Hello,

In 2025, brokerage firm Charles Schwab earned $11.75 billion in net interest revenue. That was about half of its total revenue for the year. Schwab earned this by sitting on its clients’ idle cash, not by trading stocks on their behalf or advising them.

When a client sells a stock and doesn’t reinvest the surplus cash, Schwab moves it into safe, short-term assets. It keeps the spread between what it earns on these investments and what it passes on to its customers.

This is not unique to Charles Schwab, though. It’s called a float business, something most investment and trading intermediaries do. Except, a new class of depositor is emerging - human-coded software - which will likely create one of the biggest float opportunities.

These agents need funded wallets with stablecoin balances parked in advance. Whoever custodies those balances will earn the spread on idle capital and a fee on every micro-transaction flowing through the agentic stack. That’s two revenue streams compounding off the same deposit base. Every major player from Circle to Visa is now racing to capture it.

In today’s analysis, I will explain what this opportunity means for companies trying to earn in the age of agentic payments.

Onto the story,

Prathik

The Appeal of Float

Every significant financial intermediary in history has built one of its most reliable cash flows from idle money. In its S-1 filing 24 years ago, PayPal disclosed earning a 3.8% blended yield on customer balances in 2001. That yield was PayPal’s primary revenue source before its transaction fees scaled.

The habit persisted as financial institutions evolved. Robinhood ended 2025 with $1.5 billion in net interest revenue, more than a third of its total revenue.

For trading intermediaries and investment advisory businesses prone to cyclical downturns, income from holding customer deposits is often the most reliable revenue stream.

Now imagine what happens when the depositor is not a person but a piece of software that autonomously buys compute, calls APIs, books services and pays other such software. Think AI agents. All these agents need funded wallets with balances parked in advance, ready to be used whenever triggered.

This need for working capital forms the base for building a similar float opportunity in the emerging agentic economy.

Nothing about this opportunity should surprise you. That’s how money has always worked. Whenever it sat idle, even for hours, someone always found a way to make it productive.

The Machine’s Savings Account

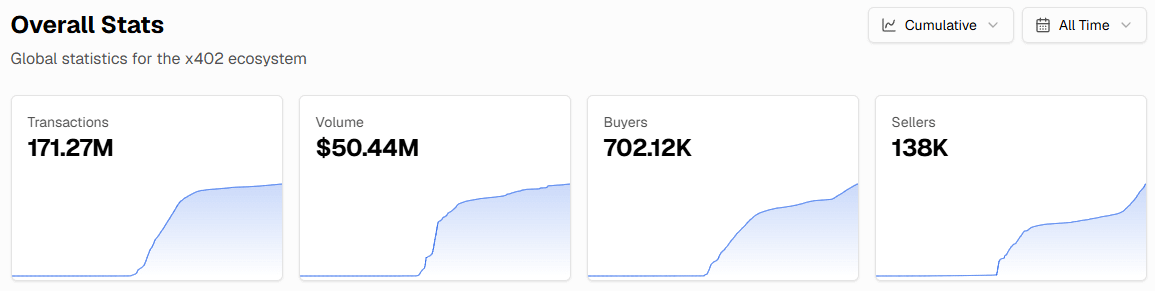

In September 2025, Coinbase and Cloudflare launched the x402 protocol. It allows AI agents to pay for a web resource, like a data feed, a compute job, or an API call, by attaching a stablecoin payment directly to the HTTP request. It removed humans from the loop by not requiring any checkout page or card numbers.

So far, the protocol has processed more than 171 million transactions, with cumulative volume exceeding $50 million. Each of those millions of transactions requires a pre-funded agent wallet that has a stablecoin balance sitting idle until it is spent.

Anyone who has studied the Schwab or PayPal playbook understands that the jackpot lies in the custody of working capital and in earning the spread on it.

Although the agentic numbers are currently insignificant relative to global payments, they represent an opportunity that didn’t exist about eight months ago. Machines paying machines, settlements happening in stablecoins and transactions being processed at sub-cent fees and sub-second finality would have sounded like futuristic ideas a year ago.

Now the world is betting on this opportunity.

The Fight for Float

There are two ways to make money from agentic payments. The first is to charge a small fee for every transaction. The second is the float, where the wallet provider earns interest on idle balances sitting in agent wallets.

USDC-issuer Circle is betting on doing both by building infrastructure to hold agentic wallet balances and process their transactions.

Earlier this month, Circle launched its Agent Stack, which includes a suite of agent wallets, a nanopayments protocol that settles transfers as small as $0.000001, and an agent marketplace.

I wrote here about how the agentic layer helps a stablecoin issuer whose primary income so far has been earning interest on treasury bills.

Read: From Issuance to Infrastructure

For Circle, a human holding $1,000 in USDC might move it once a month. But an AI agent holding $100 might execute hundreds of micro-transactions a day. If Circle can integrate these idle balances via smart contracts and deploy the capital into yield-bearing primitives such as staked treasuries or other short-term yield-bearing assets, it can pocket the spread and earn a nanopayment fee on every transaction flowing through its rails. The two revenue streams compound off the same deposit base.

In February, Coinbase launched Agentic Wallets. These are purpose-built, non-custodial wallets with programmable spending limits, session caps, and gas-free transactions that settle on the Base network.

SkyfireAI, founded by ex-Ripple executives, calls itself “Visa for the AI economy” and is building alternatives to traditional card rails by charging fees in the tens of cents to process agentic transactions.

Traditional payment giants aren’t missing the opportunity either.

In March 2026, Banco Santander completed Europe’s first live end-to-end payment executed by an AI agent using Mastercard’s Agent Pay. In December 2025, Visa announced it would list the Visa Intelligent Commerce platform in AWS Marketplace for developers and enterprises building towards agentic commerce. In the same month, Stripe launched its Agentic Commerce Protocol to enable pay-as-you-consume micropayments that settle in stablecoins.

From crypto-native rails to card networks, to big tech and startups, everyone is racing to be where the agents park their cash.

But how big is the pie they are fighting for?

The AI Float Opportunity

Microsoft projects 1.3 billion AI agents to be in operation by 2028. I understand these are just consultant projections and not realised volumes. Treat it with the scepticism any forward-looking estimate warrants. But let’s consider what this opportunity means for a company like Circle.

In March, Circle’s marketing head, Peter Schroeder, posted that USDC accounted for 98.6% of the 140 million transactions AI agents made over nine months.

The cumulative volume of $43 million is still negligible. But if Circle can scale the agent deposit base to $1 billion, then it’d add $40 million in annual income at a ~4% yield. If Circle deploys capital into other DeFi primitives, it adds an additional $10 million to its income for every percentage point of yield the primitives offer above the risk-free rate.

For context, Circle’s total reserve income from all of USDC’s $77 billion in circulation was $653 million in Q1 2026.

The yield on agent deposits complements its treasury income when interest rates are low.

Doing Business in a Post-Agentic Era

Circle’s marketing head noted that the average transaction size across 140 million payments was $0.31. Traditional payment companies like Visa and Mastercard charge interchange fees that often exceed $0.20 per swipe. The system that charges 20-cent fees per transaction cannot process a 31-cent payment. Its math is almost comical. This is why companies are rushing to build agent-specific protocols with different fee structures.

The impact of the agentic economy extends beyond payment companies. The agentic economy rewires how every business on the internet will be paid. The primary consumers of web content are soon shifting from humans to AI agents. An AI agent surfing through hundreds of articles to answer a user’s query won’t see the banner ad next to it. This topples the entire advertising model that funds most of the web’s content based on human eyeballs.

Stablecoin-enabled micropayments replace this model with a pay-per-request system that lets agents pay a few cents per article click. The content management systems (CMS) on the web are also evolving to integrate the new business model that is native to AI agents. Last month, Cloudflare and x402 launched EmDash, an AI-native open-source CMS that supports a pay-per-request model for AI agents.

In the post-agentic era, protocols like x402 can turn any point on the web into a pay-per-request service.

What happens if the businesses don’t adapt and offer AI-native payment options?

Consider a SaaS company that offers monthly and yearly subscription packages for its APIs. If it doesn’t offer a pay-per-request option, the AI agents will just use a competitor that does. The agent will show no loyalty like a human would.

This forces a re-pricing of the internet economy.

Businesses will be forced to repackage their products through micropayments that are so frequent that they add up to sizeable revenue. The companies that expose their services behind the paywalls of x402 and similar protocols earliest will capture the agent traffic.

Agentic wallets will also have a trust layer around programmable spending conditions, session budgets, and audit logs to enable monetisation. Whoever builds this layer will own the deposit base, the resulting fees, the float, and the overall yield.

Companies will still face regulatory obstacles, as they have with every other new technological adoption. Whether agent working-capital balances will be classified as deposits, e-money, or something else is still undecided. Stablecoin yield restrictions debated in Congress as part of the CLARITY Act could decide who captures the spread.

Irrespective of which side the regulation leans, what is inevitable is that idle money won’t stay idle for too long. Participants always find a way to capture value by targeting market inefficiencies. That’s the natural course of markets.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.