On March 17, the SEC and CFTC handed crypto the rulebook it has been begging for since 2013. I want to feel good about this, and I am trying.

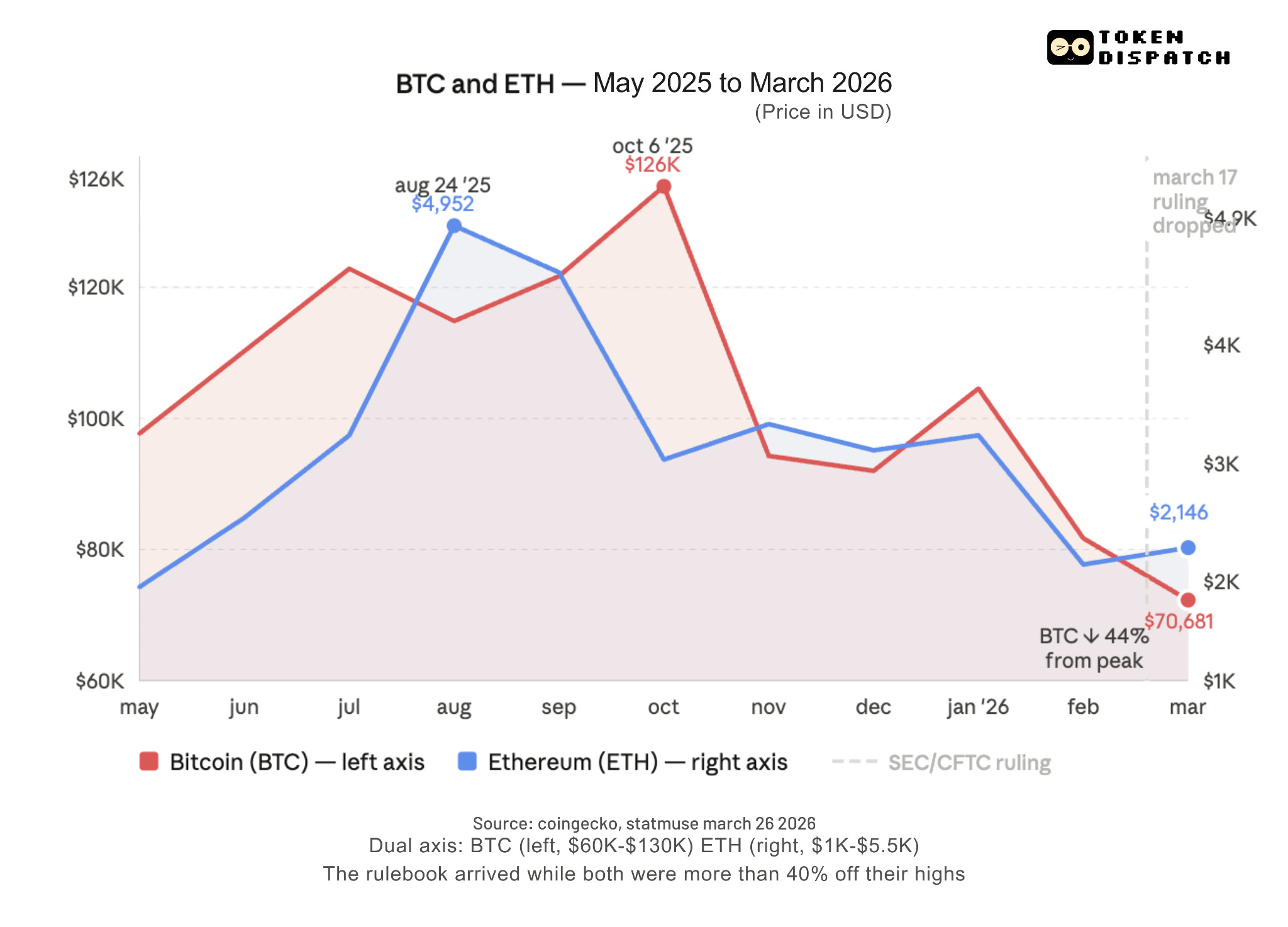

Bitcoin is down 44% from its October high. ETH is sitting at ~ $2000, less than half of its value from seven months ago. The altcoin market cap has shed $470 billion since its peak. The Fear and Greed Index is at 11. Not just 11 on a bad week, but 11 out of 100. This is when people have stopped arguing about the bottom and started selling whatever is left.

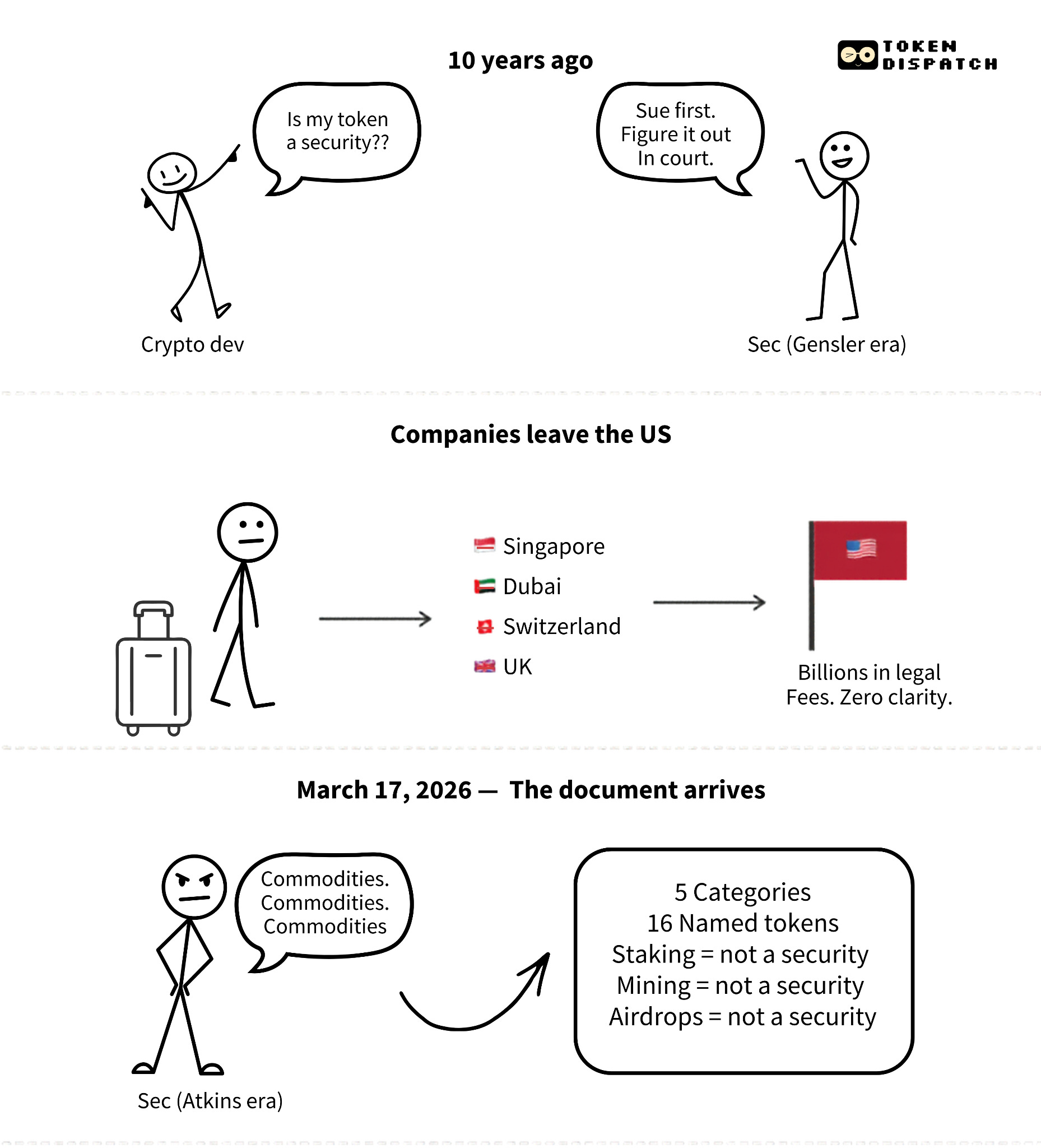

And into this, on March 17, the SEC and CFTC published a document that finally tells you what your tokens are. After ten years of lawsuits, hundreds of enforcement actions, and billions in legal fees. Companies that packed up and moved to Singapore rather than play a guessing game with Gary Gensler. And the answer arrives the week that ETH broke below $1,900.

But here’s the thing, while the token economy bleeds, everything beneath it is thriving. Stablecoins crossed $316 billion in circulation, and real-world assets (RWAs) are at $26.5 billion on-chain and growing. So much so that Morgan Stanley is building a crypto trust bank. Meta gave up on the metaverse, but is putting stablecoins into WhatsApp. Stripe is processing $400 billion in stablecoin volume. Nasdaq is building a tokenised equity venue. Crypto is becoming the backbone of global finance, most of the time without a token attached.

Crypto is no longer just a speculative asset class. The regulatory clarity that arrived on March 17 was made for the first version of crypto. But it arrived during the second one.

That does not make it meaningless.

SEC Chairman, Paul Atkins once said, “We’re not the Securities and everything commission anymore.”That sentence may have come a bit late?

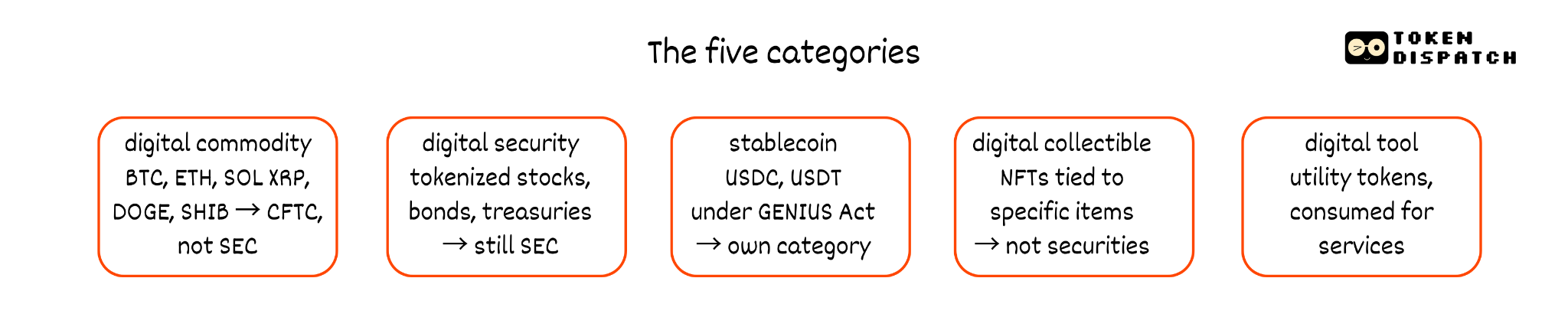

For the first time, U.S. regulators have a shared vocabulary for what crypto is. Five categories, and every token fits into one of them. I’m going to give you the definitions, read as if you have never heard this before.

Digital commodities are the big one. A digital commodity is a crypto asset whose value comes from the programmatic operation of a functional crypto system combined with supply and demand dynamics. Its value does not depend on the managerial efforts of a central issuer. If the network is genuinely decentralised and operational without any single company holding it up, the asset is a commodity. The CFTC jurisdiction, not the SEC.

Sixteen major tokens are officially named as digital commodities including Bitcoin, Ethereum, Solana, XRP, Cardano, Avalanche, Polkadot, Chainlink, Dogecoin, and Shiba Inu. DOGE and SHIB qualify because there is no promoter whose efforts drive their value. There are no promises, roadmap, or team whose continued work is essential to the token’s worth. That is why they are commodities and not securities. The test is whether someone is promising you returns based on their work.

Digital securities are tokenised stocks, bonds, and Treasuries. Basically, assets that were securities before they got put on a blockchain and remain securities after. The SEC keeps these. Full stop.

Digital collectibles are NFTs tied to a specific item or experience. Digital tools are assets you use to access software or services, with no expectation of a return on investment. Stablecoins have their own category under the GENIUS Act framework.

Staking, mining, and airdrops are cleared. The ruling explicitly states that receiving mining rewards, participating in on-chain staking, or receiving airdrops of digital commodities are not considered securities transactions. This removes one of the biggest legal risks hanging over proof-of-stake networks since the Gensler era. Wrapping a non-security token is also cleared.

The 16 named tokens are all base-layer infrastructure with years of decentralisation behind them. DeFi protocol tokens — JUP, POL, METEOR, and most of what launched in the last two years — are not named and do not obviously qualify. A functional crypto system with no central party overseeing participation is a high bar. Most actively developed protocols don’t clear it. The grey zone the interpretation was supposed to resolve is still grey for most of what people actually hold.

Value must come from the programmatic operation of a functional system, not from someone’s promises. That single test separates a decade of ambiguity into something a compliance officer can really work with.

There’s A Catch

The release does not constitute formal rulemaking under the Administrative Procedure Act and does not have the binding force of a statute or duly promulgated regulation.

You want to read that sentence again. The 68 pages that we have been waiting for is an interpretive release. Not a law or even a regulation. It’s just an agency statement of position that the current SEC and CFTC chairs issued and they can rescind it anytime.

This interpretation is a formal agency action binding on the SEC and CFTC, though absent legislation it could be modified by the agencies under a future administration. The document itself reserves the right for the agencies to refine or expand their views. A future SEC chair with different politics can reverse it without going to Congress. The next administration does not even need a new law. Just needs new leadership.

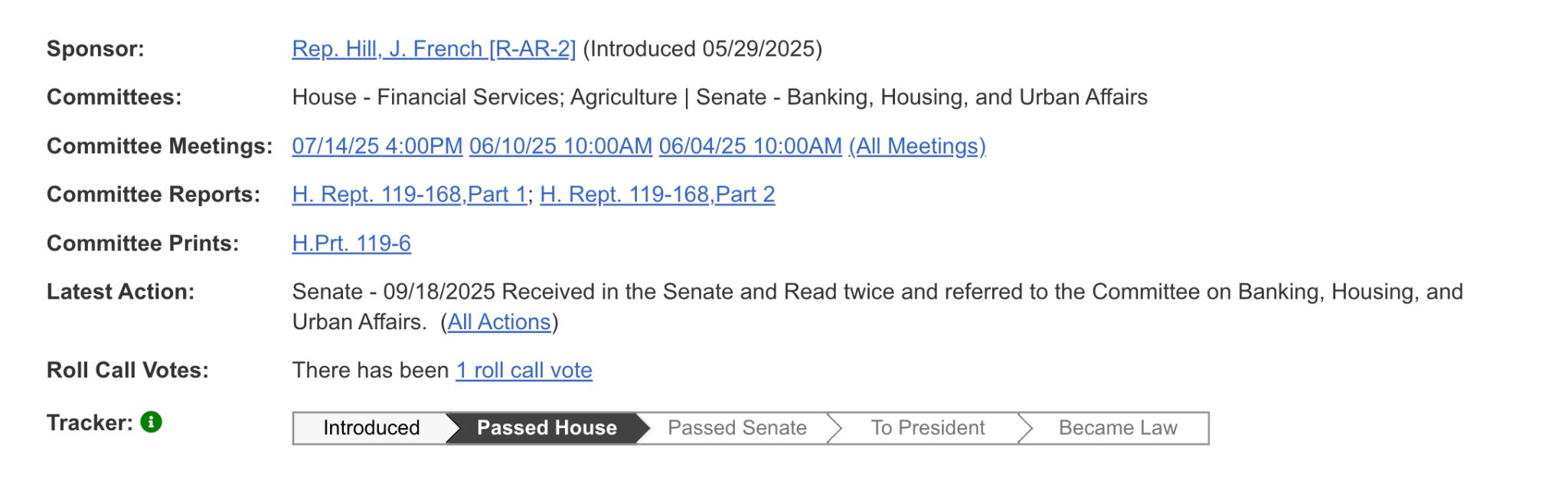

Atkins knows this. He said it on the day of the release, calling for Congressional action to provide more durable clarity. He framed the interpretation as a bridge measure pending Congressional action on comprehensive market structure legislation. That legislation is the CLARITY Act. And the CLARITY Act is in the Senate.

The CLARITY Act

The House passed the CLARITY Act in July 2025 by a vote of 294. Bipartisan is a good margin that suggests a real consensus.

Then it hit the Senate and stalled.

The issue that stopped it was stablecoin yield. Banks argued that allowing crypto platforms to pay interest on stablecoin balances would trigger deposit flight. People pull money out of savings accounts and park it in USDC for a higher return. The banking lobby went to work. The Senate Banking Committee pulled the scheduled markup in January 2026. The bill went nowhere for two months.

Read: The CLARITY Paradox ⚖️ - by Prathik Desai - Token Dispatch

On March 20, Senators Thom Tillis and Angela Alsobrooks confirmed an agreement in principle on stablecoin rewards, backed by the White House. The deal is that, passive yield on stablecoins is banned. Activity-based rewards tied to payments and platform use remain permitted. Both sides are unhappy, which is usually how a compromise works.

But the yield deal is one of five things that need to happen before the CLARITY Act becomes law. The four remaining legislative steps run against the tightest calendar of the year.

A Senate Banking Committee markup; and a full Senate vote (requiring 60 votes)

Reconciliation with the Agriculture Committee

Reconciliation with the House version

A presidential signature

The Banking Committee markup is targeted for the second half of April, after Easter recess. Senator Bernie Moreno has warned that if the bill does not reach the Senate floor by May, digital asset legislation may not move forward for years.

There is also the Iran war eating up Senate floor time. There is the voter-ID bill that Trump said he wants passed first. There are still unresolved DeFi provisions, with Senate Democrats citing illicit finance concerns. There are unresolved ethics provisions, specifically whether senior government officials should be barred from personally profiting from crypto assets, a question with obvious political sensitivity given the current administration’s crypto holdings. And Senate Republicans are now discussing attaching community bank deregulation to the bill as a political trade, which introduces a whole new set of negotiations.

The House Financial Services Committee recently held a hearing on “Tokenisation and the Future of Securities: Modernising Our Capital Markets.” The witness list is Kenneth Bentsen of SIFMA, Summer Mersinger of the Blockchain Association, Christian Sabella of the DTCC, and John Zecca of Nasdaq. Nasdaq and NYSE are both building tokenised equity venues. The DTCC controls current settlement. If the DTCC validates blockchain efficiency, the argument is effectively over.

So, the infrastructure is being built on top of a rulebook that might not exist in two years. That is the tension the industry is living in right now. Companies are making billion-dollar decisions to build custody systems, tokenization platforms, and staking infrastructure, all based on an interpretive release that carries persuasive authority but not statutory force.

What is Permanent, And What Isn’t

For the reader with a position in any of the 16 named tokens, your ETH, your SOL, your XRP. These are formally recognised digital commodities under U.S. law today because two agency heads said so. That classification remains in place as long as those agency heads, or their successors, agree.

If the CLARITY Act passes, it becomes law. No future chair can undo it without Congress. The named assets become permanently defined, and the taxonomy becomes binding.

If it doesn’t pass by May, the taxonomy rests on the opinion of a single administration. The 16 named assets are safe for now, but everything is not named. Most DeFi, most new tokens, anything permissionless with no identifiable issuer is still in a grey zone that the interpretation explicitly didn’t address.

The most awaited sentence is written in pencil.

Someone needs to pick up a pen to make it permanent. It all depends on what happens in the Senate in the next six weeks. Could the rules last long enough for all of it to matter?

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.

Exquisite summation of a very complicated and multi-faceted system. Thank you for this. We could call it "Clarity about CLARITY."