Hello,

Going public for a company is one of capitalism’s great rituals. A company spends weeks on the road (quite literally) parading its pitch deck before fund managers, hoping they buy in. Bankers play the role of the jury, weigh the demand, determine what they believe is the value of the shares the company is offering, and allocate the shares. Then a bell rings on one fine morning, and voila - the private company is now public. The buyers and sellers then engage in a battle of orders in public markets, leading to price discovery over the next few hours or days.

These rituals involving the roadshow, book and bell exist because nobody could see inside a private company and had to wait for the bankers to set a price. Every company had to go through it all and arrive on the other side.

But SpaceX, the latest to go public in the US stock market, didn’t quite walk this journey. Elon Musk named his price even before the roadshow or the bankers calculated it.

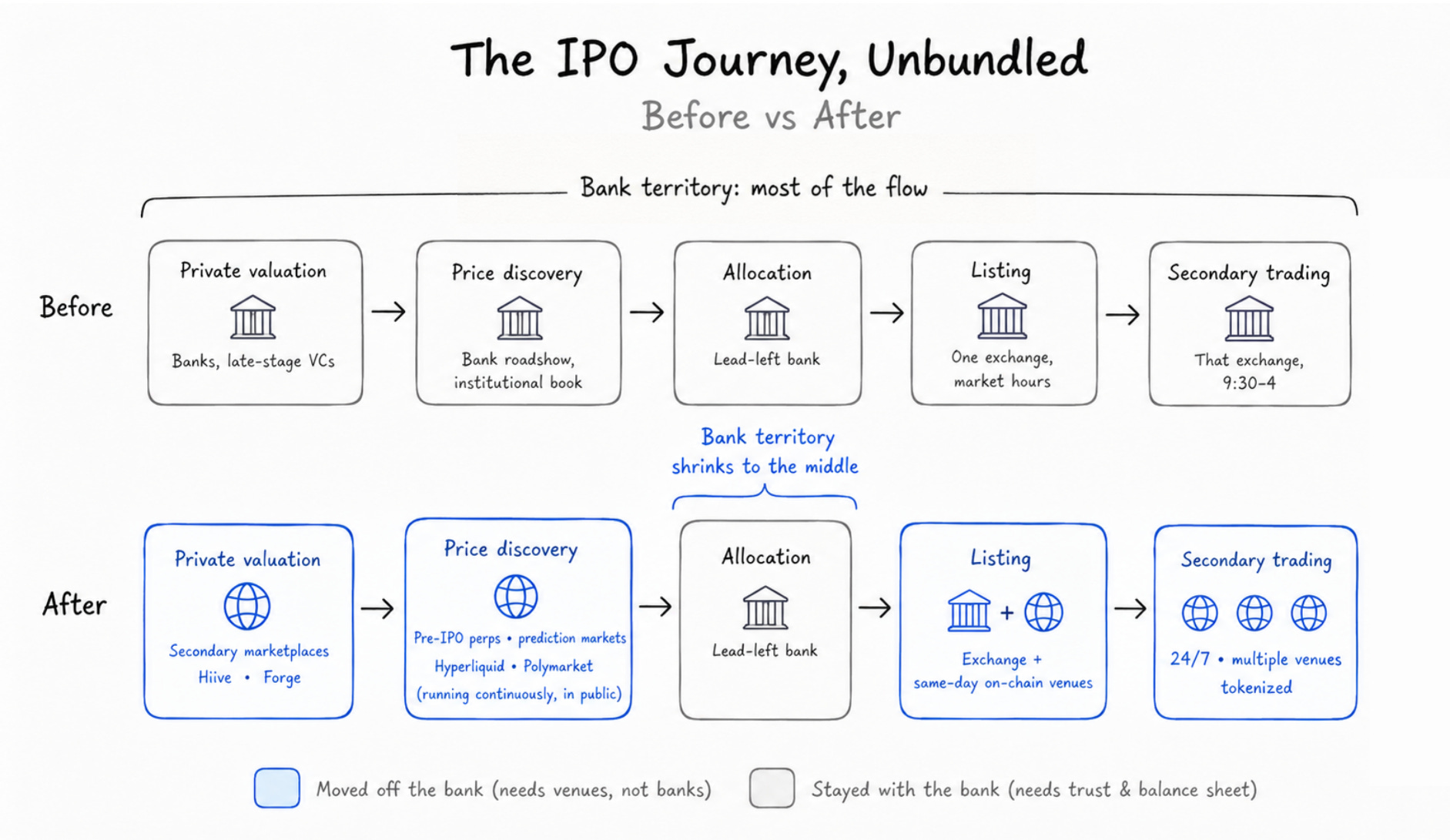

An IPO has historically bundled three things as a job for bankers and paid them a fee for doing so. They figured out the price, found the buyers, and delivered the shares. With SpaceX, all three were unbundled and functioned separately. The public had already priced the company, and buyers had already lined up before it went public.

In today’s piece, I explain how SpaceX is changing the way companies go public and the role banks play in the new journey.

Onto the story,

Prathik

The Bankers’ Fee

Bankers charge the company a fee to execute the IPO process. For most of the past century, that fee was calculated as a spread on what the company received from its investors.

As part of the execution, the banks ran a roadshow, collected soft orders from institutions and retailers across a range of price bands, and settled on a price that the market would deem right. It then had to ensure delivery of shares. In a standard firm-commitment deal, the underwriting banks buy the entire offering and resell it to those who applied for the offering.

These three functions of price discovery, distribution and allocation were fused together because it couldn’t have been done differently for years. Banks were the only institution that saw the full picture, which made them the best party to estimate demand. They had access to the company’s financials and plans ahead, which let them price its shares more accurately. Banks’ diverse clientele and cross-sector relationships enabled them to place the stock in the hands of influential institutions and retail investors. Banks’ robust settlement systems guaranteed that the shares actually moved.

So the company going public had no choice but to buy them as a set and pay the bank for the bundled services.

With an unbundled IPO, that chokepoint no longer exists. The demand is now visible to everyone in public through perp venues, prediction markets, and pre-IPO platforms, even before the bank begins work on the public offering. This lets the company negotiate its fee and choose the best venue for each service in the IPO journey.

For mid-sized American IPOs, that fee averages around 7% of the total deal value. Big deals pay less. In 2014, Alibaba’s $25 billion listing paid 1.2%. SpaceX paid only 0.67%. There could be multiple reasons for the largest IPO in history paying one of the smallest fees. The unbundling of the expectations from an underwriting bank must surely be one of them.

The Public Pricing

SpaceX went against conventional IPOs even before the roadshow began. Instead of banks testing a price range before arriving at the offer price, Elon Musk straightaway named one price, $135. Investors can either take it or leave it.

SpaceX could skip the banks for price setting because that had already been done for weeks before it went public.

Three public markets priced SpaceX differently. On pre-IPO secondary marketplaces like Hiive and Forge, where employees and early investors trade private shares, SpaceX’s share price hovered near $150, its opening price at debut.

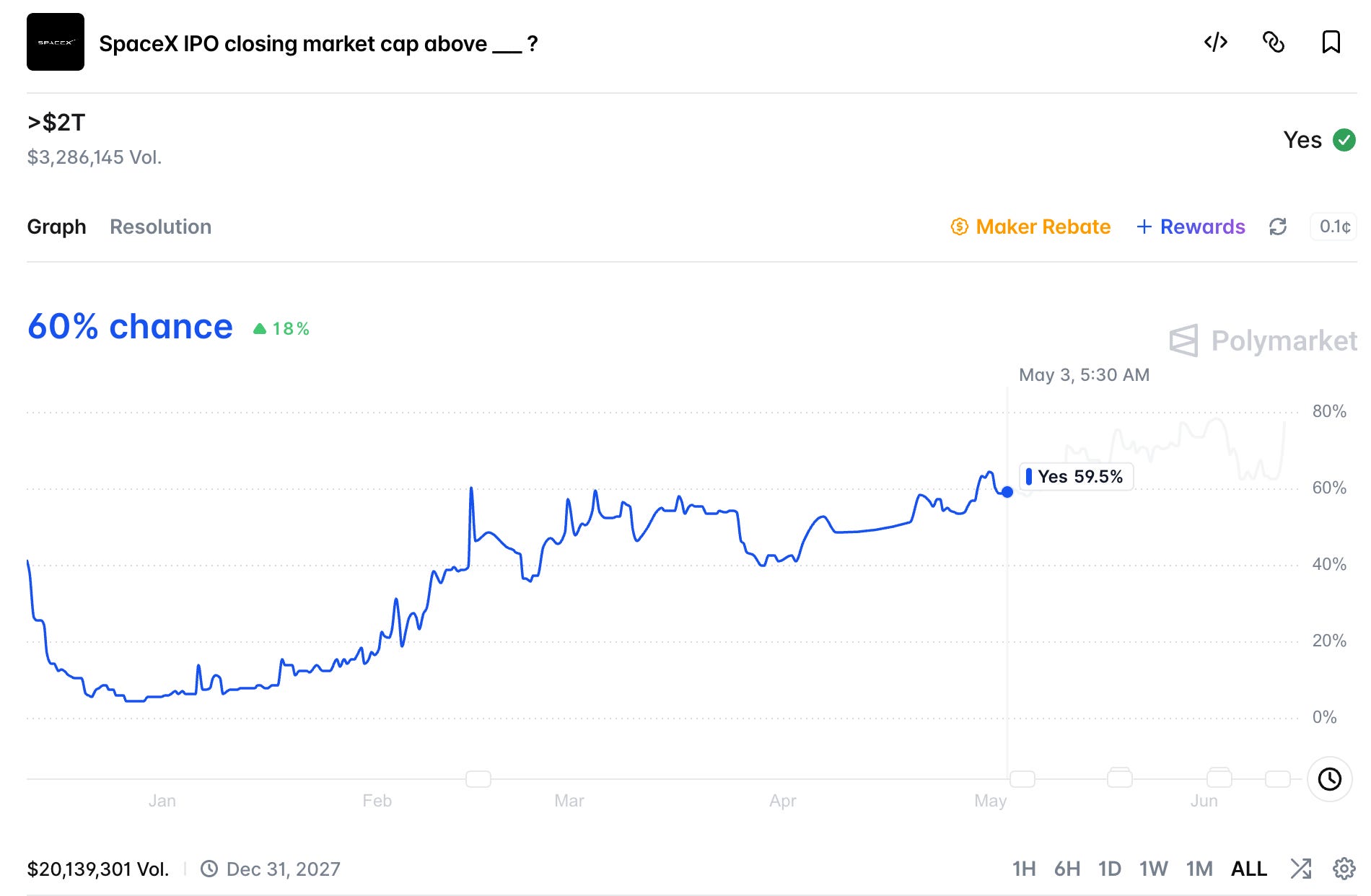

On Polymarket, the crowd was pricing in where the stock would close on its first day, with the highest cumulative betting volume implying a valuation above $2.0 trillion.

On Friday, June 12, SpaceX shares did close at ~$161 apiece, 20% above its offer price, with a valuation of $2.1 trillion.

On Hyperliquid, a perpetual futures contract on SpaceX traded continuously, around the clock, acting as a live public signal of how the market wanted to price its shares.

Until the public listing, these pre-IPO perpetuals have no underlying shares to anchor their price to. So, they act more like leveraged bets on how the market thinks the stock will be priced when it debuts.

Most of the open interest in Hyperliquid’s permissionless markets was tied to this one SpaceX contract. On debut morning, the perp contract on HIP-3 markets was trading around $174–185, a 30–35% premium to the offer price of $135. On its first day of trading on the stock market, SpaceX reached an intraday high of $176 per share.

The price of the perp contract also immediately corrected towards the opening price of $150 when the stock debuted on the bourses.

Possible coincidence? Well, it wasn’t the only time the unconventional pricing mechanisms got it right.

When chipmaker Cerebras went public weeks earlier, its pre-IPO perpetual on Hyperliquid landed within 1.3% of the eventual Nasdaq open, which then compressed to a near-zero spread once trading began. The venue predicted a company’s opening price before the company had a price.

This is how SpaceX skipped the banks for the first job in the IPO bundle - the price discovery.

The Delivery Problem

After banks help set the price for conventional IPOs, they help distribute the shares by finding buyers. We will get to this part later. Let’s jump to the third aspect of the bundled services the underwriting banks offer: allocating and delivering the shares.

On the listing day, SpaceX was trading at different venues and under different arrangements, contrary to how conventional IPO stock trades. A token on Solana issued by Backpack, a US-registered product from Kraken, a tracker from Ondo, and Hyperliquid’s synthetic perpetual all had SPCX as their underlying asset. Many centralised exchanges, like Bitget, Bybit and Binance, also allowed their users to apply for these IPOs.

On the day of listing, some of them delivered and others didn’t.

The products that held the asset directly, or sourced it through a registered broker-dealer, opened on time and tracked the stock. Backpack’s Solana token was backed 1:1 by real shares held at its broker-dealer arm. Kraken’s US product sourced stocks through Payward Securities. Ondo ran daily custody attestations against its tracker. Hyperliquid’s perp never needed a share in the first place, but its price corrected to track SPCX’s stock once SPCX went public.

Binance, Bybit and Bitget had run tokenised allocation campaigns, allowing users to subscribe to SpaceX, with xStocks (Kraken-owned tokenised stocks platform) promising to source the actual stock underlying those tokens. The shares were never allocated, and the exchanges refunded subscribers in full, with Binance alone returning roughly $557 million.

Was it a failure of blockchain? The other venues that held the asset honoured their agreement. So, the tokenised version of the stock itself wasn’t the problem. SpaceX was oversubscribed, with demand reaching 3.5 to 4 times the $75 billion on offer. It was just in case of centralised exchanges that were counting on a middleman to get shares allotted that the delivery failed. Eventually, the subscribers were compensated in full.

So, when the price discovery is commoditised and public, pricing is no longer the scarce and valuable thing in the IPO bundle. It comes down to proving whether you can deliver the shares.

This is not a new problem, though. Wall Street faced a similar problem about 60 years ago and built an institution to end it.

In the late 1960s, American trading volumes outran the paperwork. The back offices drowned in paperwork because the stock certificates were physical paper that had to be located, checked and hand-delivered for every trade. Trades failed constantly because the seller simply could not produce the certificate. The exchange closed every Wednesday just to dig out from the backlog. The industry came to a fix that involved avoiding paper movement.

In 1968, the Central Certificate Service was established (later reorganised into the Depository Trust Company in 1973) to hold certificates in a single vault and record ownership as book-entry entries. If everyone’s shares sat in the same trusted place, delivery would no longer be a question. The depository could guarantee that the seller had the share and the buyer received it.

This is the fundamental problem that custody infrastructure has to answer: Does the seller actually have the asset, and can they hand it over?

Tokenisation presents a similar problem because a token can be issued before the shares behind it ever reach the depository’s guarantee. When the claim is backed by real stock sitting at a broker-dealer, it inspires confidence in delivery. When the token is sold ahead of shares that were never sourced, the claim isn’t as strong. In 2026, it was a tokenised claim whose shares were never procured that became the problem. The difficult part of an IPO to crack will no longer be price discovery. It will be around proving that the underlying asset exists and can be transferred.

What’s Left for the Banks?

Let’s walk the IPO from start to finish and see what’s changed hands.

At the earliest stage, the private price discovery will no longer be the banks’ stronghold. It now happens continuously and in public, on secondary marketplaces, prediction markets and perpetual futures, for weeks or months before a listing. By the time a company like SpaceX decides a price, the market has already priced it using multiple tools.

Read: Pricing the Private

The listing itself is now contestable. SpaceX traded on Nasdaq and, the same morning, on a handful of on-chain venues. Secondary trading no longer stays within a single exchange, courtesy of blockchain-enabled 24/7 venues.

The answer to the delivery problem rests on who actually holds the asset. This, too, used to be the bankers’ monopoly, where they guaranteed delivery of assets by relying on the depository in which they held the shares. Now, anyone who can prove custody can stand in that position.

What still rests with the banks? The four things in the messy, middle phase.

First is the certification. The endorsement of a lead underwriting bank at the top of the prospectus vouches for the deal, telling cautious institutions this one is safe to buy. That endorsement is reputational, built over decades, and a token wrapper cannot issue it. Banks charge a fee for this reputational validation. Goldman Sachs and Morgan Stanley each walked away with $100 million from the $500 million in total fees SpaceX paid the bankers. This was despite the fact that these banks played little role in price discovery.

Second is the distribution authority. The lead bank still allocates the vast majority of shares at its own discretion, deciding who gets in and who is left out.

Next is the risk absorption. In a firm-commitment deal, the kind SpaceX had signed, the banks contractually buy the entire offering and resell it. If demand collapses and the book goes unfilled, the banks, and not SpaceX, would have to hold the unsold stock. No on-chain venue will step up to bear that kind of risk.

Lastly, the stabilisation. In the fragile initial days of trading, if a stock is wobbling, the lead bank buys back shares it had deliberately oversold at the offering (also called the “greenshoe” mechanism) to prevent wild price swings. In SpaceX’s case, it was Morgan Stanley supporting SpaceX after the bell. It is a job that needs a balance sheet and a market-making desk, and it is the banks doing that, for now.

Everything else in the IPO journey is being picked up by markets that run cheaper, for longer hours and in public.

Blockchain-enabled pricing venues have proven effective for pricing companies planning to go public. These venues are always on and offer a market for continuously pricing the stock, better than any bank does. It was evident in how SpaceX’s book was oversubscribed multiple times, and the stock closed its first day up about 19%, close to a textbook-perfect example of an IPO pop.

The old IPO model has been unbundled, and each part is being taken over by the venue that executes it most efficiently. We see this happen across every market - financial or otherwise. In Pricing the Private, we argued that markets no longer wait to price private companies. Banks that guarded and held a monopoly over pricing a company and delivering its shares will no longer be paid for these services in the new IPO model.

So, will the bankers’ revenue from IPOs all but vanish? Not really. SpaceX paid 0.67%, but that spread alone was not what the bankers focused on.

Consider the first-day pop. SpaceX closed about 19%, which on a $75 billion deal amounts to roughly $14 billion in unrealised gains in a single session. Some of the lucky investors who book part of these profits are most likely clients of the underwriting banks that made the allocation possible. Although banks can’t allocate shares to their own books, they still receive inflated trading commissions from their clients, who thank banks for continued access to favourable IPO allocations.

This is why a 0.67% fee still drew almost two dozen banks into a fight for position. The spread is no longer the main deal. The allocation power, the soft dollars banks get to make on their positions, and the wealth tail are what the banks will be in it for.

So the bank’s economics will migrate up the prestige ladder, from a commodity (pricing, which anyone can now do) toward a scarcity (access, which some banks still control).

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.