A central planner walks into a store. The shelves are empty. He says: “See? No demand.”

That’s an old joke among the economists about the soviet union.

Stuck in that same loop, we have neobanks. Five hundred startups built checking accounts that 1.4 billion people actually used. But making money out of it has been tough.

76% of neobanks are still unprofitable. The average neobank earns $45 per user per year. A traditional bank earns $350.

It comes down to the product you chose to build at the beginning, and whether that product has any real margin in it.

To understand why everyone chose what they chose, you have to look at what they were running from.

Traditional banks were bleeding people dry. They even charged you at the ATM just to take out your own paycheck. If you grew up without much capital, it's even worse. When the first neobanks showed up offering accounts with zero fees and no minimums, people chose that.

Soon, hundreds of millions of users joined. Today, Nubank serves over 60% of the adult population in Brazil. Local banks treated regular customers like an annoyance, which made that growth inevitable.

But it didn’t work out for the companies.

When you swipe a debit card at a coffee shop, the merchant pays a small fee, which is capped at around 22 cents on a $40 purchase under Federal Reserve Regulation II. That fee gets split across the card network, the bank, and the processor.

The neobank’s cut is thin. And thin, multiplied across millions of users who treat their neobank as a spending account, does not add up to a business. They keep their mortgages and investments somewhere else.

Traditional banks don’t make money when you borrow. Spending and transactions add just a tiny bit.

Banking profitability has been about credit, the interest on your mortgage, your car loan, and so on. Payments are how banks see you every day. Lending is how they make money from you. Neobanks were unprofitable because of that. You can’t just hand out loans and charge interest on a massive scale without a banking charter. Most neobanks started out as tech platforms built on top of other banks’ licenses, which meant their hands were tied legally when it came to major lending.

Nubank started in Brazil back in 2013 with a free credit card. At the time, the big traditional banks there were charging massive interest rates. So it worked out for Nubank, and they ended up getting 131 million users by 2026.

Nubank is worth $60 billion today. The free accounts were a way to get people to download the app. The profit comes from lending.

Out of their $15.8 billion in revenue last year, most of it came from credit cards, personal loans, and interest. In fact, their personal loan business grew so fast it became their biggest moneymaker. Nubank didn’t survive by inventing a new type of tech. They survived by lending money. The nice app was just the hook to get people in.

Revolut found a new way to make money. By 2025, it reported £1.3 billion in net profit. Revenue increased by 46%, reaching £4.5 billion, marking its fifth consecutive profitable year. The company’s profits mainly came from forex fees, subscriptions, crypto and lending book. Lending portfolio doubled in size with 120% growth YOY, reaching $2.9 billion. They developed these features because they had early revenue from exchange fees and subscriptions. This income gave them the time they needed to grow their lending business quietly.

Chime took the longest to figure this out. They survived almost entirely on interchange fees. Getting customers in the US is incredibly expensive, the margins on the card swipes are tiny, and you only make money when people are actively spending. If they stop swiping, your revenue goes to zero.

By 2025, Chime brought in over $2 billion in revenue but still posted a billion-dollar loss, mostly because of massive stock payouts for its IPO. They went public at an $11 billion valuation. The stock took a hard hit within months. But then, in the first quarter of 2026, they made a profit of $53 million for the first time in 12 years. Why? Because their lending products finally took off. Their paycheck advance feature was on track to clear $400 million, and their instant loans blew up.

In June 2026, a developer at Nubank accidentally activated a liquidation protocol during a routine software update. A push notification and email were sent to many customers, stating that the central bank had liquidated the bank and explaining how to claim their money from the deposit insurance fund. Co-founder Cristina Junqueira had to apologise on Instagram. She said the incident was a “bizarre” operational error. The bank and the user's money were safe and sound. But for a few minutes, a stupid mistake made it look like the company had disappeared.

To be fair, old banks do this all the time, too. Like accidentally wiring a billion dollars because of a typo. But a giant like Citi keeps rolling because it’s been around since 1812. The old banks are just terrible at tech, and the new apps are still learning how to be banks. Citi glitches, people just assume it’s a corporate mistake because they’ve been around since 1812. If people think a startup bank is failing, they run.

In April 2024, Synapse filed for bankruptcy.

Neobanks are just software companies. To offer checking accounts, they have to stitch together a web of partners behind the scenes. Synapse was the middleman connecting over a hundred different neobanks to the old-school banks holding the cash. Synapse managed the books, ran the compliance checks, and kept track of who owned what.

When Synapse went out of business, its records went with it. Around $265 million in customer money was put on hold. The partner banks had no idea which money was which users’ and discovered that $95 million had gone missing. That was a complete lack of accountability. While people were unable to access their preferred banking apps, like Yotta and Juno, for several months, some were even blocked from making their mortgage.

If one of your favourite banking apps relies on a bank that it doesn’t control, and a middle bank that it doesn’t control, then it’s an elaborate fake. The system is built to fail.

At the end of the day, the only protection against a mess like that is a banking license. Neobanks always said they didn’t need one.

I wrote last October that crypto neobanks seemed to be the real deal. Regulation was clear, and people had wealth on-chain and wanted to spend directly from it. What I wrote is still true. But I completely underestimated how infrastructure built on a partner bank would include whatever breaks in a partnership with them.

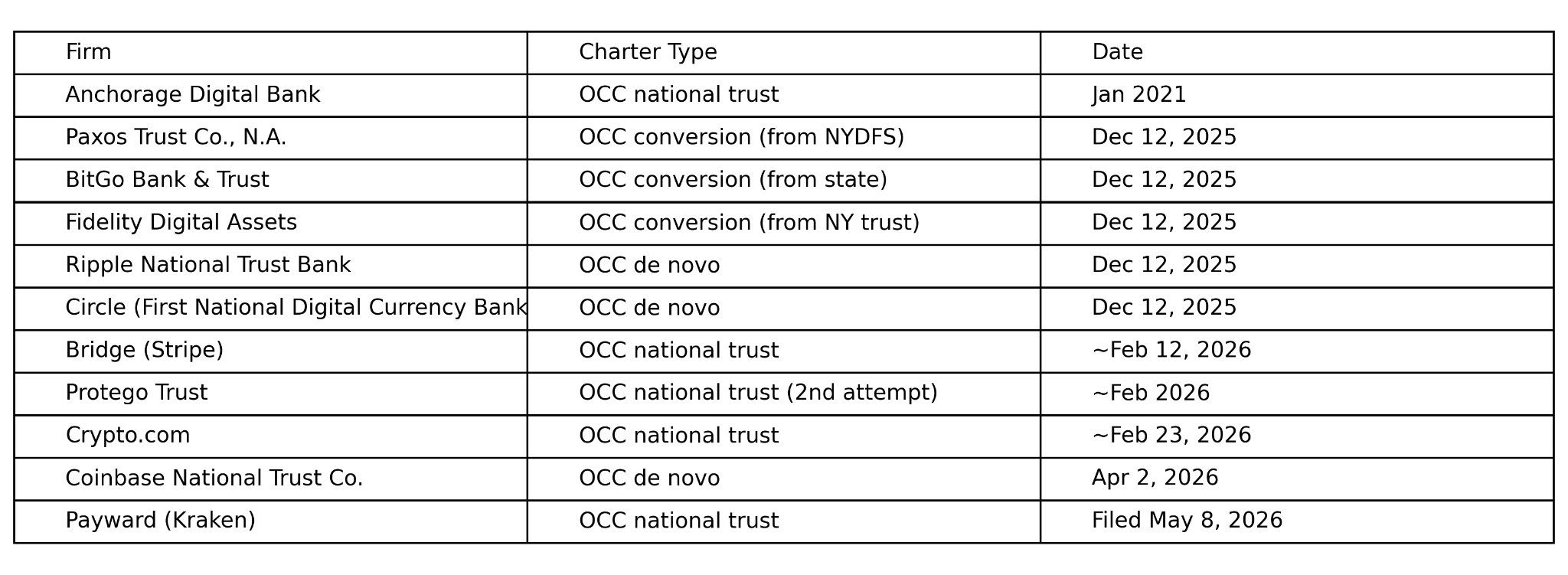

The response from crypto has been to abandon the charade and start doing. From December 2025 to May 2026, the OCC ‘conditionally approved’ about 10 crypto and FinTech national trust charters. That’s already more than the total in the previous decade. Paxos, BitGo, Fidelity Digital Assets, Ripple, Circle, Bridge (which Stripe acquired for $1.1 billion), Crypto.com. They all applied for the same charter in the US that the neobanks claimed they didn’t need (because they didn’t want it).

Because a national trust charter is the ultimate escape hatch from the middleman trap. It gives these companies a direct stamp of approval from the federal government to hold customer assets, settle payments, and operate across all fifty states under a single rulebook. They no longer have to beg traditional partner banks for permission to exist, and they don’t have to risk their entire business on invisible middleware like Synapse.

Crypto companies realised that if you want to move billions of dollars without getting riddled by the plumbing of an old-school bank, you have to buy your way into the federal system.

Read: Charters, Keys, and Control 🔐 - by Prathik Desai

Kraken’s parent Payward now has three different regulations in the US. This includes a charter from Wyoming, a Federal Reserve master account that was secured in March 2026, and an OCC national trust application from May 2026. SoFi also got its OCC charter in 2022 by acquiring Golden Pacific Bancorp. In December 2025, SoFi launched a dollar-backed stablecoin, which was the first stablecoin issued by a US national bank built on a public, permissionless blockchain. By May 2026, it was available to 14.7 million members to hold, spend, and convert within the SoFi app. Mastercard became a settlement partner for SoFi. Coinbase started moving BTC-backed loans through Morpho on the Base chain and by early 2026 had more than $1.4 billion in collateralised BTC.

SoFi’s evolution is unique - student loan refinancer to a neobank to chartered bank to stablecoin issuer. It has one of the first complete stories in the space.

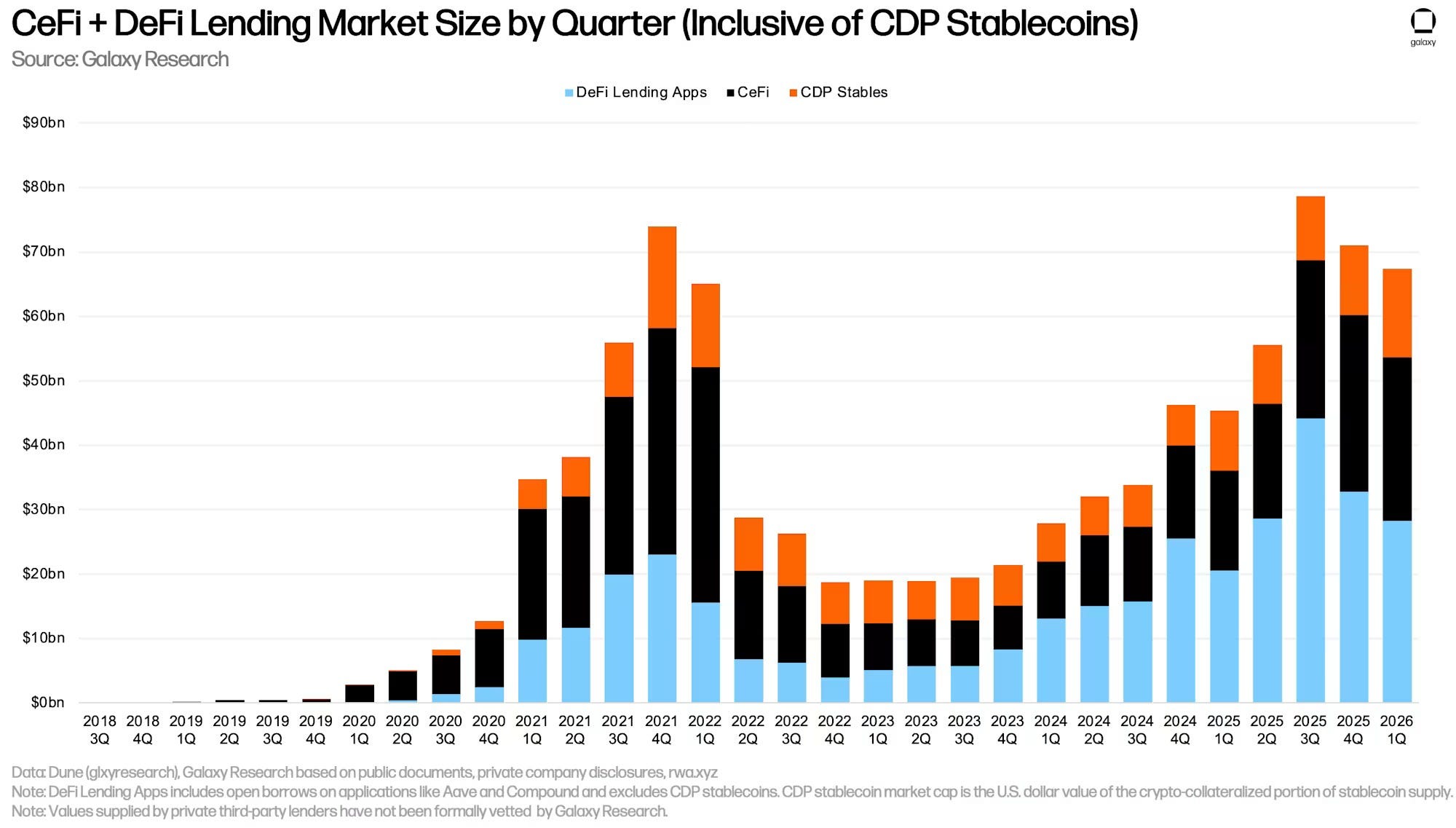

The remaining gap is unsecured lending. Total crypto collateralised lending across CeFi and DeFi combined is $67.42 billion.

The real unsecured lending throughout DeFi only amounts to $24 Million. The protocols that attempted to tap into the unsecured lending market (i.e. Goldfinch, early Maple, or TrueFi) have all either pivoted toward fully collateralised lending models or are in the process of shutting down. Maple is now the largest lending protocol in DeFi and operates at 160% collateralisation.

Read: The Lenders’ New Rails - by Prathik Desai - Token Dispatch

On a pseudonymous blockchain, unsecured lending lacks a viable enforcement mechanism. In the real world, if you default on a loan, a bank can ruin your credit score or take you to court. In DeFi, there are no credit bureaus or repo men. If a borrower walks away with an uncollateralized crypto loan, they just abandon the wallet address, and the money is gone forever. DeFi protocols tried to fix this with soft reputation metrics, but they got hit with massive defaults and realised that without real-world legal enforcement, anonymous people just won’t pay you back.

Nubank lends to 131 million customers, many of whom do not have a credit history, using transaction behaviour for the lending underwriting process. This type of product does have a real economic value, but is very unattractive and operationally intensive. For someone to solve these particular infrastructure frontiers on the blockchain, they will most likely be required to obtain a banking license in order to do the same at scale. I expect the Office of the Comptroller of the Currency (OCC) waiting room to become more crowded.

Back in October, I suggested that the crypto neobanks were revisiting the themes which emerged about a hundred years ago. I said the tech will always change, but the way humans relate to money will always be the same. I intended there to be some beauty to that setup. And now it presents a different image.

The banks will always charge you to lend you your own money. The surviving neobanks came along with the promise to stop this, and the ones that did survive did it by... lending you your own money, but at better rates and better interfaces, yet by the same mechanism.

All I want to tell you is that:

“The more things change, the more they stay the same.” - Jean-Baptiste Alphonse Karr, 1849

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.