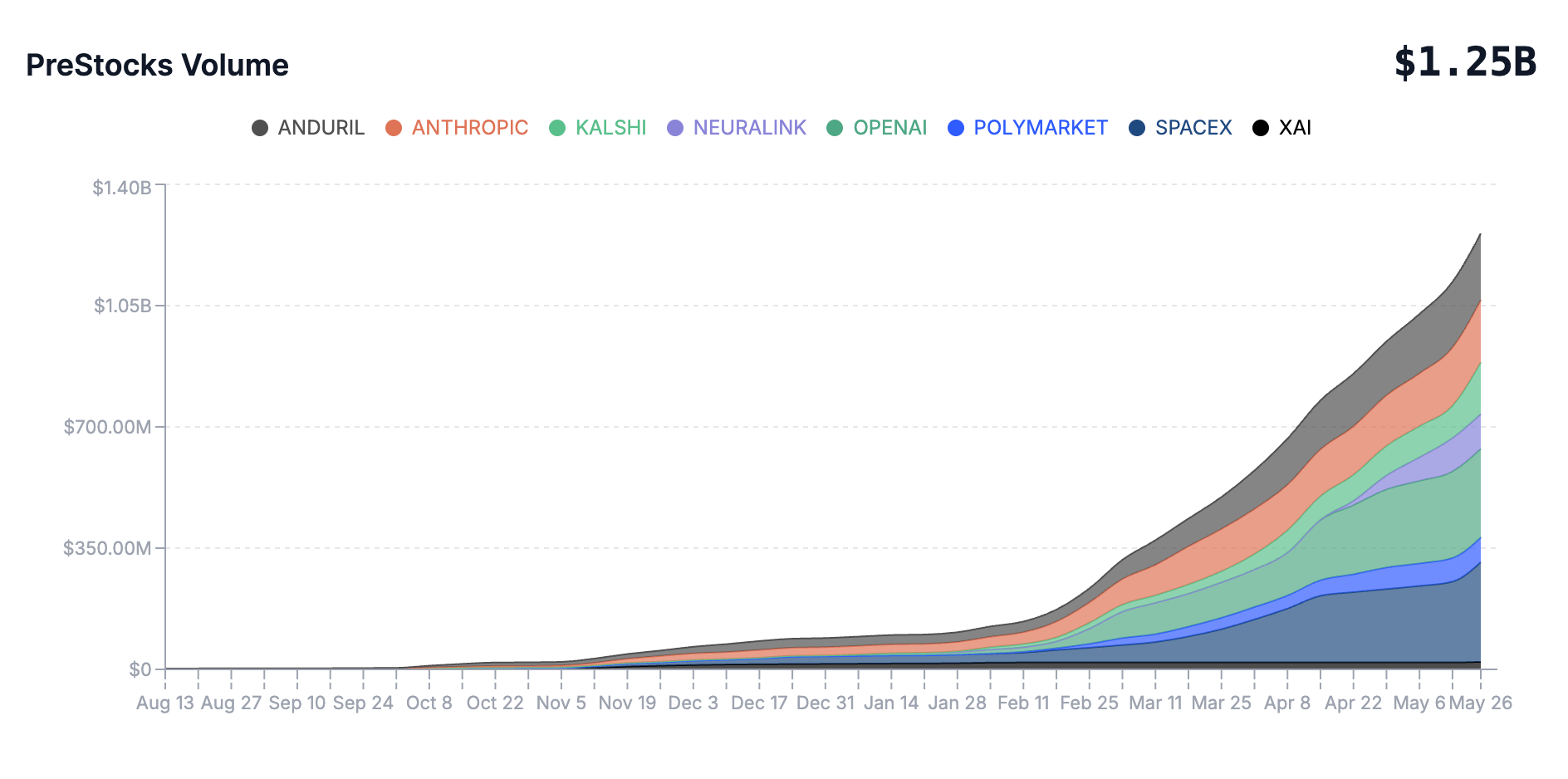

PreStocks, a Solana-based platform backed by Republic Capital, tokenises pre-IPO shares through special purpose vehicles (SPVs) that in turn hold actual equity in companies like SpaceX, OpenAI and Anthropic. Phantom, one of Solana’s largest wallets, has integrated PreStocks directly into its interface, making these tokens accessible to millions of users.

Unlike perps and prediction markets, these tokens aim to provide economic exposure to real shares, not just a price bet.

The demand for PreStocks has been substantial.

The Anthropic token on PreStocks climbed 733% between October 2025 and late April 2026, pushing its implied valuation past $1 trillion. It made Anthropic the third private company to cross that threshold on-chain, alongside OpenAI and SpaceX.

At the same time, Forge Global, a major regulated secondary marketplace, was independently pricing Anthropic near the $1 trillion mark. What’s interesting is that a Solana-based token and a regulated share marketplace were converging on the same number for a stock that has no public listing yet.

PreStocks has processed over $1.25 billion in cumulative trading volume across 3.67 million transactions so far. Of that total trading volume, 93% occurred in 2026.

Today, over 20,000 holders have exposure to pre-IPO stocks such as Anduril, Neuralink, Kalshi, and Polymarket, with a combined value exceeding $25 million.

But how reliable are these? Data shows they do carry signals.

When Trade.xyz launched its HIP-3 pre-IPO perp on Cerebras Systems earlier this month, the on-chain contract traded near $340 about an hour before the Nasdaq opening. The stock on Nasdaq opened at roughly $350. The IPO price was set at $185. The price on Hyperliquid was just about 3% off the eventual opening price. Traditional secondary market platforms were off by around 35%.

Together, event contracts, perps, and SPV-backed tokens start generating a composite, multidimensional, and market-generated price for private companies. This has historically existed only for public companies.

But there’s a cost of holding these instruments.

Perpetual futures contracts carry funding rates, a continuous cost that long holders pay to short holders, or vice versa, depending on market imbalance. For a pre-IPO perp where the majority of participants are bullish, this funding cost can compound over weeks of waiting for an IPO that hasn’t been scheduled.

SPV-backed tokens charge platform fees and carry counterparty risk tied to the underlying vehicle. Prediction market contracts lock capital until resolution. Each instrument attracts a different kind of participant. Short-term speculators are willing to absorb funding rates for quick directional bets. Those with long-term conviction lean towards prediction markets that carry a lower cost. Eventually, the composite price derived from multiple such instruments can reflect this diversity.

Ownership Not Included

There’s a catch. The entire pricing layer is detached from the ownership layer.

Nobody trading a Polymarket contract on OpenAI’s IPO timing gets a claim on OpenAI’s earnings. Those going long on a SpaceX pre-IPO perp on Hyperliquid don’t get voting rights.

Then why do we need these pricing tools for companies not yet publicly traded?

What event contracts, perp markets and SPV-backed tokens have collectively built is closer to what credit default swaps (CDS) did in the 2000s. A CDS lets you express a view on a company’s creditworthiness without lending it a dollar. It created a parallel pricing layer around credit risk that was often more liquid and responsive than the underlying bond market.

PreStocks attempted to go a step further. Its SPV-backed tokens claimed to give holders proxy ownership through indirect economic exposure to real shares. But Anthropic has hit back at that claim. Anthropic said that any share transfer to an SPV without board approval would not be recognised on their books. As a result, the Anthropic token fell from ~$1,400 to $812 in a single day.

Yet the token recovered. Two weeks after the crash, Anthropic’s PreStocks token was trading close to $1,050. The demand for Anthropic’s pricing took a hit when its legal backing was called into question, but the market absorbed the shock and repriced the risk.

This tells us how a PreStocks trader differs from a perp trader.

A trader who bought Anthropic exposure through PreStocks in October at $122 was sitting on an 8x paper return by late May, even after the offering’s legality was called into question. But SPV-backed trades continue to face thin on-chain liquidity and a risk of future legal notices from the private companies.

A trader who expressed the same bullish view through Hyperliquid’s Anthropic perp could enter and exit at any time, against far deeper liquidity, with every position verifiable on-chain and no counterparty risk tied to a company’s transfer restrictions. But the perp trader has to forgo the 8x return.

It shows that the private markets have acknowledged the role of these instruments. They help fill the gap between having an opinion and having no way to express it, and not necessarily give them absolute ownership of the equity.

The Case for Pricing the Private

Polymarket said nearly 1,600 unicorns globally represent a combined valuation exceeding $5 trillion. Companies like OpenAI and Anthropic have brand recognition, revenue at scale, and hundreds of millions of users. They have everything a public company has except public shareholders. Yet, the communications and marketing around these products and companies have ensured that everyone has an opinion about even private companies like SpaceX or OpenAI. In fact, there was never a wider gap between everyone having an opinion on SpaceX, and yet almost nobody being able to price it.

It’s this gap that crypto fills with the entire pricing stack for private companies. They still can’t price using direct equity exposure. Instead, they use indirect SPV-backed holdings, probability, sentiment, timing and continuous valuation as tools to do that.

The story of pricing private companies is about more than just prediction markets or pre-IPO perps. It shows us what happens to an asset class once a full pricing layer is built around it, even before the traditional market structures have caught up.

We have seen this happen before. Last year, Hyperliquid listed a silver perpetual contract. Within a month, it was handling 2% of the world’s silver trading. Not 2% of crypto silver volume, but 2% of the entire global silver market was routed through a blockchain protocol with no headquarters, CEO, or brokers. Silver has been traded on COMEX for decades, fed by a mature institutional infrastructure with deep liquidity. But that infrastructure also came with brokers, high-margin requirements, exchange hours, and minimum account sizes. Hyperliquid let traders price the same old shiny metal by stripping out all the friction points.

Read: A Sliver of TradFi

Robinhood is also building something similar. Its app now lets users hold equities, options, crypto, and prediction markets in a single interface. When a user sees a Kalshi election contract embedded next to their NVDA position, the pricing of each instrument provides richer context for the collective whole. The value is not in any single product.

Read: Why Robinhood Will Eat Kalshi’s Lunch

This infrastructure isn’t being built in isolation. We have seen what tokenisation can do to existing assets. Kraken’s xStocks has tokenised over 100 public equities, generating $25 billion in trading volume with 80,000 on-chain holders. Each token is backed 1:1 by the underlying share held in regulated custody. The xStocks precedent shows us what is possible with tokenisation at scale for public companies. If the same mechanism can be replicated for private companies along with securing issuer-consented pre-IPO tokenisation, it could further boost the adoption of these pricing tools.

The more instruments you can use to price a related outcome, the more accurate a price the market produces about what the world collectively knows (or believes).

This is what should matter the most about the private company pricing stack. A prediction contract, a pre-IPO perp, an SPV-backed token and a secondary transaction each price a different dimension. But collectively, they approximate what public markets do for listed companies.

The accredited investor regime that drives valuations in public markets was built on the assumption that private companies are too complex and risky for ordinary people to evaluate. That assumption is no longer sound when the same ordinary people have been tracking, following, engaging with and pricing SpaceX through social media, X posts, and a handful of different instruments for years before the S-1 lands.

The bucket shops were shut down because the establishment saw only the gambling. They overlooked the demand signal evident in how people priced things they couldn’t own. That demand went nowhere, even after the shops were shut. It has moved from the shops to brokerage accounts, futures markets, and eventually the blockchain.

Today, $5 trillion in value is behind accredited investor gates and priced only occasionally by insiders and venture capitalists. This is reason enough to validate the need for a robust parallel pricing stack for pricing private companies whose affairs and reputations are all but private. PreStocks tried to bundle pricing with ownership. Hyperliquid and Polymarket couldn’t offer ownership but enabled high-leverage, permissionless routes for pricing information.

These tools could change how some of the most important upcoming IPOs are priced by the market long before the first share is listed. They could significantly bridge the gap between price variation in companies’ S-1 filings and the eventual listing price by pricing the sentiment and information developments that occur between the two events.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.