The Second Attempt

Meta is putting stablecoins into WhatsApp. This time, nobody is stopping them.

In July 2019, Mark Zuckerberg sat before the Senate Banking Committee and tried to explain why Facebook should be allowed to create a global currency. It did not go well. Senators compared Libra to a “9/11-level threat.” Regulators in France and Germany announced they would block it outright. The Federal Reserve chair called it a serious concern. Within three months, PayPal, Visa, Mastercard, eBay, and Stripe had all withdrawn from the Libra Association. By 2022, the project was dead, its assets sold to a small California bank for $182 million.

Seven years later, Meta is putting stablecoins into WhatsApp, Facebook, and Instagram. The rollout is planned for the second half of 2026. Stripe, the same company that withdrew from Libra in 2019, is the frontrunner to power it. And so far, Washington has said almost nothing.

Nothing about what Meta wants has changed. Everything else has.

It helps to be precise about what Libra actually was, because the 2026 version is something different, and the difference matters.

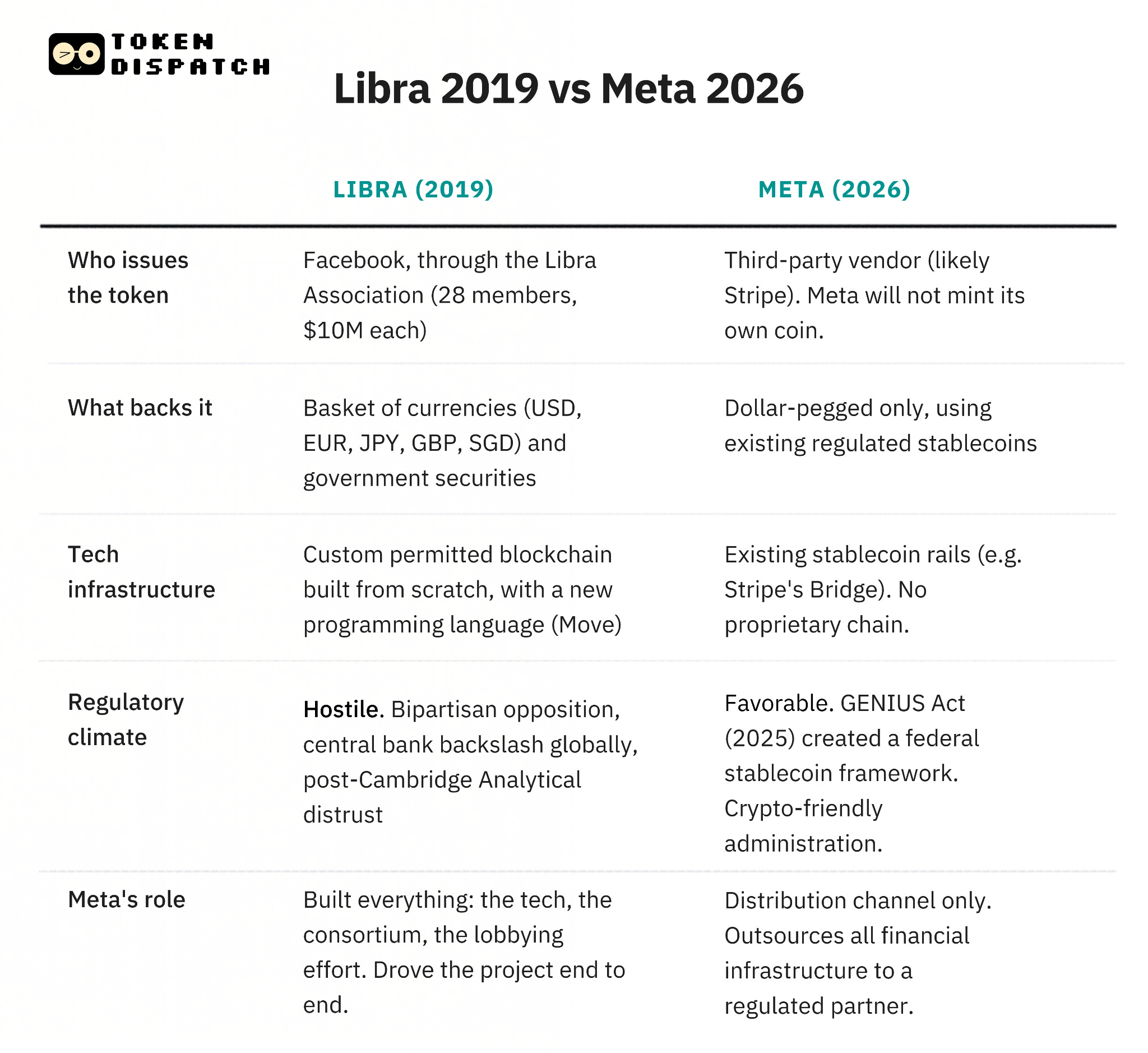

Libra was an attempt to create a new global currency. It would be backed by a basket of sovereign currencies, governed by a private consortium of corporations, and issued on a proprietary blockchain. Facebook wanted to create money. Not a payment method or a settlement layer. Money. A new form of it, controlled by a private association that Facebook was the most powerful member of, was circulating across two billion users before any central bank had figured out what to do about it.

That is what regulators killed. The concern was that an entity the size of Facebook issuing currency to two billion people, outside the existing regulatory apparatus, was a genuinely novel threat to monetary sovereignty. The congressional panic was overheated, but the underlying concern was not wrong.

What Meta is doing in 2026 is closer to the opposite. The company has no plans to issue its own stablecoin. It has issued requests for proposals to third-party providers. The goal, as Meta spokesperson Andy Stone put it, is about “enabling people and businesses to make payments on our platforms using their preferred method.” Meta is not trying to be the issuer but the interface.

The distinction sounds small. It is not. Issuing currency means owning monetary policy, managing reserves, dealing with central banks, and becoming a regulated financial institution in every jurisdiction where your currency circulates. Being the interface means building a wallet and plugging into stablecoins that other regulated entities have already issued, already backed, and already cleared with regulators. The compliance burden moves from Meta to Circle, Paxos, or whoever wins the contract. Meta gets the distribution without the liability.

David Marcus, who led the original Libra team, has said the project spent years revising its design and addressing regulatory concerns, only to be blocked by political pressure rather than a clear legal rejection.

The political pressure, ironically, produced the GENIUS Act, signed in July 2025, which created a federal framework for stablecoin issuers in the US. The law mandated 1:1 reserves in high-quality assets. It legitimised stablecoins as a form of tokenised cash. It gave large companies exactly the regulatory clarity they needed to move. The people who killed Libra, in other words, spent the next five years building the conditions that made the 2026 version possible.

The partner list matters as well.

Stripe acquired Bridge, a stablecoin infrastructure company, in October 2024 for $1.1 billion. Bridge received conditional approval from the OCC for a national trust bank charter in February 2026, allowing it to operate as a regulated entity for stablecoin issuance and custody inside a clear federal framework. Patrick Collison, Stripe’s CEO, joined Meta’s board in April 2025. The institutional ties between the two companies are now significant enough that Stripe being named the infrastructure provider for Meta’s stablecoin integration would not surprise anyone who has been watching this game.

This is what “arm’s length” looks like in practice. Meta handles the user experience across nearly four billion monthly active users. Stripe and Bridge handle custody, compliance, on-ramps and off-ramps, and cross-chain settlement. The blockchain, whichever one ends up being used, remains, as much as I hate this phrase — invisible” to the person on Instagram who receives a creator payout or sends money to someone. It is also what makes the adoption argument interesting.

The industry has been measuring adoption by wallet addresses and exchange signups, and finding it still limited to people who already know what they’re doing. That framing assumes adoption looks like people choosing to use crypto. What Meta is building assumes adoption looks like people using crypto without choosing it, because it’s already inside the app they use every day.

Read: The Consumer App Problem - by Thejaswini M A

The use cases that make sense here are specific and unglamorous. Creator payouts: Meta currently processes payments to creators in dozens of countries through traditional banking, which is slow, expensive, and unavailable to creators in markets with limited financial infrastructure. In December 2025, YouTube enabled US creators to receive earnings in PYUSD, PayPal’s stablecoin. PayPal manages the conversion on the backend. The creator sees a number in their wallet. The structure Meta is building is the same logic at four times the scale, across markets where the case for bypassing traditional banking rails is far stronger than in the US.

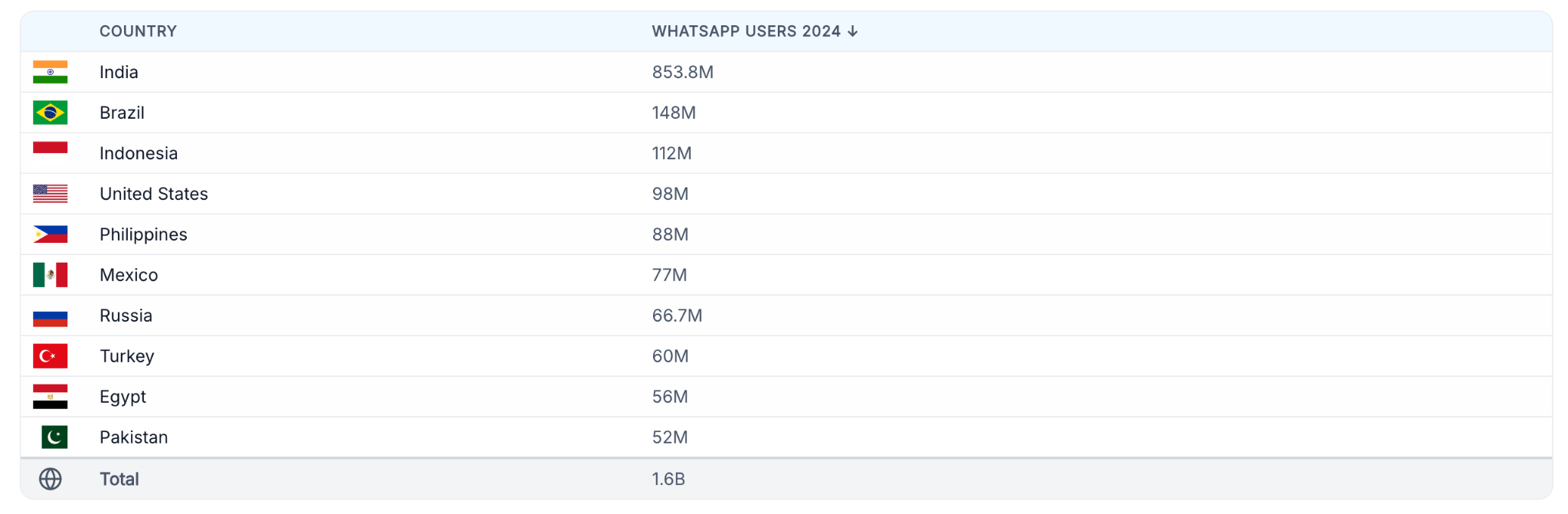

Cross-border remittances: WhatsApp has an 84% daily open rate in many emerging markets. It is the primary communication infrastructure for small businesses across India, Brazil, Nigeria, and Southeast Asia. Embedding dollar-denominated payments into a tool people already open thirty times a day is a different proposition than asking them to download a crypto wallet.

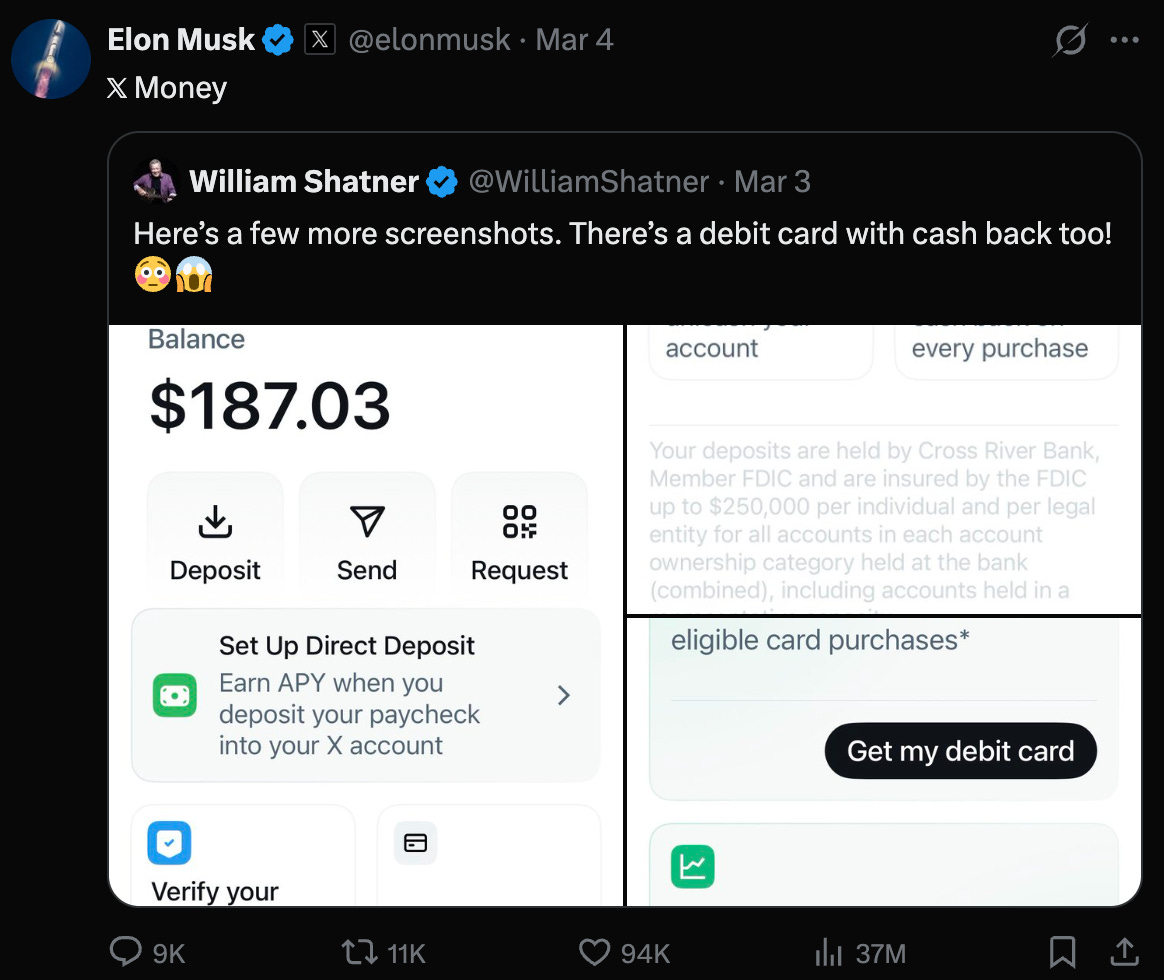

X Money is the comparison that every piece about Meta’s stablecoin integration will make, but be careful about what the comparison actually shows.

Elon Musk has been gesturing toward payments on X since he bought Twitter in 2022. He said X would launch payment services by mid-2024. It didn’t. In February 2026, Musk confirmed during an internal xAI presentation that X Money was running in closed beta among X employees, with a limited external rollout expected within one to two months. The beta features, as revealed through the William Shatner promotion, include peer-to-peer transfers, a 6% APY on deposits via Cross River Bank, FDIC insurance up to $250,000, and an X-branded debit card with cashback. Despite years of speculation about Dogecoin integration, the current beta shows no sign of any cryptocurrency support.

Let’s have a look at the contrast with Meta. X Money, at least in its current form, is building a neobank. High-yield savings, debit cards, direct deposit, FDIC insurance which are the features of a bank account that happens to live inside a social media app. It may work. But it is operating inside the existing financial system, using traditional banking infrastructure via Cross River Bank and Visa’s payment rails. X is solving for the American retail banking market.

Meta is solving for something else. The stablecoin integration is aimed at the markets where traditional banking is either too expensive, too slow, or simply unavailable. WhatsApp’s user base is disproportionately in the developing world. The app leads in 65 of the 100 most populous countries, and in markets like Nigeria, South Africa, and Brazil, over 90% of internet users are on it monthly.

The creator economy that Meta is trying to streamline is global. The cross-border remittance market, worth roughly $800 billion annually, runs on correspondent banking rails that take days and charge significant fees. Stablecoins, settling in seconds for cents, are not a marginal improvement in that context.

Two different theories, in other words. X wants to be a bank for its existing users. Meta wants to be the payment infrastructure for a global internet that its platforms already reach. They are not really competing for the same thing. Meta reported Q4 2025 revenue of $59.89 billion, up 24% year over year. The company has the capital to do this seriously.

With Meta, there’s always a data privacy concern. In January 2026, Instagram suffered a scraping incident that exposed the data of 17.5 million users. Meta’s standard response to scraping incidents is that no systems were breached, only publicly accessible data was collected. It matters less when the data in question starts to include transaction history. Financial data layered on social graph data creates an identity profile that is more complete and more exploitable than either alone. Meta will have to make a credible case on this front for the integration to scale without a political backlash that rhymes with 2019.

There is also the more immediate commercial reality. A platform that can see what you buy, not just what you click, has significantly better targeting data than one that cannot. Meta’s advertising business runs on behavioral inference. Transaction data removes the inference.

The regulatory environment is friendlier than it has ever been. It is not unconditionally friendly. The GENIUS Act prohibits stablecoins from paying yield, which is why Meta’s product is framed as payments rather than savings. That prohibition also creates a meaningful ceiling on how compelling the product can be in developed markets where users have yield-bearing alternatives. The emerging market use case is more durable, but also more complex to execute across dozens of regulatory jurisdictions.

None of which changes the core observation about what is happening.

In 2019, the argument was about whether Facebook should be allowed to touch money at scale. That argument is now settled, and it settled in Meta’s favor, because the regulatory environment decided that stablecoins issued by regulated third parties and distributed by large platforms were a manageable risk. The GENIUS Act is effectively a license for companies like Meta to do exactly what Libra tried to do, through a different structure.

The stablecoin market passed $300 billion in circulating supply last year. Stablecoin transaction volume reached $33 trillion in 2025. Stripe’s stablecoin volume hit $400 billion, growing through market downturns. The distribution problem is the only remaining hard problem, and Meta has 3.98 billion monthly active users.

The “adoption” debate in crypto has always been about getting people to choose to use it. What Meta is building doesn’t require that choice. The choice gets made at the infrastructure level, and the user experiences something that looks like sending money on WhatsApp.

Meta is not the only company doing this, but it is the largest, and it is doing it in the markets where the case for stablecoin payments over traditional banking is strongest.

Whether this is good for “crypto” in the sense that people mean when they say crypto, for decentralisation, for token prices, for the broader DeFi ecosystem, is a different question. What it is good for, unambiguously, is stablecoin volume and the utility of dollar-denominated digital payments as global infrastructure. Libra wanted to create a new form of money. The 2026 version is content to move the money that already exists, better and cheaper than the existing rails.

That is a smaller ambition. It is also a more achievable one. And it has almost four billion potential users.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.