Your parents did not think of it as an investment. They bought it because they needed somewhere to live, because the mortgage was manageable on one salary, because the neighborhood had good schools, because that is what you did. They painted the living room twice, replaced the roof once, argued about the kitchen for years and never renovated it. They raised children in it. They grew old in it. And somewhere along the way, without really trying, they built the most valuable thing they will ever own.

Now they are trying to figure out how to pay for healthcare, and the house is worth $1.2 million.

There is a number that keeps appearing in financial research right now: $124 trillion.

That is the estimated value of assets moving from older generations to younger ones over the next 25 years. Analysts call it the Great Wealth Transfer. It gets written about as though it is straightforwardly good news for the people receiving it.

Is it though?

The wealth being transferred is largely illiquid. Most of it is property.”Homes that boomers bought when prices made sense, paid off over decades, and watched appreciate into the primary store of their wealth. The generation inheriting those homes grew up watching the same prices make homeownership impossible for them. Now the homes are coming anyway, illiquid, emotionally loaded, legally complicated, and increasingly difficult to do anything useful with.

That is the problem the $124 trillion headline does not capture.

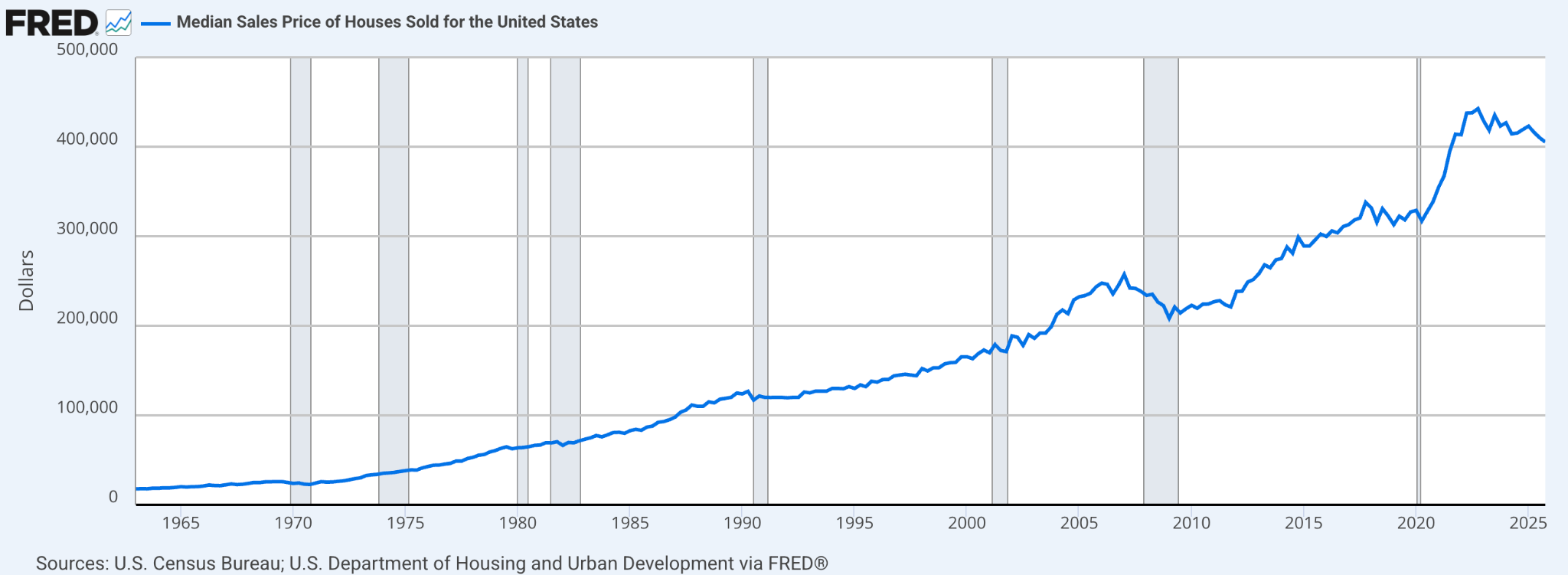

To understand why this matters, you have to understand what happened to housing between the 1960s and now. It changed categories. What began as shelter, a place to live, slowly became the primary financial instrument of the American middle class. For households outside the top income percentiles, the home is not one asset among many. It is the asset. Real estate equity accounts for the largest single line item on the balance sheet of the median American family, dwarfing retirement accounts, stocks, and everything else combined.

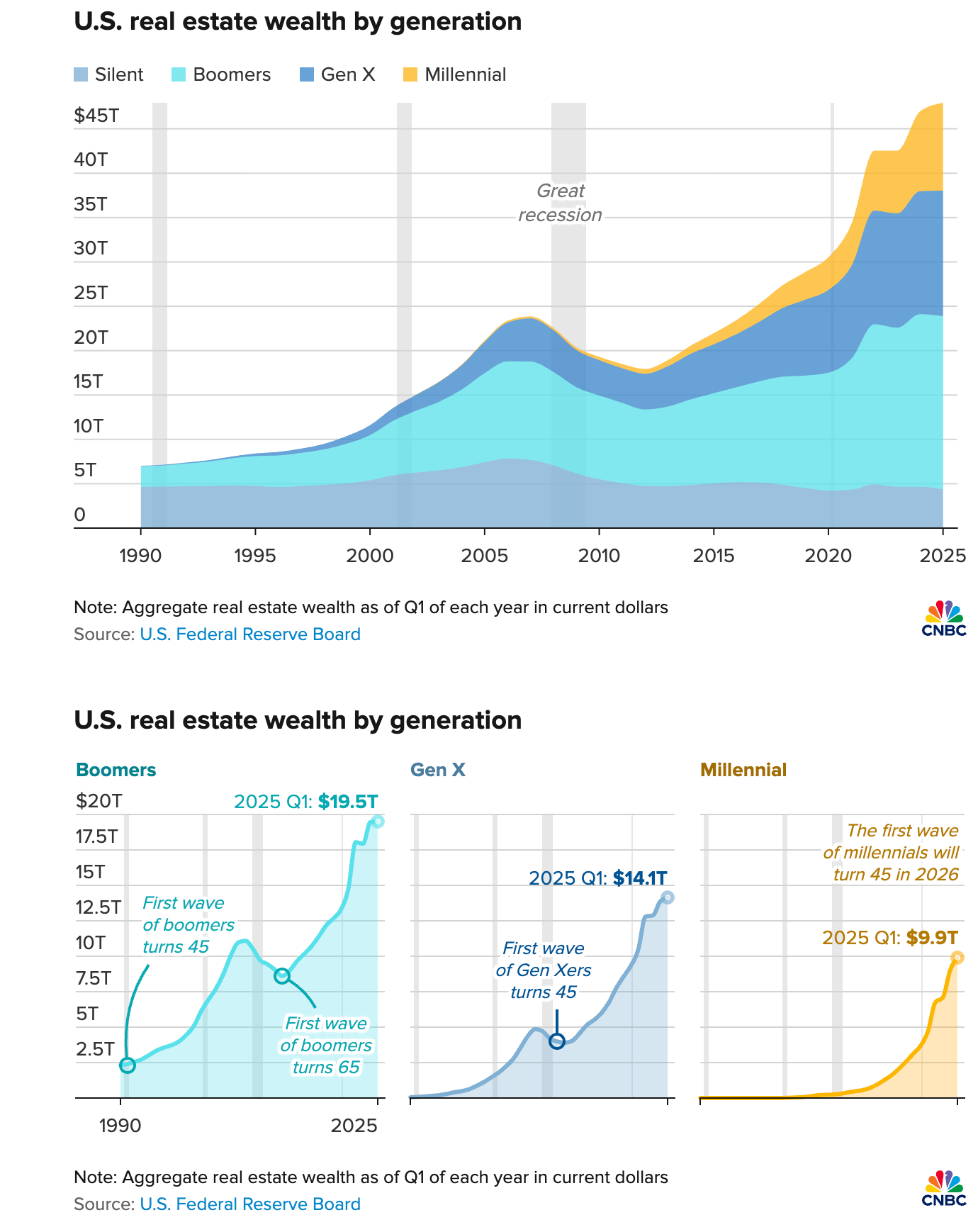

Boomers built their wealth in this asset during conditions that no longer exist. They bought when price-to-income ratios were between 2 and 3.5. They paid off their mortgages over decades of real wage growth. By 2025 Q1, boomer real estate holdings had reached $19.5 trillion, up from a fraction of that in 1990.

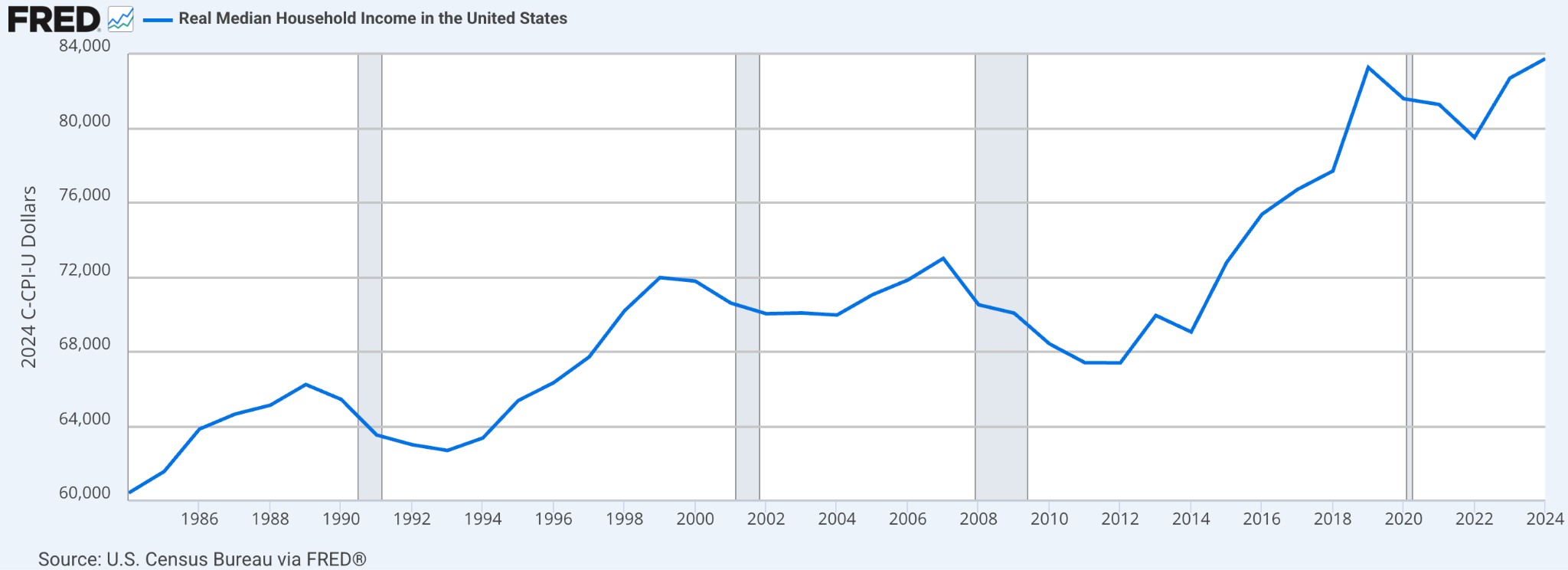

The millennial who enters the market today faces price-to-income ratios that have more than doubled since their parents bought. They arrive carrying student debt their parents did not have. They face mortgage rates that make monthly payments on a median-priced home nearly unmanageable on a median income. The down payment alone, on a home that keeps appreciating faster than savings can accumulate, has become its own kind of trap.

The result is a generational split that stopped being cyclical a long time ago. The generation that could afford to buy did. The generation that could not is about to inherit what the first generation built.

Real estate is among the most illiquid assets a person can hold.

You cannot sell 10% of a house when you need cash. You cannot move it when your job changes. You cannot divide it cleanly among four siblings without triggering a legal process that can take 18 months and drain money the estate may not have. Inheriting a million-dollar home in a city you cannot afford to live in is not good news. It is a decision. Sell it, keep it and carry the costs, rent it out and become a landlord, or spend years negotiating with your siblings about which of those to choose.

Boomers now hold ~40% of US housing wealth.

Sixty-one percent say they will never sell, and when you understand the incentive structure, I don’t think it’s stubbornness. Selling triggers capital gains on decades of appreciation. It resets a 3% mortgage to a 7% one. In California, it can increase a property tax bill tenfold overnight. And there is nowhere affordable to downsize into anyway.

So they stay. The homes do not circulate. Younger buyers remain locked out, waiting for an inheritance that, in many cities, has become the only realistic path to ownership. When the inheritance finally arrives, the illiquidity problem transfers instead of dissolving.

Nansen co-founder Alex Svanevik described what comes next as a tsunami. Speaking in January 2026, he said that something like $100 trillion is going to be inherited over the next 20 years, and that the forces driving that capital toward crypto are structural, not speculative. His estimate is that if even 3% of those inherited assets flow into crypto, the market could double from its current size.

The 3% figure sounds modest? But consider who is doing the inheriting. Gen Z is five times more trusting of crypto than boomers, according to a recent OKX survey. Millennials already hold more digital assets than their parents do. We don’t need to convince them crypto is real. They grew up using it the way earlier generations used savings accounts. What they need is for the wealth they are inheriting to meet them where they already are.

That is the gap. Tokenisation is what closes that gap.

Real-world asset tokenisation means representing ownership of a physical asset on a blockchain. Once that happens, ownership can be divided, transferred without a broker, held in a wallet, used as collateral, or traded without requiring unanimous agreement from everyone who has a stake in it. The friction becomes manageable in ways it currently is not.

What tokenisation offers for inherited real estate, specifically, is a solution to four problems that currently have no good answers.

Liquidity: A tokenised property can be partially sold. An heir who needs $50,000 and holds a $500,000 home can sell 10% of their ownership rather than the whole house or nothing. It also makes borrowing against the asset far easier because the underlying real estate can be bought and sold fluidly, lenders can actually underwrite it. Taking a loan backed by the property becomes significantly simpler for the same reason.

Division: When four siblings inherit a property, tokenisation allows each to hold their exact share digitally, trade it, sell it, or hold it independently, without requiring unanimous agreement about what to do with the physical asset. The legal fights that currently consume inherited estates become substantially simpler when ownership is programmable.

Mobility: A tokenised property can sit in a portfolio alongside stocks, crypto, and other assets. It can be managed remotely, transferred across borders, and eventually used as collateral in DeFi protocols. The location-bound nature of real estate stops being a constraint on the heir’s financial flexibility.

Access: For the heir who cannot afford to buy property but stands to inherit it, tokenisation allows partial participation. For the younger sibling who gets a smaller inheritance, fractional ownership lets them hold a real asset rather than liquidating their share immediately.

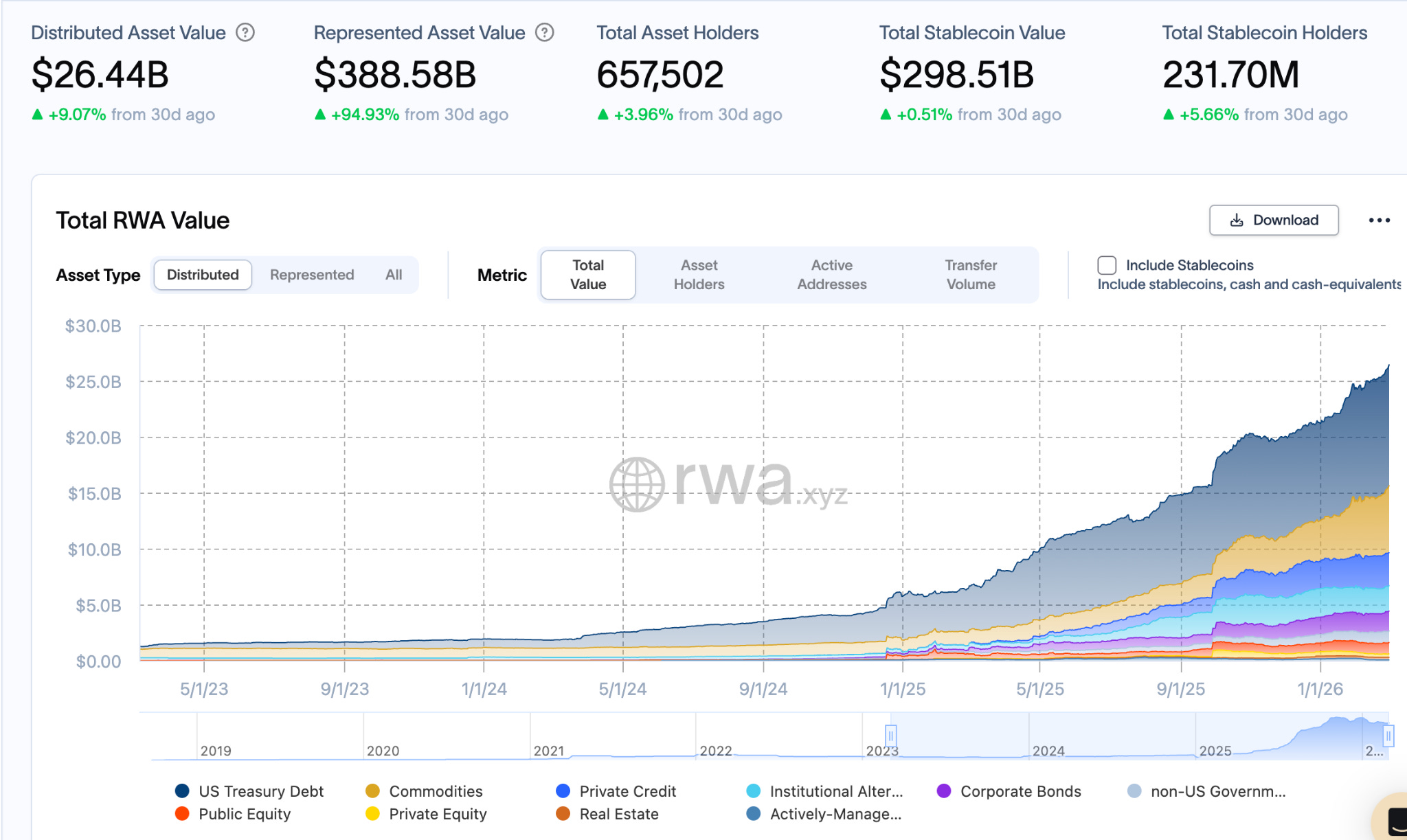

The market is already moving in this direction. Total tokenised real-world asset value has reached $26 billion in distributed assets and $388 billion in represented assets as of early 2026, growing sharply. Real estate is still a small slice of that, but the infrastructure being built, wallets, onchain settlement, programmable ownership, is functional in ways it was not even two years ago. Svanevik noted that the product Nansen has built today could not have existed two years ago because the underlying infrastructure was not ready. That has changed.

None of this means tokenisation solves the housing affordability crisis. Prices will not fall because ownership becomes more portable. The structural problems in the market, supply constraints, rate lock, the long decoupling of home prices from wages, remain exactly what they are. And we don’t know whether financialising the last illiquid asset most families own actually makes their lives better, or just makes their problems more tradeable.

What tokenisation addresses is a narrower and more immediate problem. It is about what happens when $25 trillion in property wealth changes hands between a generation that stored everything in real estate and a generation that thinks about wealth as something fluid, digital, and not necessarily tied to a physical address.

The existing toolkit for unlocking home equity is broken for most of the people who hold it. Cash-out refinancing requires giving up a 3% mortgage for a 7% one. HELOCs and home equity loans require income qualification that retirees often cannot meet. Reverse mortgages carry 30 years of stigma and create inheritance complications. Selling triggers the tax trap and the rate reset simultaneously. Every option costs something the holder cannot afford to lose.

The transfers are already happening, at roughly $1.5 trillion per year and accelerating. The first wave of millennials turns 45 in 2026. JP Morgan, BlackRock, and Franklin Templeton have all moved into tokenised assets in the past two years, building infrastructure for exactly this moment. Robinhood CEO Vlad Tenev wrote last year that this wealth transfer is happening alongside technological dislocations that will make the coming years critical.

The generation inheriting this wealth already thinks about financial assets as things that live in wallets rather than filing cabinets. The friction is in working with the paper-based, broker-mediated system that currently governs how property moves between people.

Every generation builds wealth in the language it knows. The next one has to translate it.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.