Tokenisation is Living its Pre-API Moment 🔗

Wrappers help build trust to introduce on-chain native assets

Hello

By 2015, European banks had been online for nearly two decades. You could check your balance, transfer money, and pay bills, all from your phone. Although the infrastructure worked, every financial service still had to run through the bank as a gatekeeper. Nothing else could plug into your money without the bank’s permission.

Then PSD2 forced banks to open their plumbing via APIs. Stripe built its European Treasury on open banking, Plaid connected hundreds of millions of accounts, and Shopify started underwriting loans using transaction data. By 2030, embedded finance is expected to exceed €100 billion in annual revenue across Europe alone.

But for the industry to arrive there, it had to pass through 15 years of online banking, which had already taught hundreds of millions of people that digital financial infrastructure was reliable. The API layer didn’t conjure trust from nothing. It was built on the trust that had accumulated over the years.

This is the story of how trust evolves around any new technology. Tokenisation is living through the same moment right now.

Last week, Pantera Capital published a report on the state of tokenisation in 2026.

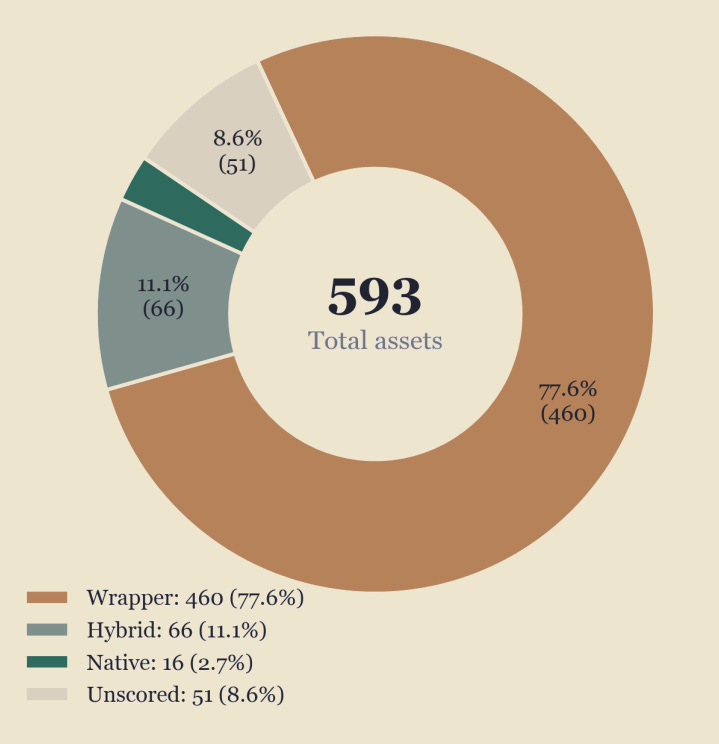

In this report, they scored 542 out of the 593 live tokenised assets across three dimensions of on-chain maturity — issuance and redemption, transferability and settlement, composability — and arrived at an average Tokenisation Progress Index (TPI) of 2.04 out of 5. About 77% of tokenised assets are still digital receipts of the original assets off-chain. In these cases, the off-chain ledger remains authoritative, and the token adds just a data layer on top of it.

It’s tempting to read these scores as a poor grade. Crypto natives might call it a stalled industry. But no technology can build sustained, mass adoption by skipping the trust-building phase. Here is why.

Onto the story,

Prathik

Wrapper: The First Stop

The Pantera report found that 460 out of 593 (77%) tracked assets fell into the ‘Wrapper’ bucket, while only 16 were natively launched, managed, and recorded on-chain. Tokenised wrappers are assets whose minting and redemption still occur off-chain through a centralised issuer. About 66 fell into the hybrid category.

Pantera calls the current state the “newspaper-on-a-website phase.” The phase isn’t a failure of the industry to mature quickly. It’s the first stop that tests the thesis that on-chain representations of existing traditional assets can offer any benefits.

Let’s rewind two decades. Imagine reading about online commerce for the first time. You scroll, you click, and a stranger ships you a box. The thought felt magical back then. You’d order once to experience what it feels like, perhaps. But you would pay before the box arrived?

The early e-commerce era was heavy on cash-on-delivery because customers were slowly warming up to the idea of buying something without first touching and feeling it. Users preferred to pay on delivery because it let them cross the first hurdle of believing that something like e-commerce was even possible. Technology to facilitate online transactions wasn’t the problem. SWIFT-enabled interbank transfers have been around since the early 1970s, and consumer payments became possible via platforms like CyberCash and PayPal in the 1990s and early 2000s.

Yet, the switch to paying online came much later.

Similarly, the first drive toward tokenisation is setting the stage for what comes next: programmable compliance, autonomous collateral management and real-time yield optimisation. Then follow the financial building blocks that separate ownership, cash flow, and risk, and recompose them.

A tokenised version of an off-chain asset shows that the new tech can do faster settlement, cheaper transfers and cleaner ledgers of record. Each time a tokenised Treasury or money market fund settles faster than its off-chain equivalent, it builds confidence among its customers.

The data in the report also backs this idea.

Of Pantera’s three Tokenisation Progress Index (TPI) criteria, the one that measures transferability and settlement scores the highest at 2.29. The fact that 205 assets have reached a score of 3 on this dimension indicates that the industry is leaning toward using blockchains as the authoritative management and settlement layer. By contrast, the TPI of the issuance and redemption layer lags at 1.82. Over 91% of assets still rely on admin-gated minting and custodian-mediated exits.

These scores indicate that the market is more comfortable with reliably moving assets on-chain before it can trust the chain to autonomously originate and redeem assets.

This maturity curve is inevitable for any technology. That’s because even the greatest technology cannot magically generate demand for that asset.

Demand is for the Asset, Not the Rails

Introducing a native on-chain asset will not automatically attract capital. The data from the report reinforces this idea.

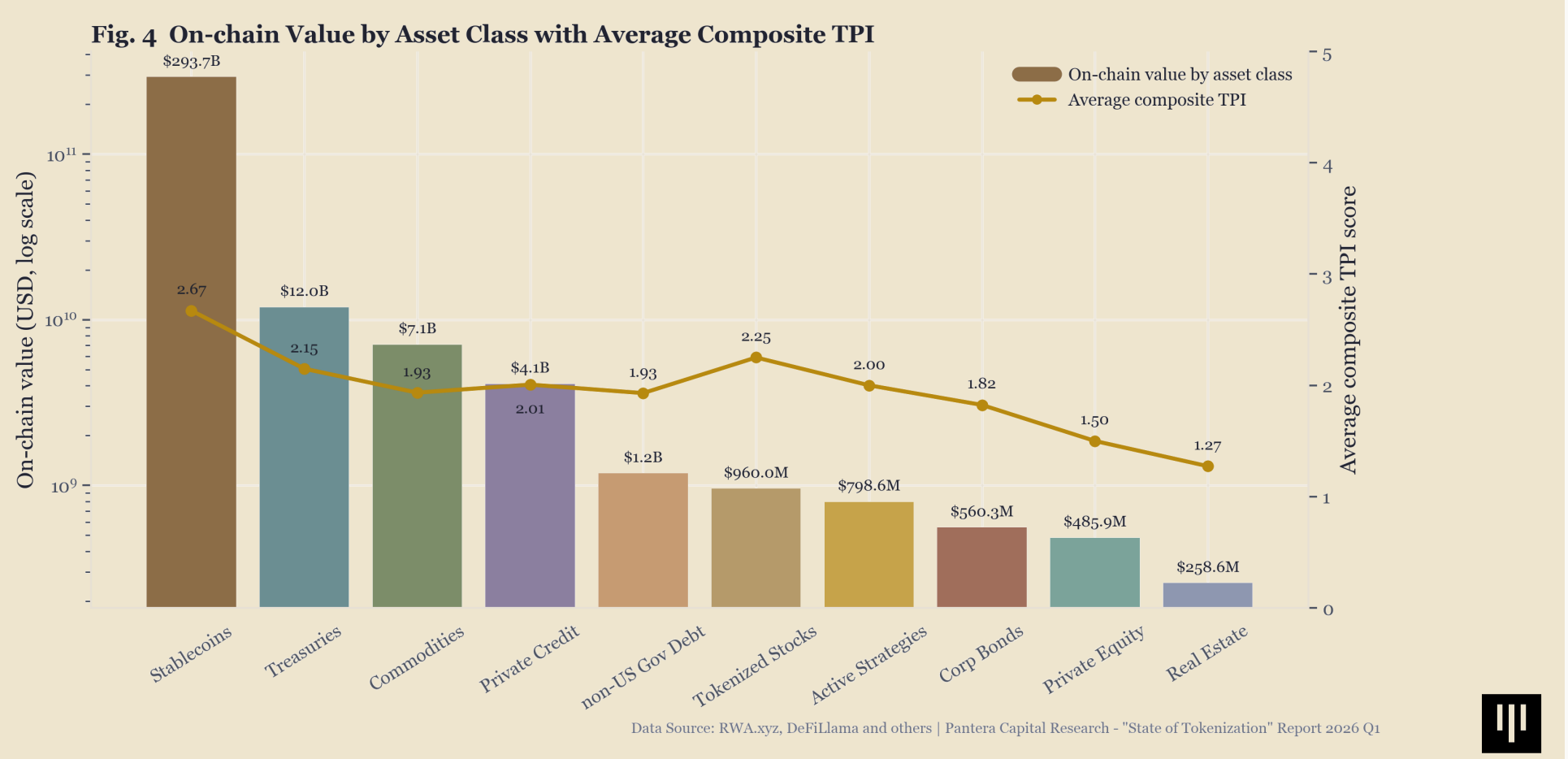

Stablecoins account for 91.6% of the $320 billion tokenised market. US Treasuries add another $12 billion. Together, that’s roughly 95% of the total. Everything else, including private equity, real estate, and corporate bonds, accounts for a negligible 5% today.

This shows that the market isn’t following the most interesting native tokenised asset. The demand follows for those assets that people have wanted to invest in all along. People don’t care whether something comes in a wrapper or a native on-chain treasury fund. As long as the new infrastructure offers them an incrementally better experience of holding, transferring, and recording the asset, they will prefer it to the old infrastructure.

We have seen this across multiple primitives in the crypto ecosystem.

Hyperliquid’s HIP-3, launched in late 2025, enabled permissionless perpetual futures markets for real-world assets, including equities, commodities, indices, and FX. These markets have recorded over $240 billion in trading volume since launch. In January 2026, Hyperliquid’s HIP-3 perps market on Silver captured 2% of the global trading volume for the metal in just one month of its launch.

Read: A Sliver of TradFi

All this demand didn’t materialise because Hyperliquid invented a new format. The traders who chose Hyperliquid already wanted exposure to Tesla, silver, gold, and the S&P 500. The format that Hyperliquid offered, which is a 24/7, permissionless, non-custodial venue, simply minimised the friction and time between an event happening and a trader expressing a view on it. The underlying assets were popular even outside Hyperliquid. The technology succeeded because the platform amplified access.

The same dynamic is playing out inside tokenisation.

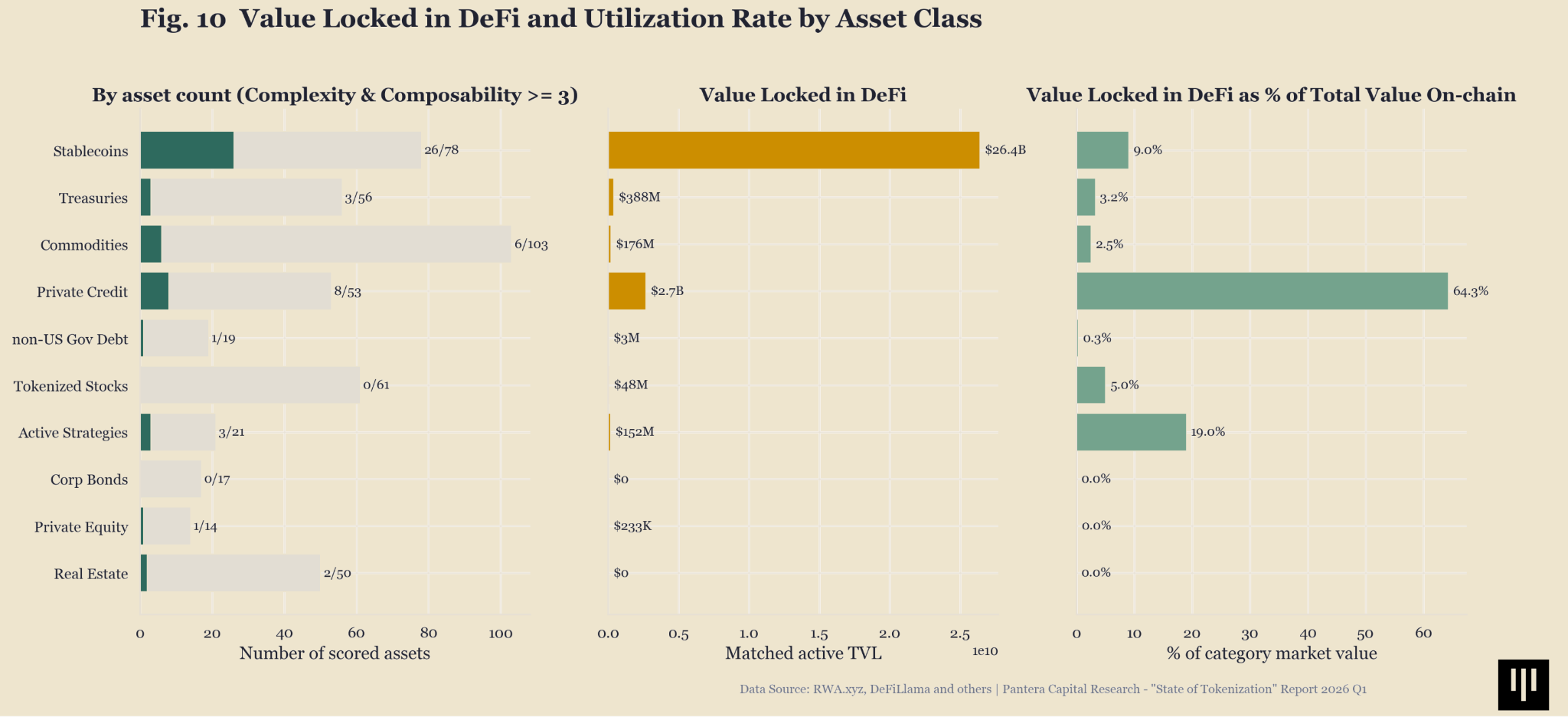

At 64%, Private Credit accounts for the highest share of its supply actively deployed in DeFi protocols. That’s far more than Stablecoins at 9% and Treasuries at 3.2%. The demand isn’t specifically for “tokenised” private credit.

People who deploy their funds into DeFi protocols via tokenised private credit do so because these wrappers offer them yield denominated in stablecoins. The underlying appetite remains for non-crypto yield. They don’t care whether the underlying rail is merely a wrapper for an existing private credit product or a native on-chain one.

Even the surge in commodities reinforces this idea.

Native on-chain products around tokenised commodities have grown fivefold from $1 billion in January 2025 to $5 billion today. That’s not because these rails offered something different. The jump tracks gold’s 65% rally in 2025, its sharpest annual gain since 1979. Tokenised gold products gained value largely because gold gained value. The blockchain just facilitated better settlement, transfer, and ownership of the asset.

If the underlying asset is compelling, tokenisation can make it more accessible, cheaper to settle, and easier to move. If the underlying isn’t that exciting, no amount of on-chain composability can fix that.

Where does that leave the industry?

The Pre-API Moment

I find striking parallels between the PSD2 moment and the journey of tokenisation.

Europe’s regulatory breakthrough, passed in 2015, took effect in 2018, and produced scaled native products like Stripe Financial Connections and embedded lending by 2020–2023. It took roughly five to eight years for native products to thrive on the underlying open infrastructure.

Tokenisation’s regulatory breakthrough moment began to take shape in 2024, and it’s arriving in parts across jurisdictions. MiCA took full effect in December 2024, with 102 crypto-asset service providers authorised across Europe by year-end 2025. The GENIUS Act was signed in July 2025, the first federal US legislation for digital assets. A couple of weeks later, the SEC launched Project Crypto, with Chairman Atkins acknowledging that firms from Wall Street to Silicon Valley were lining up to tokenise.

If the embedded finance timeline holds, we should expect native on-chain products to emerge in the next 3-4 years. They may not be everywhere and for every asset class. But in the pockets where the wrapper phase has already built enough trust and where the underlying demand already exists, we will see the change coming sooner than later.

Private credit is the clearest candidate. Two out of every three dollars of on-chain private credit are already active in DeFi. The composability that makes private credit products like Maple’s syrupUSDC useful in DeFi was built on top of a lending infrastructure that first had to prove it could reliably underwrite, disburse, and collect on-chain. The native features will arrive as extensions of trust already earned.

The $320 billion tokenisation market scored 2.04 out of 5. That still reads like a poor grade. But that’s where a new industry starts to build trust and position itself to grow through faster settlements, cheaper bookkeeping, and more transparent ledgers, until the demand for native on-chain assets catches up.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.

Great perspective - tokenisation still feels early, but the infrastructure being built now could define the future of financial markets. Timely and well explained.