Hello,

In 1688, a coffeehouse on Tower Street in London became one of the most important rooms in global commerce. Ship captains, owners, and merchants would walk into Edward Lloyd’s cafe carrying a slip of paper with a description of the cargo, the route, and the vessel. They needed someone to bear the risk of the voyage. Individuals willing to accept a share of that risk would write their names underneath the terms. That gave birth to the word “underwriting”.

The most powerful person in the room was the one who set the terms on that slip, including the premium to charge, the risk to absorb, and which voyages to back. No vessel sailed until this person priced the risk of its first journey.

This arrangement helped the coffee house evolve from a social gathering place to Lloyd’s of London, one of the world’s largest insurance markets, over the past three centuries. Interesting, right? What I found even more interesting when I started reading this story was an insight that remains relevant today. It’s the realisation that every asset, venture, or anything tradable needs a moment where someone decides “this is worth backing, at this price, on these terms.”

We saw this pattern repeat each time a new asset class emerged.

About two centuries after Edward’s coffeehouse, we saw J. Pierpont Morgan underwrite the terms for publicly funded railroad projects in the U.S. by issuing stock in companies such as the New York Central Railroad. This established J.P. Morgan’s reputation as the mobiliser of capital and an expert railroad financier.

His underwriting set the terms, chose the investors and captured the spread between the price paid to the issuer and the price offered to the public. When Morgan refused to underwrite a venture, it didn’t get built.

The modern IPO is the digitised version of the same mechanics. A handful of banks underwrite a company’s initial public offering (IPO), gauge demand from preferred clients, set the offer price, and allocate shares. The debut day “pop”, where shares jump by 20-30%, is more than merely a market phenomenon. It reflects the underwriter’s margin.

The one complaint investors have to date across four centuries is that insiders get the best allocation, the first price rarely reflects true demand, and everyone else arrives after the spread has already been captured.

Last week, James Evans posted the HIP-6 proposal for token launch auctions on Hyperliquid, which addresses part of this complaint. In his post on X, James disclosed that he held $HYPE in his portfolio and that he works with Reciprocal Ventures, an early-stage crypto venture capital firm.

In today’s deep dive, I will evaluate HIP-6 and other on-chain platforms to assess if they can address the legacy problem in capital formation.

What’s Broken

The book-building process that dominates traditional capital formation is a black box by design. Banks solicit demand from institutional clients behind closed doors, set prices based on conversations the retail market is never privy to, and allocate shares to “random” accounts. The issuer gets a price, and the public gets whatever is left.

Consider two instances.

During Facebook’s (now Meta) 2021 IPO, lead underwriter Morgan Stanley cut their revenue forecasts during an investor roadshow. The negative news was available immediately to major institutional clients as part of analyst notes, while retail investors bought in blind. The stock dropped by approximately 50% in three months. Retail got the worst of both worlds: full allocation at inflated prices and no access to the information insiders had.

There’s a more recent precedent in Rivian’s 2021 public listing debut as an electric vehicle maker. Its IPO, which was priced at $78, popped to $179 on day one. Institutional clients who received allocations from Goldman and JPMorgan captured the spread. Retail bought at the open. Its share price dropped about 40% in 10 days. Investors then filed a lawsuit alleging that Rivian had concealed that its vehicles were priced below their material costs. The company eventually agreed to pay $250 million in settlement, while maintaining that it was not an admission of fault. Today, its share price hovers below $16 each.

This modus operandi has been normalised into a business model to the point that an average investor doesn’t even get a whiff of what’s wrong with it.

Beyond allocation, the infrastructure is slow and siloed. An IPO takes four to six months from filing to first trade. Settlement takes a full business day. The asset can’t be used as collateral until it clears. Market makers operate under separate agreements, often with guaranteed spreads. This entire apparatus is also jurisdictionally locked. So, a retail investor in Mumbai (India) cannot participate in a New York IPO on equal terms even if they are willing to bear the same risk.

The underwriter’s power comes precisely from these frictions. Inefficiencies such as opaque pricing, delayed settlement, and gatekeeping in access are exploited and treated as a moat by them.

What Changes with On-Chain Underwriting?

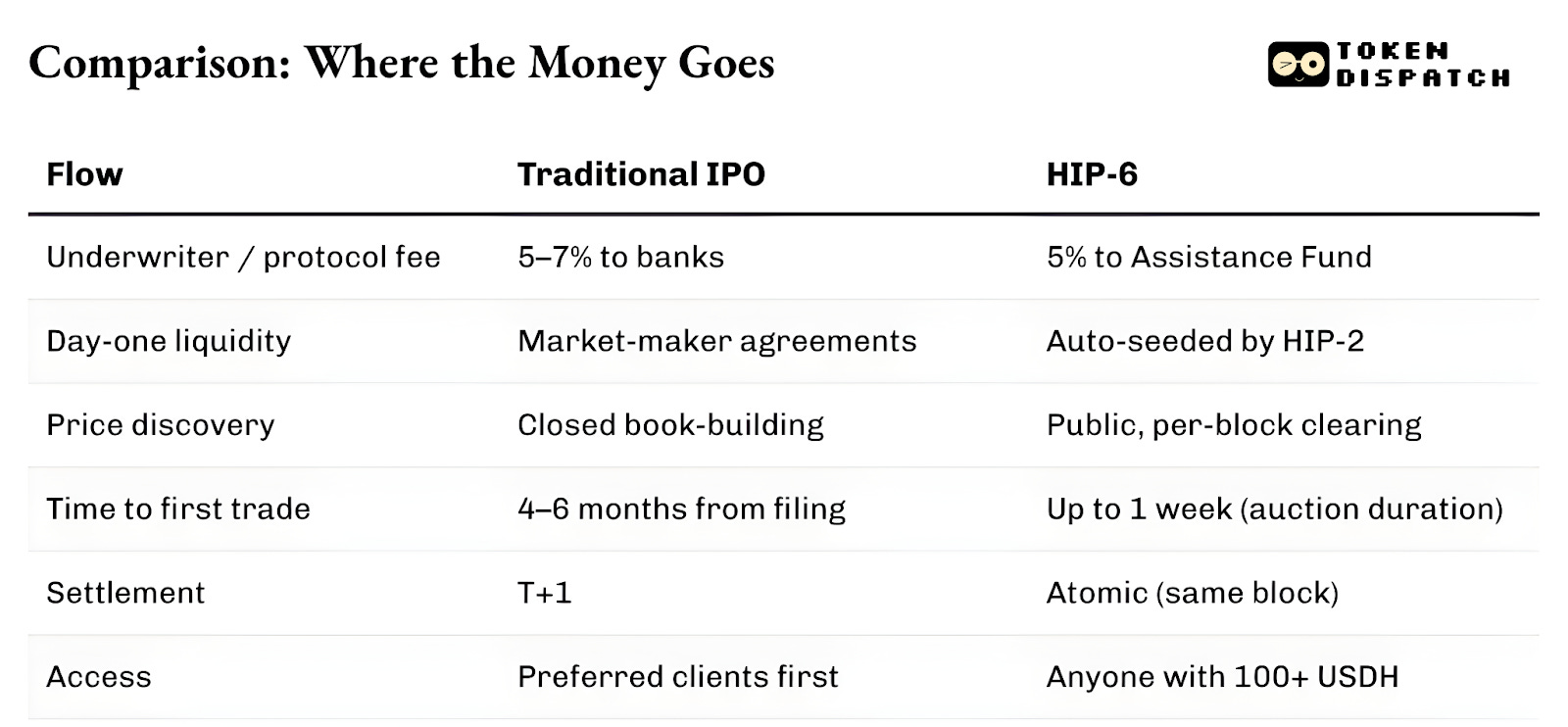

The underwriting process is structurally different, with fewer intermediaries on-chain. A bonding curve or a continuous clearing auction (CCA) publishes every bid in real time. On-chain, liquidity is programmatic from block one. It is coded into the launch mechanism itself through computation rather than negotiation. An asset can exist, be traded, and be used as collateral within the same block. No need to wait for T+1 or the clearing cycle.

Access gatekeeping persists, but along a different tangent.

A pump.fun launch is open to anyone with some SOL in their wallets. An Echo sale is gated by KYC, but is accessible across jurisdictions. Hyperliquid’s HIP-6 has set a 100-USDH minimum economic filter, but doesn’t limit people on an accreditation basis. All these systems avoid a “preferred client” allocation model that most traditional book-building processes follow.

The biggest differentiator between the two forms of capital formation is that on-chain underwriting treats every token launch as a buy order for the ecosystem’s native token, either SOL, USDC, USDH, or something else. Traditional underwriting doesn’t generate captive demand for anything except the underwriter’s fee.

This difference is more consequential than you might think.

On March 20, 2025, pump.fun - Solana’s dominant token launchpad - launched PumpSwap, its own automated market maker (AMM). Until that day, every token that graduated from pump.fun’s bonding curve was automatically routed to Raydium, Solana’s largest decentralised exchange. That graduation flow had become one of Raydium’s most significant revenue sources. Overnight, the pipeline was severed.

Read: Solana Showdown: pump.fun Vs Raydium

Raydium lost an estimated 35-40% of its AMM revenue. Its token, RAY, dropped by 30%. Raydium did not sit quietly. It hit back instantly by shipping LaunchLab, its own token issuance product, within 48 hours. The price of RAY peaked, doubling in six months, before collapsing to a two-year low. Today, it’s down almost 70% since pump.fun launched its own AMM.

The lesson was that whoever controlled where a token was born controlled the downstream fee revenue. Issuance meant order flow.

Two Lanes of Token Birth

What’s emerged since is a landscape split into two divergent lanes.

One is market formation, where a tradable chart is manufactured at internet speed. Pump.fun is the best example, with its bonding curve, $69,000 graduation threshold, and automatic liquidity seeding via PumpSwap. It has generated almost $1.5 billion in cumulative fee income, launched over 16.8 million tokens and allocated over 98% of revenue to buy back its PUMP token, offsetting more than 27% of the circulating supply.

The other lane is capital formation, with structured distribution into real users with compliance guardrails in place. Coinbase acquired Echo for $375 million in October 2025 and added a KYC-gated token sales platform with time-weighted deposit vaults to its product lineup. Echo’s Sonar product is at the opposite end of the spectrum from pump.fun, with a regulated, identity-verified, lead investor-curated approach.

The gap in Coinbase’s stack is liquidity at launch. Echo handles distribution but doesn’t auto-seed a trading market.

Where the Two Lanes Meet

The HIP-6 proposal is the latest attempt to merge the two lanes into a single protocol-level primitive.

The proposed mechanism is a continuous clearing auction (CCA) embedded in HyperCore’s consensus layer. At every block, the system computes a clearing price from all active bids using a budget-spread-over-remaining-blocks model.

This model is not entirely new. The HIP-6 proposal explicitly adapts Uniswap’s CCA, which launched in November 2025 and was first used by Aztec Network to raise $60 million from over 17,000 bidders, with no detected instances of sniping or automated manipulation.

The two implementations share the same core DNA. They both break down a large auction into thousands of sequential per-block mini-auctions, release tokens gradually, compute a uniform clearing price at each block, make bids non-withdrawable while in range to prevent coordinated price swings, and automatically seed liquidity at settlement.

This design solves the same legacy problems.

Fixed price sales force investors to guess the correct opening price. Capped pro-rata sales create oversubscription spirals. Dutch auctions make room for timing games that favour professionals. CCA eliminates all three. In CCA, the final seed price is derived from a volume-weighted average over the auction’s closing window, which is an anti-manipulation measure that makes price sniping structurally expensive.

Where Hyperliquid and Uniswap diverge is in their settlement architectures.

HIP-6 will run inside HyperCore’s consensus layer itself. The auction logic executes within the block transition function and not as an external contract. Clearing will happen at the same level as trade matching.

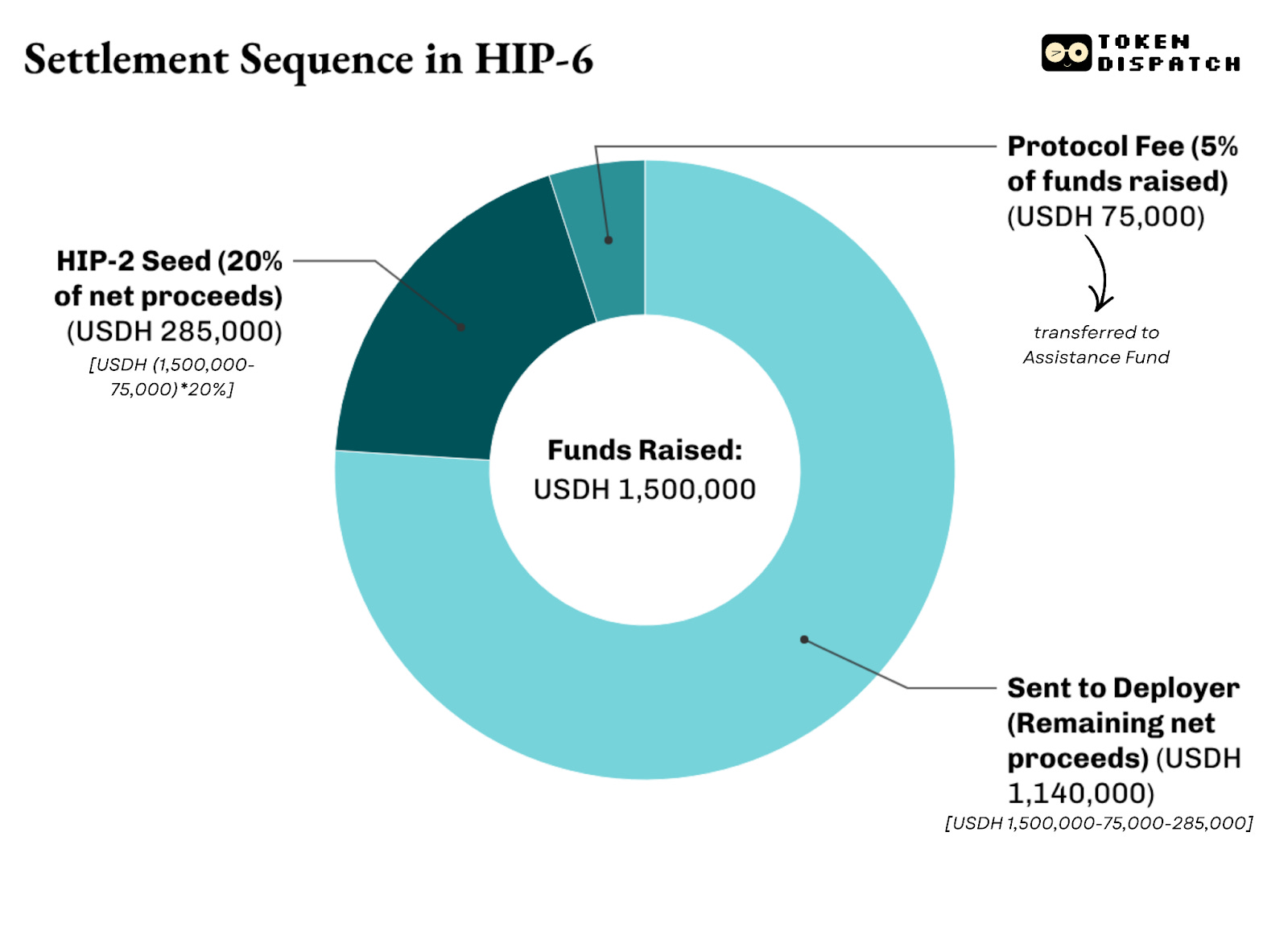

Settlement will be multi-tiered. The proposal states that a 500 basis-point (bps) protocol fee will be applied to the total funds raised and transferred to the Assistance Fund, through which Hyperliquid funds all its $HYPE buybacks. Out of the net proceeds (after deducting the protocol fee), 2,000-10,000 bps (20-100%) will be used to seed a HIP-2 market at the derived price. Then, any remaining funds will go to the deployer.

For example, a $PROJ token auction on HIP-6 raised 1.5 million USDH, with a total supply of 10 million tokens and a 20% HIP-2 seed. Here’s how the settlement would be done:

This is what separates HIP-6 from Uniswap.

Uniswap built CCA as a token-launch tool that feeds into its existing AMM pool. With HIP-6, Hyperliquid will become a full-stack primitive that lets stakeholders raise capital, discover price, seed two-sided liquidity, and begin trading on a central limit order book (CLOB).

What’s more? It will all be denominated in an asset the protocol wants you to hold: USDH.

Unsolved Problems

While transparent price discovery, programmatic liquidity, and atomic settlement are significant improvements over the traditional model, on-chain underwriting also brings its own set of problems.

None of these mechanisms solve for the quality of the project. Pump.fun’s bonding curve ensures fair access to the price curve, but says nothing about the credibility of the project behind the token. HIP-6, too, is open about this drawback. It mentions nothing about token quality, governance, or holder protections.

Traditional underwriters bear reputational and legal liability when an offering fails. A bank’s name on a prospectus signals that someone with skin in the game reviewed the issuer. On-chain mechanisms offer no equivalent recourse. Coinbase’s Echo comes close through KYC, issuer disclosures, and selling restrictions. But it does so by reintroducing gatekeeping that on-chain underwriting is designed to eliminate.

Whether token launches constitute securities offerings also remains unresolved in most major jurisdictions. A softened U.S. enforcement climate has made permissionless issuance easier to ship, but the underlying legal uncertainty hasn’t vanished.

But these are early days, and I expect improvements to make this an even better proposition than the legacy systems for capital formation.

The entity that controlled where an asset was born has always captured the most durable fees in finance.

Between 2012 and 2021, Goldman Sachs led more U.S. IPOs than any other bank. Yet the benefit transcends the unmatched fee revenue the IPOs brought in for the bank. Once Goldman underwrote an IPO, it typically also became the primary advisor for follow-on offerings, mergers and acquisitions, and debt issuance for that company.

We saw how pump.fun earned over a billion dollars in revenue by offering a reliable platform for 16.8 million tokens to be generated through its mechanism. The Raydium slump showed the same pattern as a corollary. Once it lost control of the token birth pipeline, 35-40% of its revenue disappeared overnight.

With on-chain underwriting, the system remains the same, and only the entity changes. From being a bank or a syndicate desk, it’s now changed into a protocol. This protocol offers a transparent and auditable process of allocating tokens without demanding a relationship with insiders.

In return, it expects you to conduct the entire trade using a unit of account that contributes to the protocol’s coffers: its native token. And I think it is a trade-off that also benefits the investors. A captive demand for native tokens leads to locked float and stickier liquidity.

This makes it competitive not just between traditional and on-chain underwriting, but even among on-chain players. The fight has moved upstream from fighting over the secondary market to controlling who gets to set the first price, allocate the first tokens, and decide which currency an investor needs to show up with.

That’s it for today. I will be back with another analysis.

Until then, stay curious!

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.