No open network survives its own success without losing its innocence.

Then the economics arrived. The people who build on it need revenue; the people who fund it need returns. Most people want reliability, which is the toughest to achieve.

makes a series of small adjustments, each defensible on its own, that cumulatively amount to something the founders would not have proposed at the start.To preserve that founding vision, the network

The early internet was supposed to be ungoverned and borderless. Then Yahoo had to remove Nazi memorabilia after French courts intervened in 2000. Then Facebook hired 15,000 content moderators. Then Apple built an App Store with rules. They were the price of operating at scale in a world with governments, regulations, and users who needed protection from each other.

The open network became a governed one because commerce required giving up the ideals. DeFi is going through the same adjustment, and Sky is the easiest example.

MakerDAO’s own Endgame governance document warned of US Treasuries: “The major downside is that they can be seized easily. Anything that can be seized by global powers may be at risk of seizure through legal means.”

The community that read that document, a few years later, voted to put $8 billion into US Treasuries.

Writing down exactly why something is dangerous and then doing it anyway is institutional self-awareness (that’s me learning to accept things as they are). So I am not going to call it cognitive dissonance, or corruption, but a clear-eyed calculation that the risk is worth taking for reasons that can be articulated. Most institutions suppress the doubt. MakerDAO published it in its governance documentation and proceeded regardless.

I find that more grounded than most things I read in this industry.

To those who don’t know, Sky is not a lending protocol in the way Aave or Morpho are. Users do not deposit US Treasury bonds as collateral to borrow money on Sky. What Sky does is closer to what a central bank does.

It holds assets on its own balance sheet to justify the currency it issues. Users deposit USDS or DAI, earn the Sky Savings Rate, and the yield comes from the interest Sky earns on its Treasury holdings.

This structure has a name outside crypto. You deposit your capital into a protocol that immediately puts it to work in US government bonds. Once the government pays out the interest, the protocol skims a portion off the top for itself and routes the remainder back to you as a yield.

Yes, that’s a money market fund.

It is what Fidelity’s SPAXX does. It is what JPMorgan’s government money market fund does. It is what every bank savings account does at a structural level, except that those banks are regulated, your deposits are insured, and the yield is lower.

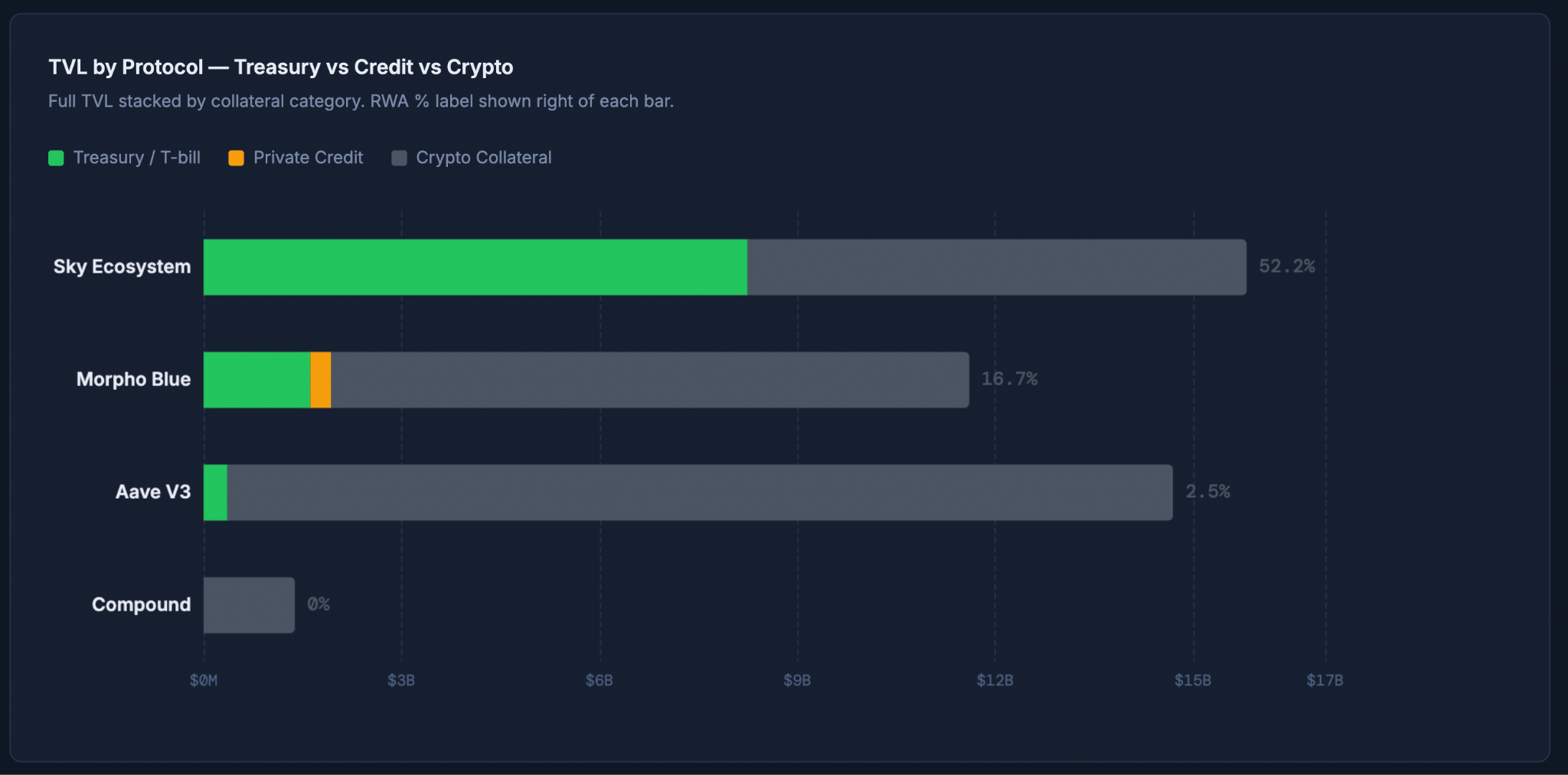

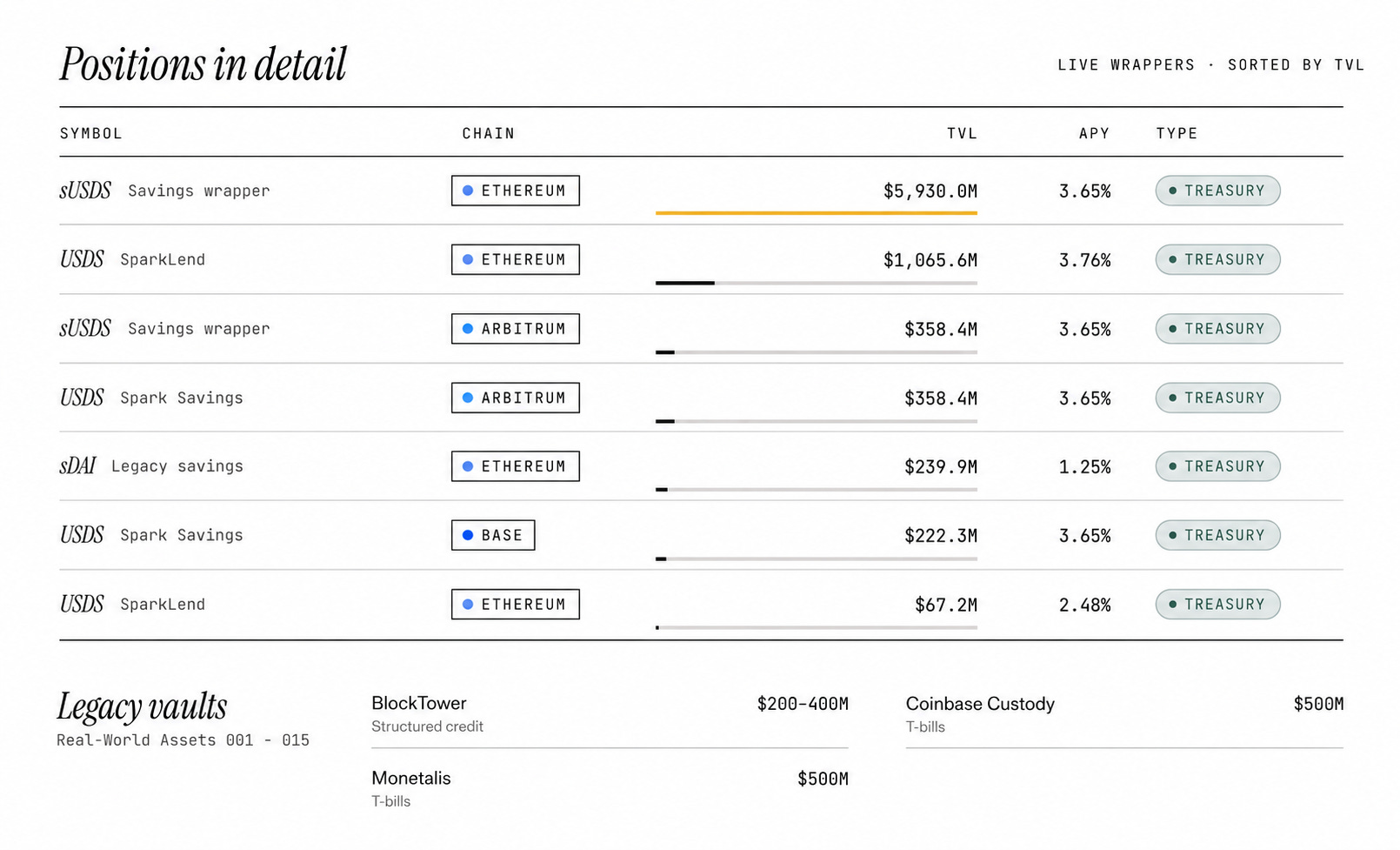

Sky is now a money market fund that operates on Ethereum. Its depositors believe they are using decentralised finance. In reality, they are lending money to the US federal government through an on-chain wrapper. sUSDS holds $5.9 billion in US Treasury-backed collateral. Sky’s total RWA exposure is $8.245 billion, which is 52.2% of its total value locked (TVL) and 78% of all RWA deployed in DeFi lending. We’ve funnelled everything down to a single protocol trading a single country’s debt. DeFi became a more efficient way to interact with the same system.

I find this less upsetting than I expected to.

All of this was a series of choices. It began in November 2020 with a $20 million debt ceiling for 6s Capital’s real estate loans. Because crypto-native collateral was too “volatile” to scale DAI, and real-world assets (RWA) offered a way to break free from the ETH price cycle. The community agreed and voted yes.

From there, things shifted. Monetalis Clydesdale pushed T-bill exposure to $1.25 billion, followed by Coinbase Andromeda’s $500 million Treasury investment, and then big players like BlackRock’s BUIDL and Janus Henderson. Each move had its own reasoning, like yield stability here, DAI supply growth there, but they all pointed to one thing. The Sky Savings Rate needed an engine, and RWA was the only thing strong enough to drive it.

The breaking point was in March 2023, when Silicon Valley Bank collapsed, and USDC lost its peg; DAI fell with it. A stablecoin designed to eliminate counterparty risk had simply traded one middleman for another. But the community did not back down because if you have to rely on a counterparty, the US government is a safer bet than Circle. Please argue with that logic if possible.

By 2025, RWA generated 60% of Sky’s revenue. You just read the reality of surviving at scale.

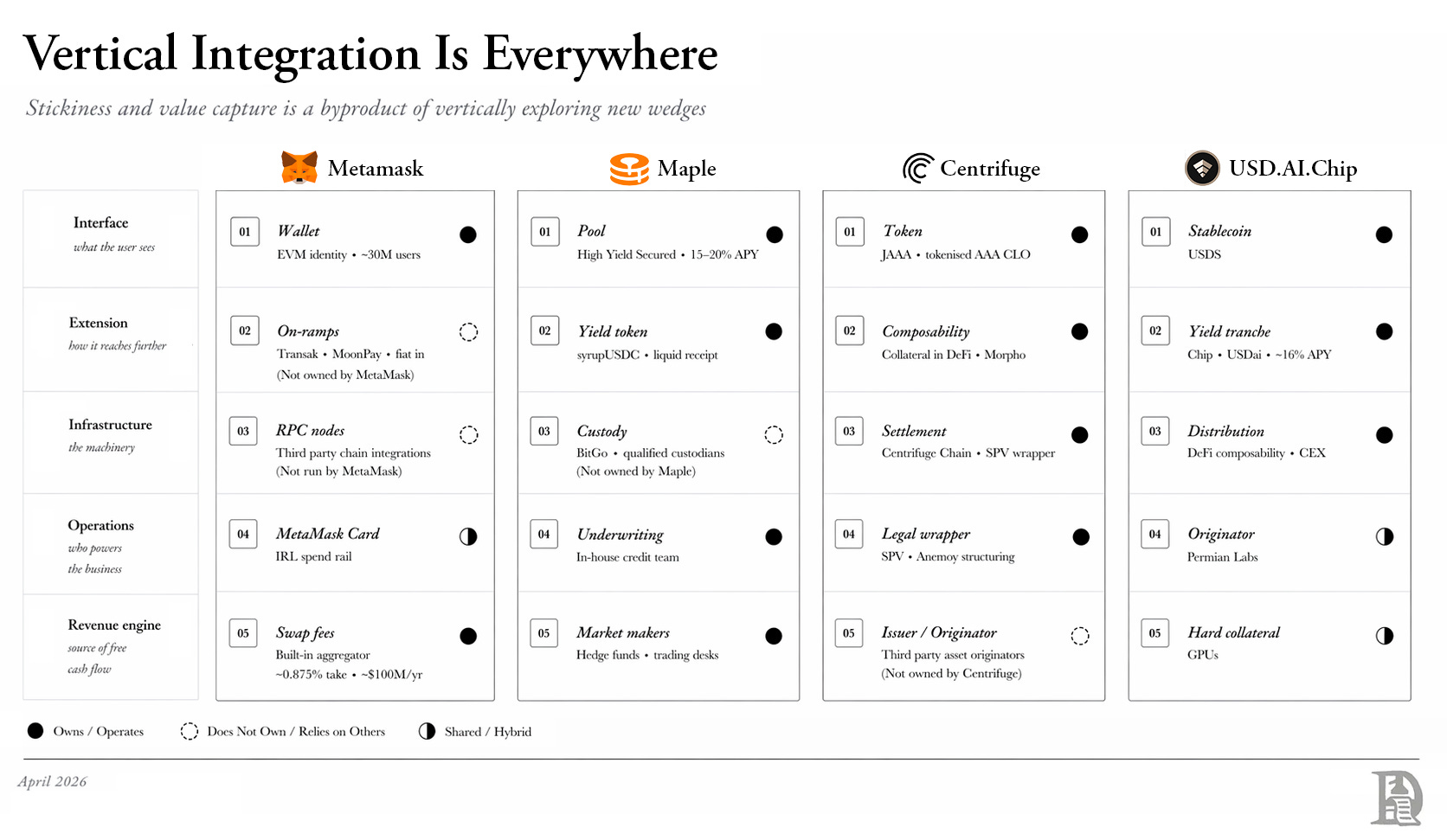

Looking across DeFi today, the protocols that are building durable businesses are the ones that own multiple layers of their own stack. Maple owns the credit origination, the yield token in syrupUSDC, the underwriting process, and the market-making relationships. It does not outsource the parts that determine its margins. Centrifuge owns the institutional token in JAAA, the composability layer through Morpho, the settlement infrastructure, and the legal wrapper through Anemoy structuring. USD.AI is building its own stablecoin, its own yield tranche, its own distribution across DeFi and CEX simultaneously, and even its own hard collateral in GPU infrastructure through Permian Labs.

The margin in crypto increasingly comes from capturing the entire supply chain rather than owning a single piece of it and relying on others for the rest. A protocol that owns only the smart contract layer, not collateral sourcing, yield generation, or distribution, depends entirely on others for its economics.

Sky owns the stablecoin, the savings-rate product, the collateral-management function, the distribution through Spark across multiple chains, and the institutional counterparty relationships with BlackRock, Janus Henderson, and Superstate. No competitor owns all of those layers at the same time. That is why it has $15.8 billion in TVL and generates the majority of its revenue from the RWA allocation it controls directly, rather than from fees on collateral it does not choose.

The protocol built a vertically integrated financial product that scales, and it is not alone in this. Every protocol building a durable business in 2026 is doing some version of the same thing. Joel John at Decentralised.co says that the protocols winning today own the supply chain, not just a layer of it. Maple owns its credit underwriting. Centrifuge decided they couldn’t scale without owning their own settlement chain and legal wrappers. Hyperliquid took the same path, vertically integrating everything from the risk engine to the front-end interface.

There is constant tension between creating a protocol that functions well at scale and holding onto the “pure” decentralised vision we began with. Sky was the first major player to acknowledge that the vision needed to adapt to business demands. In the end, the protocols that don’t make that trade usually don’t survive to tell the story.

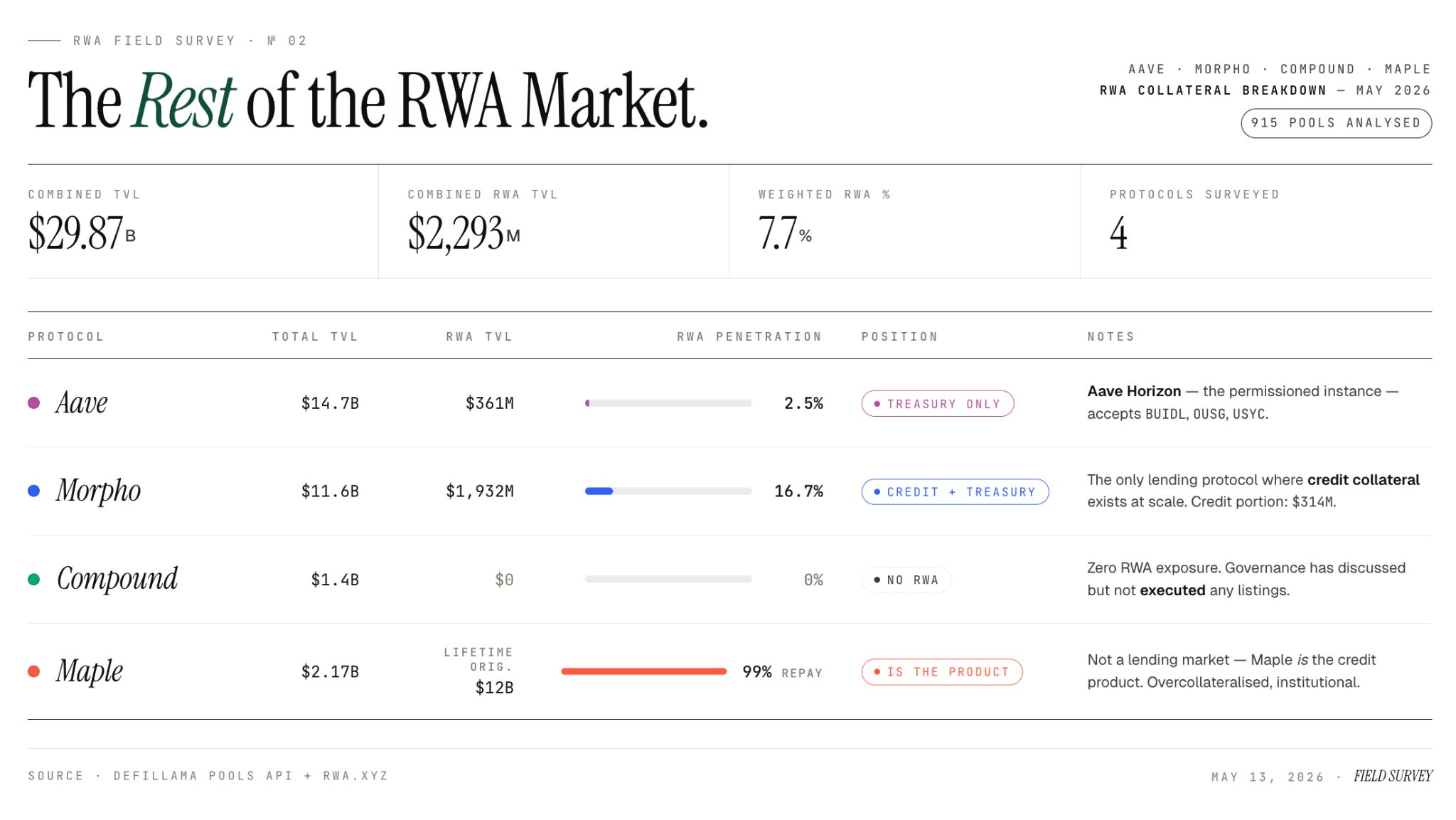

The rest of the RWA market is smaller. Morpho is the only lending protocol in which the original credit idea is used as collateral. Its RWA exposure consists of about 84% Treasuries and 16% credit. This includes $314 million in credit products from Fasanara’s private credit vehicle, Apollo’s Diversified Credit Fund, and SG-Forge’s MiCA-compliant stablecoins.

Morpho’s permissionless setup allows credit originators to create isolated markets without needing a governance vote, and they are doing just that. Fasanara increased its amount from zero to $190 million in three months. Apollo brought institutional credit on-chain through Securitise. Pareto and FalconX developed credit vaults using zero-knowledge KYC. The credit experiment is happening in one place because one protocol was designed to allow it to operate without prior permission. If tokenised credit is ever going to show its value as lending collateral in DeFi, Morpho will be the source of that evidence, and it will arise from $314 million, gradually growing into something larger.

Read: Morpho Is Becoming the Backend - by Thejaswini M A

Maple stands apart from other protocols. It ranks as the 30th largest DeFi protocol by total value locked (TVL) at $2.17 billion. Unlike typical lending markets, it does not accept user credit as collateral. Instead, Maple itself serves as the credit product. It has achieved $12 billion in lifetime originations, with a 99% repayment rate since its 2022 model. The protocol is fully overcollateralised, featuring institutional-grade underwriting conducted by its in-house credit team.

Maple has rebuilt itself after losing 90% of its active loans during the FTX collapse. It returned with a model that has proven effective. It has excelled in the credit sector as a standalone product .

Rather than acting as passive collateral within a broader liquidity pool, Maple has carved out a niche as a primary lender. It has shifted from being a component of the money markets to a destination for credit, handling the entire lifecycle from risk assessment to final settlement in-house.

There is $10.26 billion in Treasuries acting as DeFi lending collateral, while only $314 million is in credit. This gives a ratio of 97:3.

In this context, “credit” refers to private sector lending, financing real-world business activities like corporate debt or fintech loan books. While Treasuries are essentially a bet on US interest rates, credit is about backing commercial risk for a higher, non-correlated margin.

The original DeFi pitch focused mostly on eliminating the middleman and a system that didn’t require central bank approval. That’s what attracted everyone. But it changed thanks to the reality of incentives.

Sky depositors are mainly funding the US federal deficit through an Ethereum-shaped straw. A protocol designed to eliminate the need for trust is now supporting the most powerful government in the world. Sky did something uncommon for a major organisation. They put the risks in writing, debated them publicly, and then agreed together that the yield was worth the trade-off. Strategic pivots shouldn’t be mistaken for a betrayal of values. We have learnt it the hard way.

The underground station loved being “off the grid” until they realised they needed a bigger antenna to reach the city. To get the signal, they had to buy the license and follow the script.

I’ve stopped being surprised by this change. Once you notice the economic forces pulling these protocols toward the Treasury, it seems inevitable.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.