Rainbow and the Window

The moment consumer crypto has been waiting for is here. So are they.

Rainbow spent its first five years as the wallet people recommended to their friends.

Not because it was the most powerful option in space. Not because it had the deepest DeFi integrations or the most chains, or the best swap rates. It was because it was the least scary. You could hand your phone to someone who’d never touched crypto, and they could figure it out. That was the product: a beautiful, approachable, non-custodial Ethereum wallet that didn’t make you feel stupid for not knowing what a sequencer was.

However, this reputation can also be a trap. There’s a version of Rainbow’s future where they spend the next decade being the nicest option in a category that never breaks out of the early adopter bubble. The prettiest wallet in a room nobody else walks into.

Sometime in the last eighteen months, without much fanfare, it stopped trying to be that. The new framing, from the CEO down, is not “best crypto wallet.” It’s not even the “best wallet.” It’s something closer to: the first serious attempt to make crypto earn its users rather than just explain itself to them. It’s a finance app that happens to run on crypto, for people who will never need to know that. Perps. Prediction markets. An on-ramp that doesn’t bleed 7% before you’ve done anything. A savings layer. Tokenised stocks, eventually. Every asset class in one place. But also the things that have never been available to normal people at all such as borrowing against your assets instead of selling them, the move wealthy investors make to avoid a tax event, now available to anyone with a DeFi position. That’s not rebuilding what Robinhood has. That’s building what Robinhood can’t.

This shift might seem like a marketing pivot, but it’s not. It’s a product conviction about where consumer finance is actually going. And the reason it’s worth paying attention to is that Rainbow might be right.

The problem they’re solving isn’t the one you might think. Here is what happens when someone new downloads a crypto wallet in 2026: They get redirected to a third-party service they’ve never heard of to fund the wallet. They create an account there that doesn’t carry over anywhere else in the app, deposit $100, and receive $93. They try to use the remaining balance but hit an error about gas on the wrong chain. They close the app and don’t come back.

This is the state of crypto onboarding across almost every wallet that isn’t Coinbase.

Nubank has 113 million customers. Venmo has 66 million monthly active users. The largest crypto wallets are in the hundreds of thousands. The gap is not a marketing problem. It’s a product problem, specifically the problem of what crypto onboarding actually feels like to a normal person in 2026. The protocol layer has matured considerably over the last four years. Gas is cheap, settlement is fast, and the infrastructure works. But the product layer has not caught up. The people building these products largely don’t feel the friction because they’ve had MetaMask installed for years and have forgotten what it was like not to know what gas is. The feedback loop is broken. Builders test on themselves, fund on themselves, and then express genuine confusion when adoption doesn’t follow.

Alex LaPrade Kikis, who joined as Rainbow’s CEO about eighteen months ago, describes their goal as making crypto fade into the background. Build the finance product first. Make the blockchain the part nobody thinks about. The first thing he named when I asked about competition was not Phantom, not MetaMask, not Coinbase Wallet. It was Robinhood. That answer tells you almost everything about what Rainbow is actually building.

The on-chain version of everything

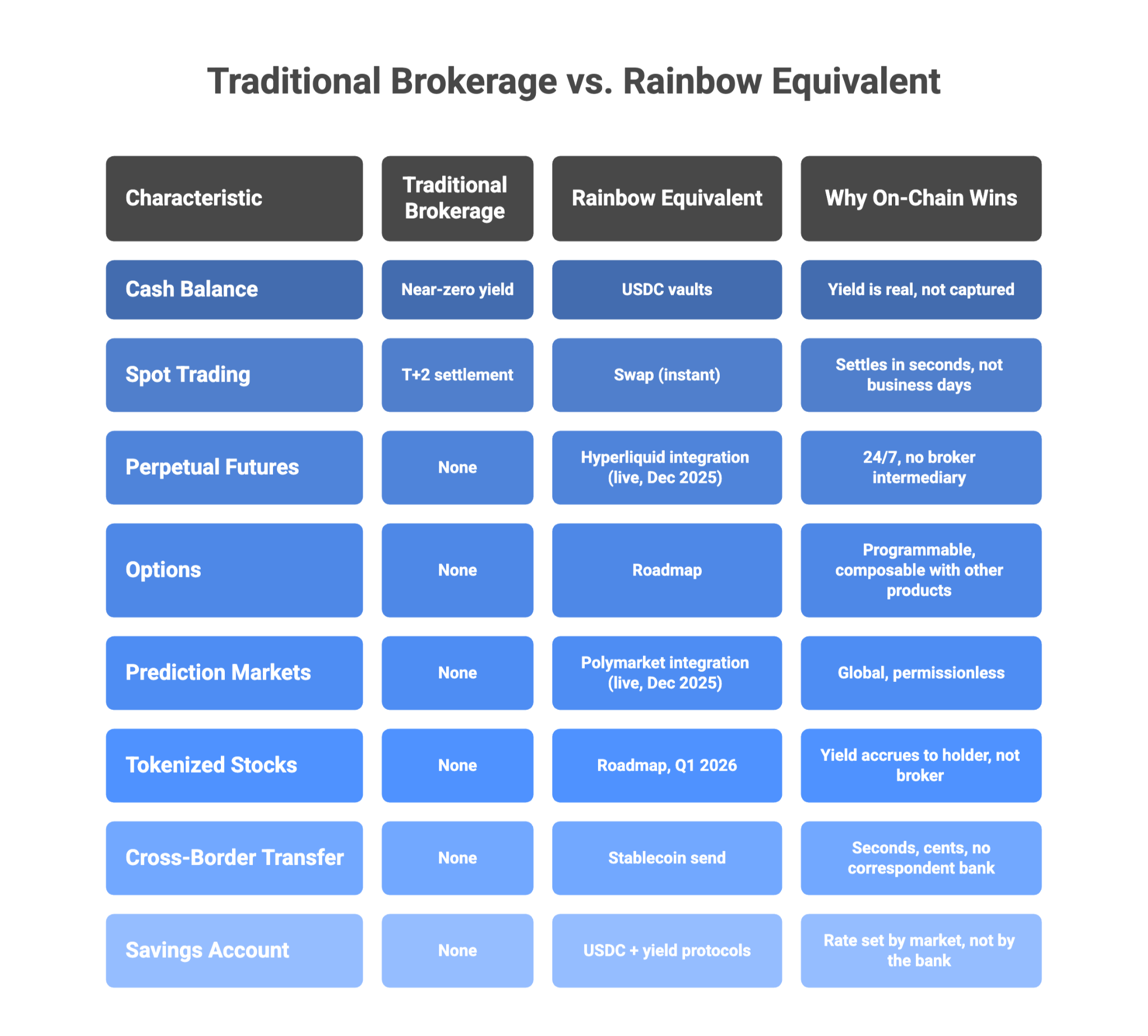

The specific thesis is that for every revenue line that exists in a traditional brokerage today, there is an on-chain equivalent that is structurally superior once you strip out the friction. Cash balance that earns real yield instead of near-zero. Spot trading without the 2-3 day settlement lag. Perpetuals and options. Tokenised stocks where the yield accrues to the holder instead of disappearing into the broker’s margin. This is a strong claim. It’s also probably right, in the long run. The question that haunts every team making this argument is timing. What happens in the years between now and then, while Robinhood is figuring out what a sequencer is, and JPMorgan is running blockchain pilots that won’t ship for three years.

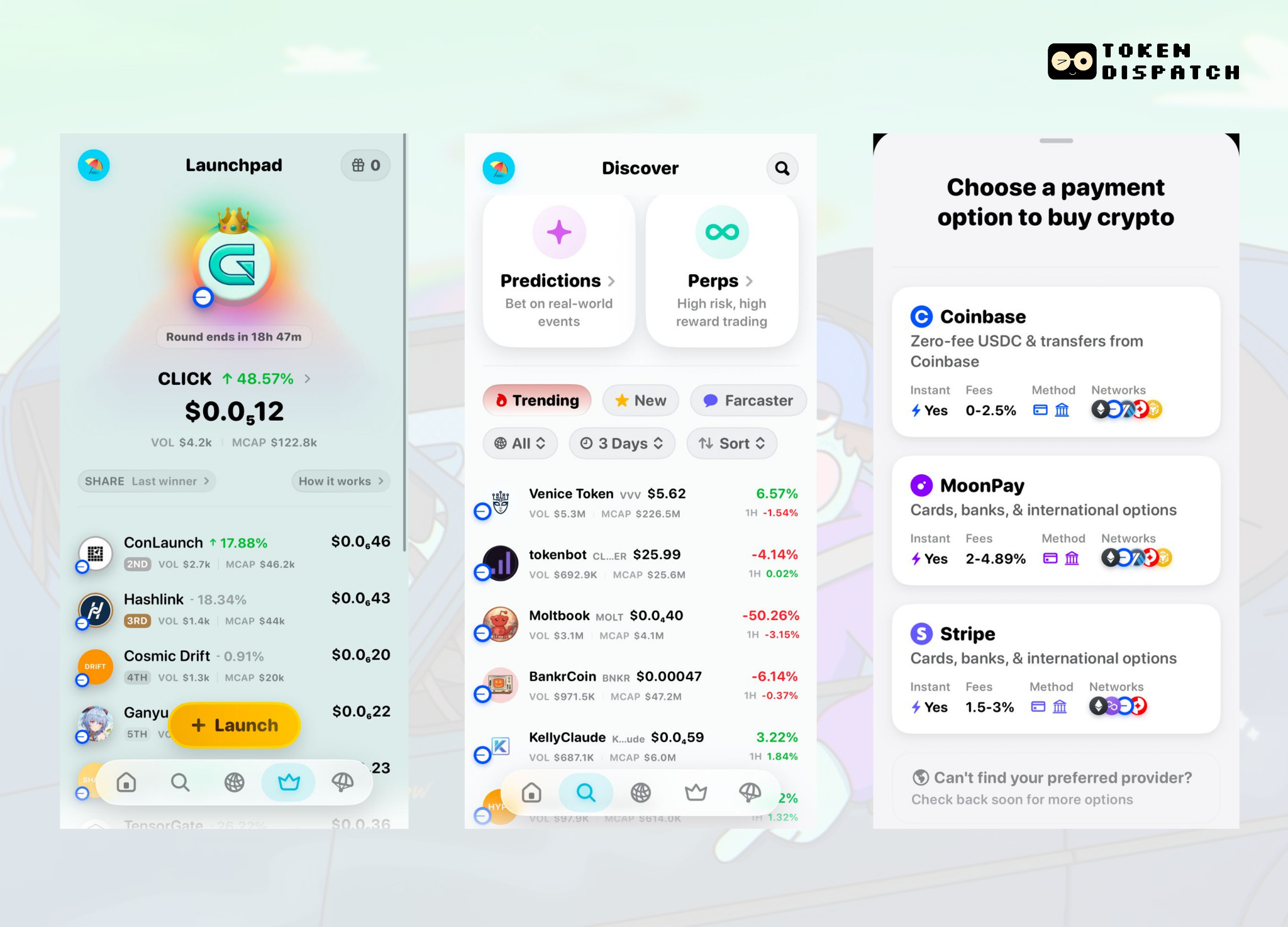

What Rainbow has shipped toward that vision is perpetual futures via Hyperliquid, added in December. Prediction markets via Polymarket, also December. Candlestick charts and real-time portfolio pricing built in, which matters if you’re trying to eliminate the need for a separate market app. An on-ramp being rebuilt on direct rails, aimed at Cash App parity, meaning no redirect, fee leak, or wrong-chain error on arrival. Solana support is coming this year, a meaningful concession from a team that has been Ethereum-native since the beginning.

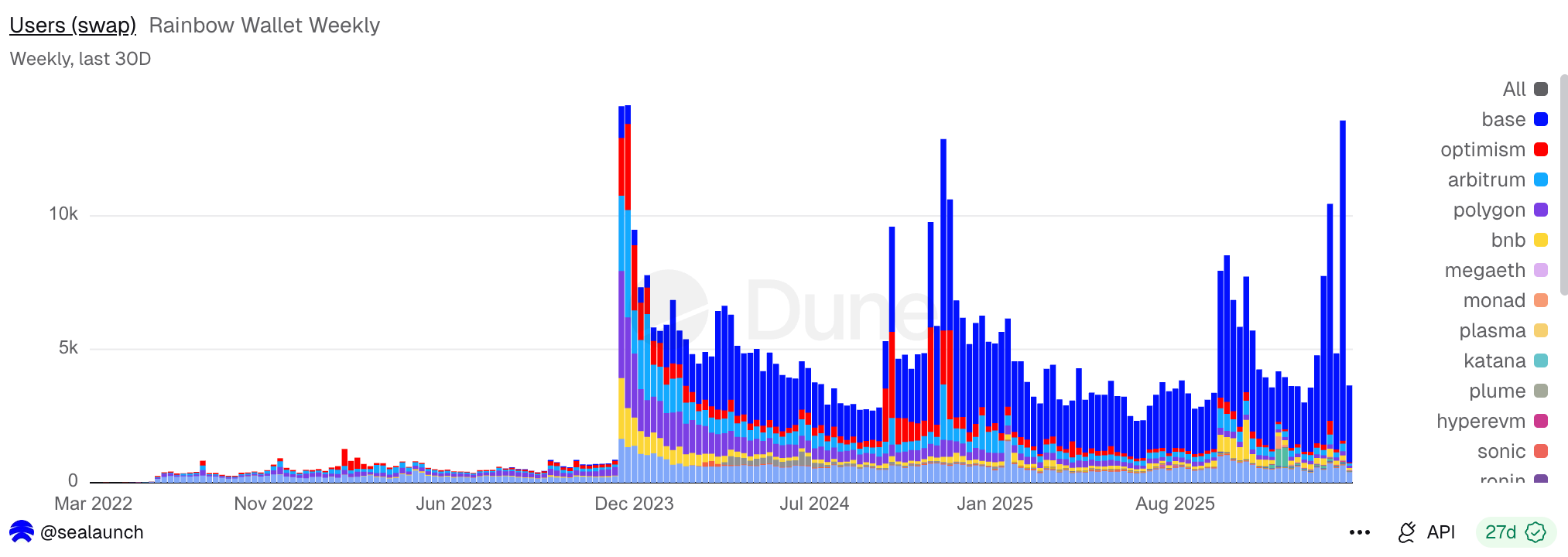

The numbers are honest about where Rainbow stands. On-chain data shows , Rainbow users processed about $101 million in on-chain swap volume in a recent month. $14 million of that happened inside Rainbow itself. The remaining $87 million went directly to dApps, because users with existing habits go to the interfaces they already know. The 20% share-of-wallet figure is something the team tracks and talks about without varnish. It tells you whether users trust the app enough to do their financial life inside it, whether they’ll stay, and whether the on-chain Robinhood thesis is actually working or just a slide deck.

The user breakdown matters here, because it changes what problem Rainbow is actually solving. There are three distinct groups using Rainbow, and the most important one is not the most obvious.

First, the OGs. Crypto-native users who adopted Rainbow early and stayed. They use centralised exchanges to on-ramp because they know how, and use Rainbow for everything after. Second, the Robinhood migrants: millennials moving away from traditional brokerages who found their way into crypto through fintech and landed on Rainbow because it was the least hostile option available. Third, and this is the one that changes the calculus. Only 20% of Rainbow’s users are in the US. The rest is a global base spread across dozens of countries, with Latin America and Southeast Asia growing the fastest.

Their usage is stickier than the other two segments. The transaction sizes are small. And the behaviour is exactly what the original crypto thesis was supposed to produce: just better money.

Last week, I wrote about Meta bringing stablecoins into WhatsApp. The argument was that Meta isn't trying to create a new currency. It's building the interface layer for dollars that already exist. Hundreds of millions of people across emerging markets are going to receive stablecoins for the first time through a platform they're already on. Those people will need somewhere to put those dollars to work. A savings product. A way to accumulate BTC over time. Something that doesn't assume they understand what a seed phrase is or care about L2 decentralization. Rainbow's long game is that they are the destination for that moment. Because by the time that moment arrives, they will have built the product layer that makes sense for it. The discipline to not push the most revenue-generating products at new users, to guide them toward USDC vaults and BTC accumulation instead of meme coins, is what Alex describes as underwriting a 20-to-30-year user relationship. The math behind that bet is an Oxford Economics study commissioned by Wealthfront estimates the wealth of digital natives growing at 11.3% annually, from $12 trillion in 2022 to $140 trillion by 2045. The user who gets a good first experience today is worth an enormous amount more in twenty years.That is a non-crypto way to think about a crypto product. It's also how every fintech that won thought about it.

Read: The Second Attempt - by Thejaswini M A

The race

Robinhood has a non-custodial wallet. It is not good. They announced an Ethereum L2 on Arbitrum last June and had a testnet eight months later. They will get there eventually, because they have 24 million funded accounts and the capital to solve product problems with money. But crypto is not in their institutional DNA, and the track record reflects that. Meanwhile, institutions that were the loudest skeptics of crypto two cycles ago are now moving real parts of their businesses on-chain. That shift is happening, regardless of what crypto-native teams do.

What crypto-native teams have that those companies are still trying to acquire is something you can’t buy. They understand how these products actually work at the user level. They know what a seed phrase recovery flow needs to feel like. They know what MEV protection means at the swap layer. They know the exact sequence of UI failures that cause a new user to close the app and not come back. That head start is there but not permanent. The window for crypto-native teams to own the consumer finance layer is measured in years, not decades. You can see Rainbow treating it that way. The pace of product shipping in the last six months, perps, prediction markets, the on-ramp rebuild, suggests a team that has done the math on how long they have.

What the token doesn’t change

Rainbow’s token (RNBW), which launched in February, dropped roughly 84% from its all-time high within weeks. This pattern is familiar enough in this space that it barely requires comment, except to note the team's stated position on what follows. They are not doing buybacks. Even with the token trading well below where the team thinks it should be, they still believe reinvesting in the product returns more. That is either a very high bar for product conviction, or a very low bar for the token. Probably both.Rainbow has not exhausted those ideas.

The Rainbow Foundation holds equity in the company. Token holders benefit from reinvestment in the business rather than from yield extraction. Whether that framing holds long-term is worth watching separately. The more relevant point right now is that the token doesn’t change the product thesis. The thesis predates it. The market’s opportunity predates it. The onboarding problem predates it. Those are the things that will determine whether Rainbow becomes the app it is trying to become.

Every major consumer finance company was built during a window. Robinhood launched in 2013, when zero-commission trading was still a radical idea, and the incumbents were too comfortable to take it seriously. Cash App launched the same year, when peer-to-peer payments still felt like a problem worth solving. Both companies looked subscale and slightly naive for years before they didn’t. The window they were building for eventually opened, and they were already inside it.

Rainbow is built during a similar window. Stablecoin infrastructure is everything anyone ever needed. The regulatory framework has arrived. The moment where ordinary people start receiving and holding digital dollars at scale is no longer theoretical. It has a product roadmap and a launch calendar across major platforms.

What that moment produces is people who have money in a digital wallet and need somewhere to put it to work, who just want the yield to be real and the transfers to be fast and the app to make sense. That user needs something that doesn’t exist yet at any meaningful scale.

Rainbow is closer to building it than anyone I’ve seen. They understood the assignment before most people in this space were willing to admit what the assignment was. That matters more than it sounds. The companies that win the next decade of consumer finance will not be the ones that built the best crypto tools. They will be the ones that were already in position when the tools stopped mattering and the product became everything.

Rainbow is in position.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.