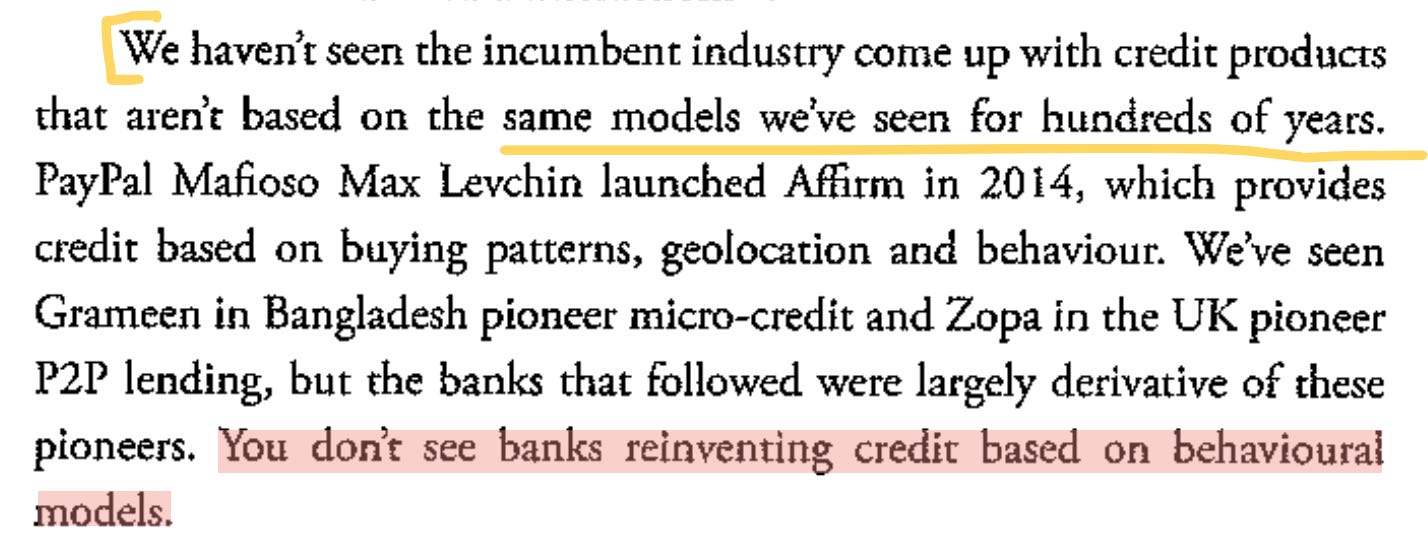

Could you forget the bank you have and create one from scratch? Start from zero, with the tech we’ve got now.

While doing that, would you build physical branches? Paper money? A “wet” signature on a form, witnessed and filed, to prove who you are? Passbooks, plastic cards, cheque books, and a mortgage that needs 17 - 20 pieces of paper.

This is what Brett King asks you in his book, Bank 4.0. Today, I am reviewing his thesis to see what parts of his future showed up.

“No, I’m sorry,” King writes. “That’s just plain crazy talk.”

He’s right, that’s why I kept reading after the 50 pages (that’s my rule of thumb to decide whether to drop or go on with a book). The bank you use is a stack of medieval artefacts, now made with software on top of it. The Medici built the shape of it in Florence. Today’s payment networks are another version of the Knights Templar moving gold for royalty in the 1100s. For those who don’t know, the Knights Templar created the first international banking system to protect wealth. Instead of carrying physical gold through dangerous areas, rulers deposited their assets in Templar fortresses and travelled with coded letters of credit.

An 1850 passbook in plastic is now your “debit card”. Apple Pay is that plastic card copied again inside a phone. And the branch? It hasn’t really changed since Monte dei Paschi opened in Siena 750 years ago and never left.

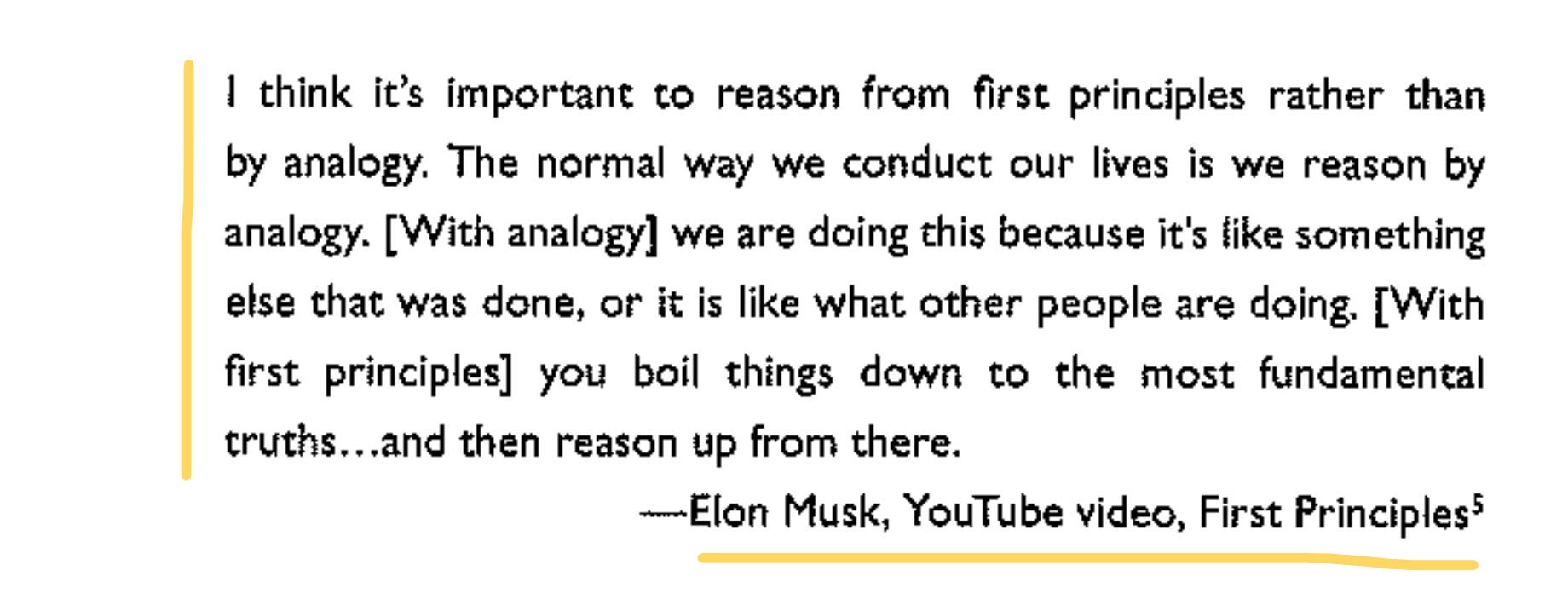

King borrows a word from engineers for how this happens. Design by analogy, which is when you solve a problem by looking at how something completely unrelated works and stealing their idea.

You build the new thing by copying the old thing and improving it a little. Von Braun’s V-2 became NASA’s Apollo became every rocket since. Carl Benz, in 1885, instead of trying to build a faster horse carriage, took an existing engine and built the first car. Musk did the same with SpaceX and dropped the cost to orbit by more than 90 per cent. Jobs carried a block of wood around the office to remind his team that a phone could start from nothing.

When the web showed up, King says, they took the branch and retyped it onto a screen. Online banking is a branch form, but it is in a browser. Mobile banking is the same form, but smaller. Did we ask if the form needed to exist?

A quarter century after the internet went commercial, there are still places you can’t open an account without going there in person and signing your name with a pen. You prove your identity with a first-century artefact that isn’t unique and is easy to forge.

If you build a bank from scratch today, you don’t build a bank at all. You just want your money to move from point A to point B. So, the whole thing is a tool of utility. When you remove the cards and signatures, you can see how they were blocking what you actually wanted to do without that friction; the “bank” would be swallowed up, and only the function would remain.

Most of the book is about the companies King thought would do the stripping. Neobanks and Fintechs. Also, the Chinese giants like Alibaba and Tencent.

The heroes of Bank 4.0 mostly did the analogy thing, too. Revolut, Monzo, N26, and King’s own Moven built a beautiful app and a faster sign-up. But they are still routing your money through the exact same slow, fifty-year-old banking pipes as Everyone Else.

That means a neobank is an app, not a bank in the deep sense. When you tap a Revolut card or send a transfer, the app hands the job to the old systems everyone uses. Visa and Mastercard clear the card tap. A network called ACH handles bank-to-bank transfers in the US, and it settles in batches.

King’s test requires abandoning assumptions and rebuilding infrastructure from zero, but his chosen heroes fail that benchmark. They only make small changes to old systems instead of building a new foundation.

If you do not touch the rail, you are iterating on the branch. Seventy-six per cent of neobanks still lose money. I have written about this last week. The average one earns about $45 a year per user. A normal bank earns $350. The surviving neobanks did it by reaching for the oldest trick banks have. Lending. Nubank makes its money on credit cards and loans. Revolut turned its first real profit once its loan book grew. To sum it up, the neobank that lived became a bank.

Read: Neobanks Have to Be Banks - by Thejaswini M A

King writes, is “what inevitably emerges when you have to retrofit money, value stores and payments systems to a real-time world sitting on the IP layer, directly accessible by the user rather than through a gatekeeper.” Read that again with stablecoins in mind.

I meant to say take the volatility out of his Bitcoin, and you land on the thing his own logic was pointing at. He couldn’t say it in 2018, so he kept the chapter at arm’s length, probably why he called it “a futurist’s perspective,” and moved on.

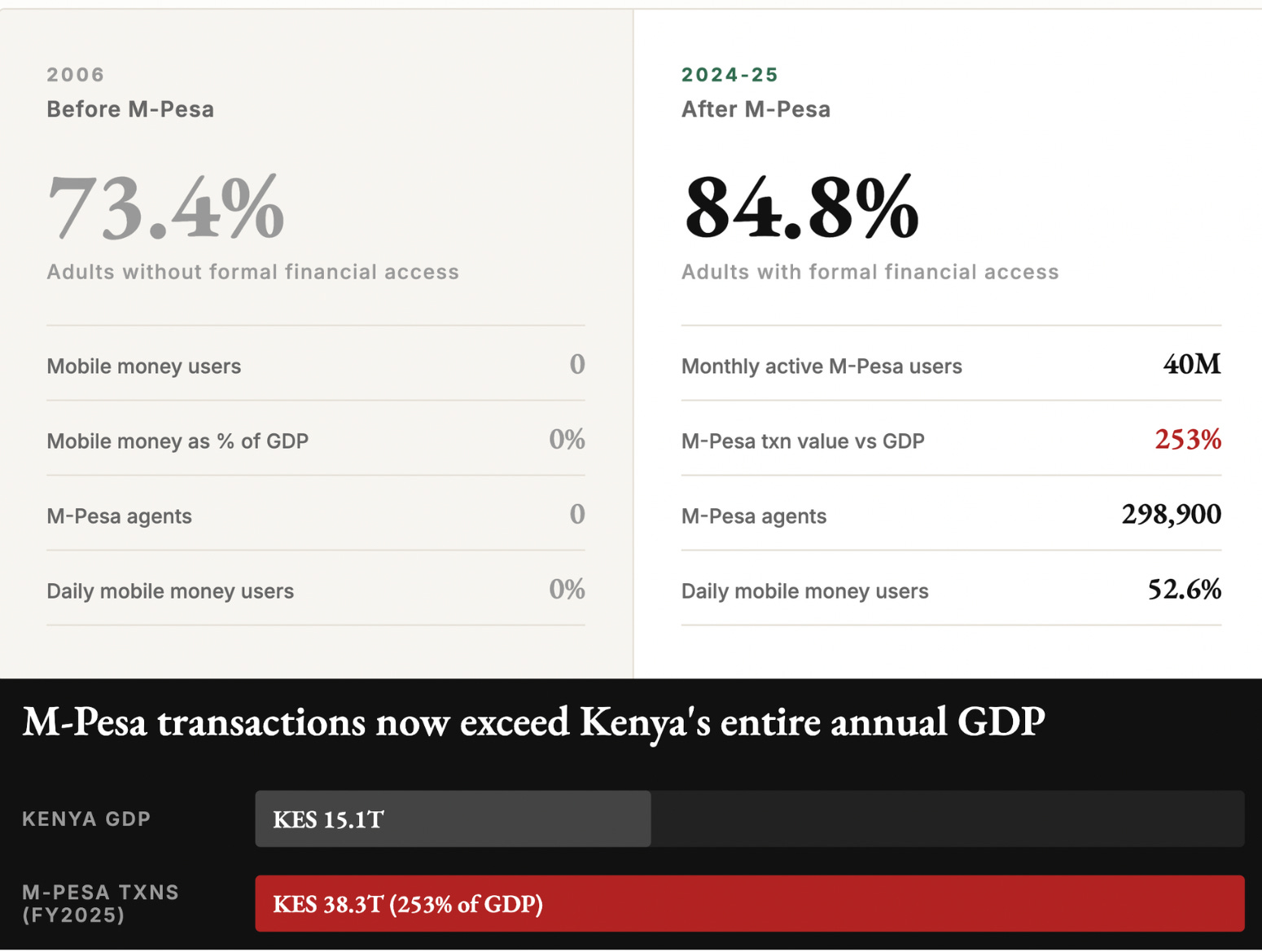

The action is in emerging markets, where legacy is poor. Then he tells the M-Pesa story. In 2005, seven in ten Kenyans had no bank account. Today, nearly every adult uses mobile money, and around 40 per cent of the country’s GDP moves across M-Pesa’s rails(at the time when King wrote this, now it’s more). The banks saw it coming and lobbied the finance ministry to investigate. They were already too late. First principles win first in the places the old system never bothered to serve. Stablecoin adoption is loudest where the local currency is shaky, the banks are slow, and a phone is the only branch anyone has, which is the same shape as M-Pesa, one layer down.

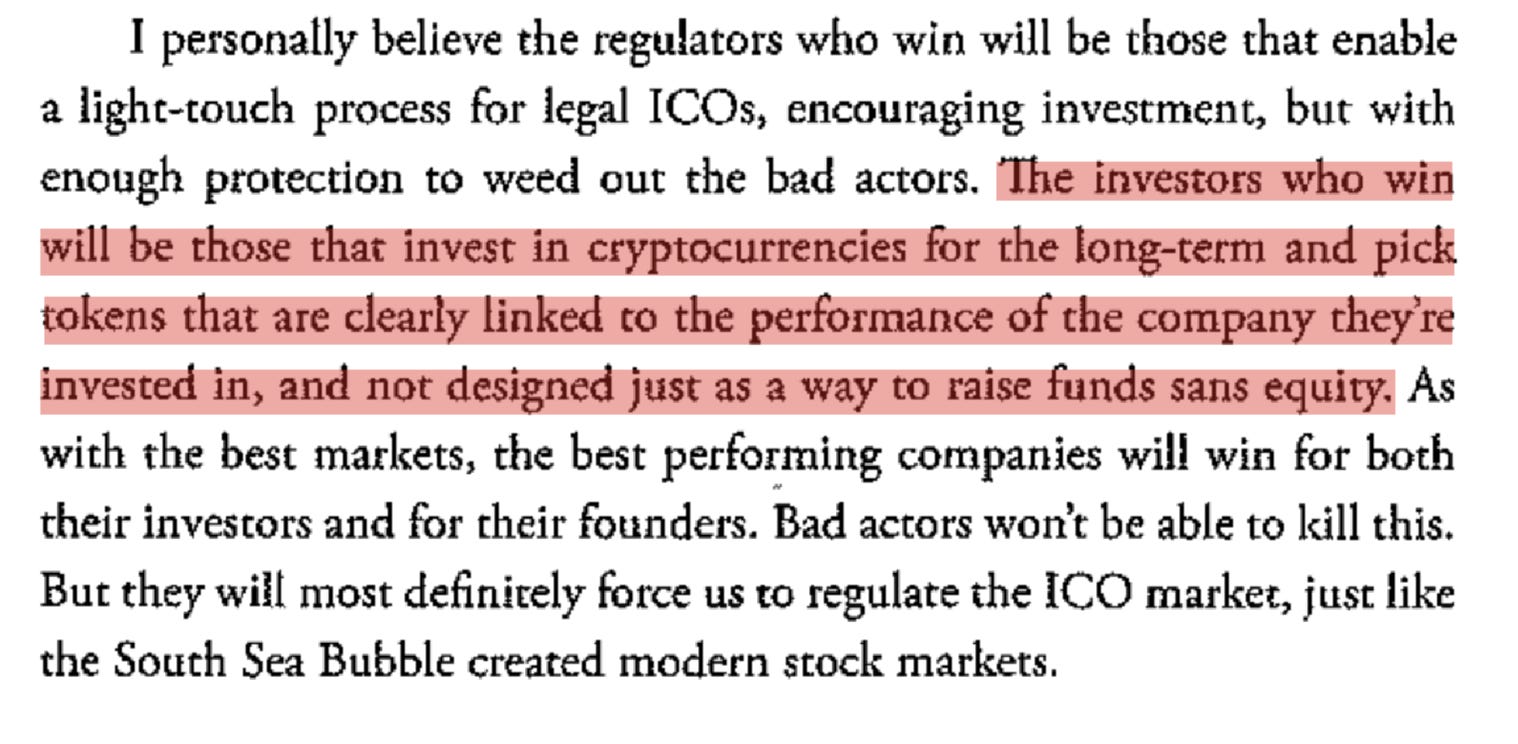

In this book, the crypto pages are a time capsule. Back then, ICOs were the “killer app.” John McAfee promised Bitcoin would hit a million dollars. I want to believe him still. A little embarrassing to read now, but it remains an essential read because we look back to “First principles.”

Eight years on, that’s what the phrase has come to mean. Crypto, for all its dead tokens and noise, is one of the few places running the experiment for real, asking what money even is when you start from zero. Some of the answers are junk, but we see that for what it is. King dared banking to picture itself starting today. Almost nothing around us would survive the question. And we’d keep it anyway.

First principles is a beautiful idea. But using it means you look at the thing you’ve served your whole life and admit you might not build it again. So the idea stays admired and unused.

That’s it about Bank 4.0, see you next week with another one.

Stay tuned.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.