I am writing this from Bangalore, which is UTC+5:30, which means the US stock market opens at 7 pm my time. I have covered crypto markets for 5 years, which means I have spent 5 years watching markets that never close. We don’t have a trading halt. Neither do we have a pre-market or after-hours distinction. Just continuous movement, whether I am asleep or awake, whether it is Saturday or the middle of a geopolitical crisis.

Financial markets in general are not built this way. The New York Stock Exchange runs from 9:30 am to 4 pm Eastern, Monday through Friday. London runs 8 am to 4:30 pm. Tokyo runs 9 am to 3:30 pm, with a lunch break.

When one closes, the next opens, more or less. What I am saying is, capital should move continuously because the sun is always up somewhere. In practice, every major exchange has hours, creating long periods of downtime when regulated markets are closed.

There was a reason why it was designed this way. It grew from the physical constraints of people standing in rooms and shouting at each other. Computers were supposed to fix it. They made the shouting faster and still kept the schedule.

An object at rest stays at rest until something acts on it. That’s what we studied in school. The financial market schedule stayed because nothing forced it to move. Then, on a Sunday morning in May, someone wanted to price SpaceX before the bankers did. Hyperliquid was open. The contract launched at 5:16 am UTC. $33 million moved in 24 hours. Morgan Stanley had not yet opened the books.

The Indian time zone turned out to be the right schedule for this story. The US financial press wakes up at 9:30 am Eastern. By then, I had been watching markets for most of the afternoon.

CME Group (Chicago Mercantile Exchange) is the largest derivatives exchange in the world. That’s where professional traders buy and sell futures on oil, gold, interest rates, stock indices, and Bitcoin. Trillions of dollars in daily volume, and they have been around since 1898.

ICE (Intercontinental Exchange) owns the New York Stock Exchange. Also owns derivatives exchanges globally. Another titan.

These are the most powerful financial market infrastructure companies on earth. It’s tough for regulators not to listen to them when they point at something and call it dangerous.

CME and ICE are lobbying the CFTC and Capitol Hill to crack down on Hyperliquid, warning that the KYC-free platform is a breeding ground for market manipulation and sanctions evasion.

There’s zero KYC here. While Hyperliquid uses a frontend filter to block OFAC-sanctioned addresses on its main website, the underlying protocol is fully permissionless. If someone bypasses the website and interacts with the smart contracts directly, there’s no identity check waiting for them.

There are no position limits on Hyperliquid. On CME, no single trader can hold more than a certain size position in any contract. That prevents manipulation and systemic risk. Hyperliquid has no such limits.

CME monitors trading patterns for manipulation, such as spoofing, wash trading, and coordinated attacks. Hyperliquid has no surveillance system watching for this.

Fair points.

HYPE dropped 9% on May 15 on news. Two market makers pulled $100 million in liquidity on May 18 in response.

But watch which specific product they flagged. Not Hyperliquid’s crypto perpetuals, which have run for years without regulators blinking. The focus was on the oil contracts. The contracts that traded $720 million over a weekend when CME’s own oil markets were dark.

CME and ICE aren’t entirely wrong about the regulatory headache here, but we also know they aren’t neutral bystanders. Their business model relies on a legally protected monopoly over the trading calendar. They don’t mind competing on tech, but they absolutely lose their minds when someone competes on time.

By pulling real volume into oil over the weekend, Hyperliquid basically broke the space-time continuum of tradFi. And the incumbents are asking the government to force everyone else to go to sleep when they do. I’d rather ask permission to open on weekends; apparently, that’s just me

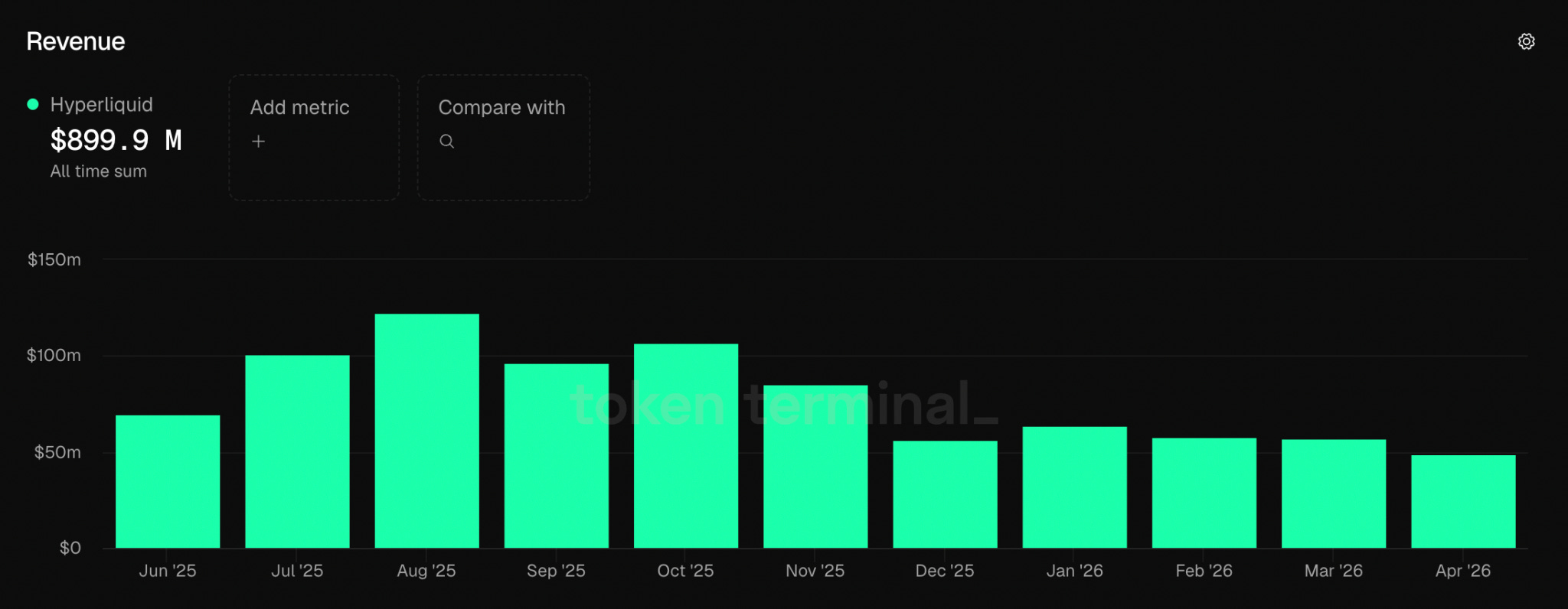

Hyperliquid has 11 people in a Singapore office. The protocol generated $51 million in revenue in the 30 days ending 21 May 2026. In March, it processed $2.6 trillion in notional derivatives volume.

Hyperliquid routed 97% of its trading fees into HYPE token buybacks via an on-chain fund. With 11 people generating $51 million in monthly revenue, the per-employee economics have no real comparison in crypto or outside it. HYPE is up 101% year-to-date as of late May.

All of this is not necessarily because Hyperliquid built a better derivatives product in any technical sense. It’s just open when CME is closed, which is enormously valuable. Recently, something new happened that extended this logic further.

On May 1, Trade.xyz, a platform built on Hyperliquid, launched pre-IPO perpetual futures for Cerebras, the AI chipmaker. The contract ran for two weeks before the IPO. Early in that window, traders implied a roughly 50% premium over the $185 IPO price, indicating an opening around $277. Then the market updated. One hour before Cerebras opened on Nasdaq, Trade.xyz’s perp was pricing the stock at $340, within 3% of the actual opening price. Cerebras opened at $350 on May 14, up 89% from its $185 IPO price. Traditional secondary platforms like Forge and EquityZen missed by 35%. Hyperliquid missed by 3%.

$277 was what the market implied when there was still genuine uncertainty. By the time the information had come in and been priced, the crowd had closed the gap. That is how price discovery is supposed to work.

Then on Sunday morning, May 17, Trade.xyz launched a perpetual futures contract for SpaceX. It opened at a $150 reference price, ran to $216 within hours, and finally settled around $203, meaning the crowd priced the company at a $2.4 trillion valuation.

But SpaceX hadn’t dropped a public S-1, no Wall Street analyst had touched a price target, and the official roadshow was nonexistent.

Traders had absolutely no idea that SpaceX had already slipped a confidential filing to the SEC on April 1, targeting a $1.75 trillion to $2 trillion valuation.

Traders settled the contract at $203, implying $2.4 trillion. The crowd landed at the top of the company’s own target range, before the bankers had their first meeting, without access to the filing. SpaceX officially and publicly filed its actual 277-page S-1 prospectus just a few days later on Wednesday, May 20.

Three products are currently trying to give investors exposure to SpaceX. Each one took a different bet on the legal surface.

PreStocks tried to get clever. They set up special investment funds (called SPVs) to buy actual SpaceX shares, then sliced those funds up into blockchain tokens so everyday investors could buy a piece. It looked like a clean backdoor into private tech companies.

Just before Hyperliquid launched its SPCX contract, Anthropic and OpenAI publicly disowned third-party SPV products that purported to track their valuations. Platforms in Hong Kong and UAE had been selling tokenised exposure to both companies without board approval. Both companies released warnings stating the share transfers behind these products were invalid. PreStocks tokens crashed 50%. When you own actual shares, the company whose shares you own retains the right to intervene.

Ondo Global Markets tokenises stocks through a US-registered broker-dealer, each token backed by the underlying security. The compliance is clean, and DTCC is building settlement infrastructure around it.

But Ondo’s greatest strength is also its biggest vulnerability. It has a physical address. If the SEC decides they don’t like it, they know exactly whose door to knock on. If Elon Musk objects, SpaceX lawyers know exactly which custodian to sue. By playing by the rules, Ondo makes itself a perfect target.

Read: Regulatory Asphyxiation - by Thejaswini M A

And then we look at Hyperliquid’s SPCX contract, which is built on absolutely nothing.

There are no shares, registered broker-dealers or claims on any physical asset. It is a synthetic perpetual, an absolute ghost. It’s a pure bet on a price ticker, settled entirely in USDC on a decentralised network.

If SpaceX wants to stop people from trading derivatives based on its valuation, it can’t. There is no corporate entity to serve legal papers to, and no central issuer to pressure.

It’s brilliant, really. Hyperliquid basically realised that you can’t get punched in the face if you don’t have a face. By anchoring the product to nothing physical, they became untargetable.

I am not sure this is straightforwardly good.

It is genuinely hard to argue against the national security nightmare of a zero-KYC venue routing trillions of dollars outside the global banking system. Hyperliquid co-founder Jeff Yan flying to Washington on May 17 to meet with policymakers shows just how live this pressure is.

Talking about Jeff Yan. He is a real human, he has a face, and he went to Harvard. If SpaceX wants to sue him for trademark infringement or intellectual property violation because his platform hosts a contract called “SPCX,” they can absolutely serve him with papers.

But suing Jeff doesn’t stop the contract.

With PreStocks, if the company deletes the underlying shares, the product ceases to exist. With Ondo, if a judge freezes the bank or custodian, the product struggles. But Hyperliquid’s SPCX is an autonomous code deployment. Even if Jeff Yan gets sued into oblivion, the smart contracts are already live, the code is immutable, and the global order book keeps running on-chain.

That is the immaculate theory of decentralisation. The practical reality is a bit more fragile. Hyperliquid runs on just 20 validators, not 900,000. They are identifiable. And the JELLY incident showed they will intervene when they choose to. The validators are not immutable.

Again, the clock is the only product they can’t copy.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.