Hello,

In March this year, OpenAI shut down a feature that let AI agents shop on your behalf. Barely 30 Shopify merchants used the feature in five months since its launch. There was nothing wrong with the payments infrastructure. The problem was that there were no rules in place to ensure a seamless shopping experience. What the agent could buy, who collected sales tax, how fraud was caught, who handled returns — none of it was settled.

Giving an agent a wallet or building payment infrastructure has been easy to crack. But allowing individuals or businesses a trusted and governed way to use an agent to spend their money is tricky. Only programmability and rules can ensure a trusted environment. This gap in the governance layer has become an opportunity in the agentic economy.

Last year, AI agents settled $73 million across 176 million transactions. The number might seem insignificant now, McKinsey projects that AI agents will mediate $3-5 trillion in global consumer commerce by 2030.

Companies building this economy are racing to own the governance layer, including spending controls, identity checks, and policy enforcement that determine which agents are trusted with budgets.

Today, we map out who is building the banking layer for the bots and what’s in it for those who dominate it.

Onto the story,

Prathik

Why Own Multiple Layers

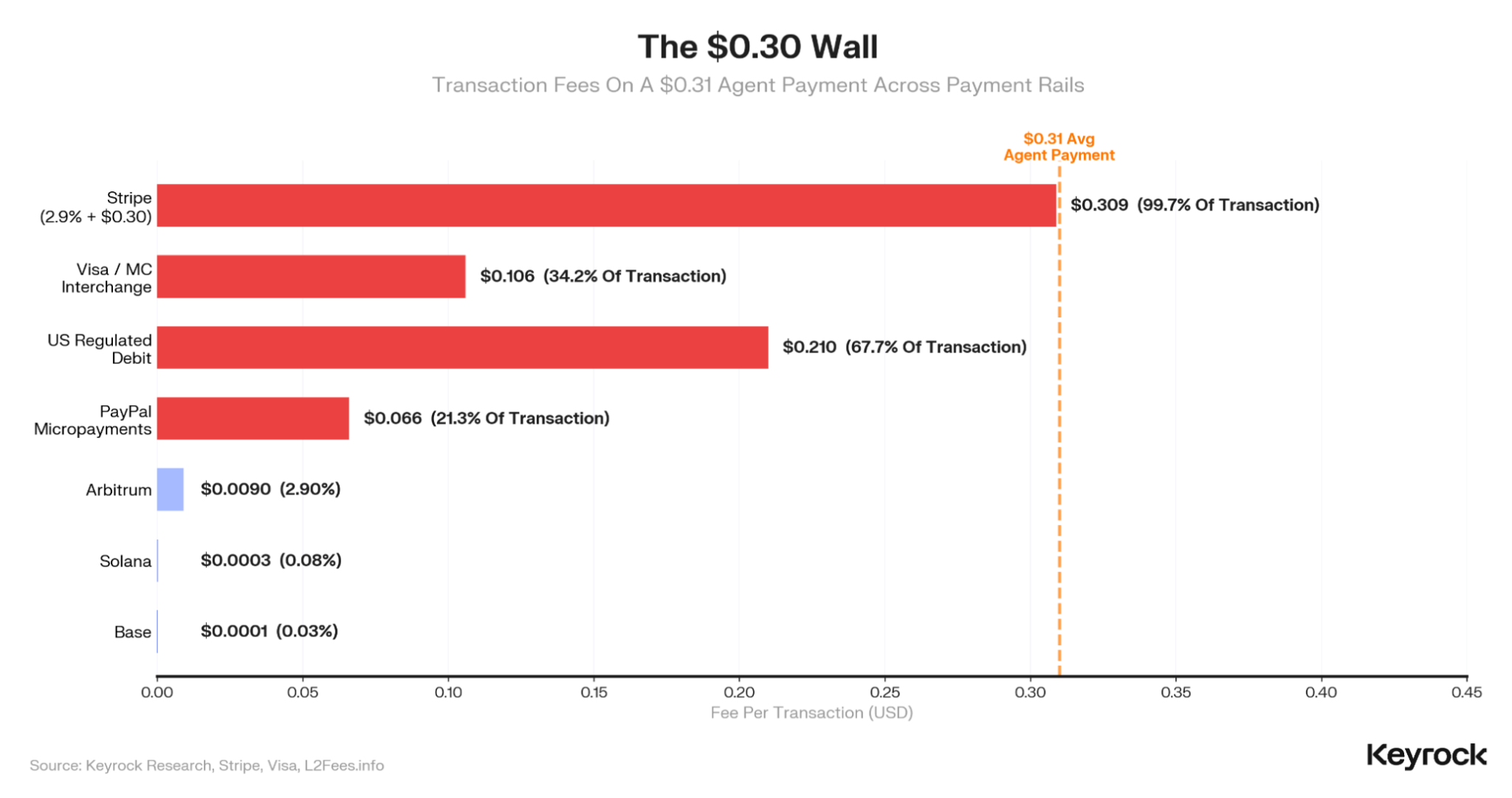

The economics of processing agent payments are brutal. The average payment made by AI agents over the last 12 months was 31 cents.

Consider what a 31-cent payment would leave behind for those orchestrating the transaction across several layers in the background. Stripe’s standard pricing of 2.9% plus 30 cents in fixed fees leaves the merchant with less than a tenth of a cent. Visa interchange swallows a third of it. On the other hand, Layer-2 stablecoin rails process the same transaction for $0.0001.

These economics established the case for crypto’s use across the settlement layer.

The payment infrastructure across the settlement layer is largely solved. Coinbase’s x402 protocol processed the vast majority of last year’s 176 million transactions, with around 3,900 merchants now accepting agent payments. Stripe and Tempo co-authored a competing protocol, Machine Payments Protocol (MPP), that launched in March with over 100 integrated services. Google, Visa and Mastercard all shipped agent payment products in the same window. That’s five competing payment architectures in 12 months.

But the problem with agentic payments is that nobody will get rich by processing 31-cent payments. So, the value concentrates in the float and in enforcing the rules around how agents make the payments.

Last week, we explained how businesses could capture value by owning the wallet layer that holds the stablecoin balances for AI agents. But the float is only one of many such value layers worth capturing. The other is the rules governing how that float gets spent.

These rules include spending controls, agent identity, policy enforcement, audit trails, and liability allocation when transactions fail. This layer is wide open.

In April, American Express launched Agent Purchase Protection, an insurance product that covers erroneous purchases made by AI agents. This is an implied admission of the state of the governance layer across AI agents. There’s value to be captured here by addressing the missing governance in an industry expected to grow to $3-5 trillion in less than five years.

This is why the incumbents are now racing to capture the governance layer.

But at what level should this layer be built? It can be a bank, a developer API or even a wallet.

Wallet as the Governance Layer

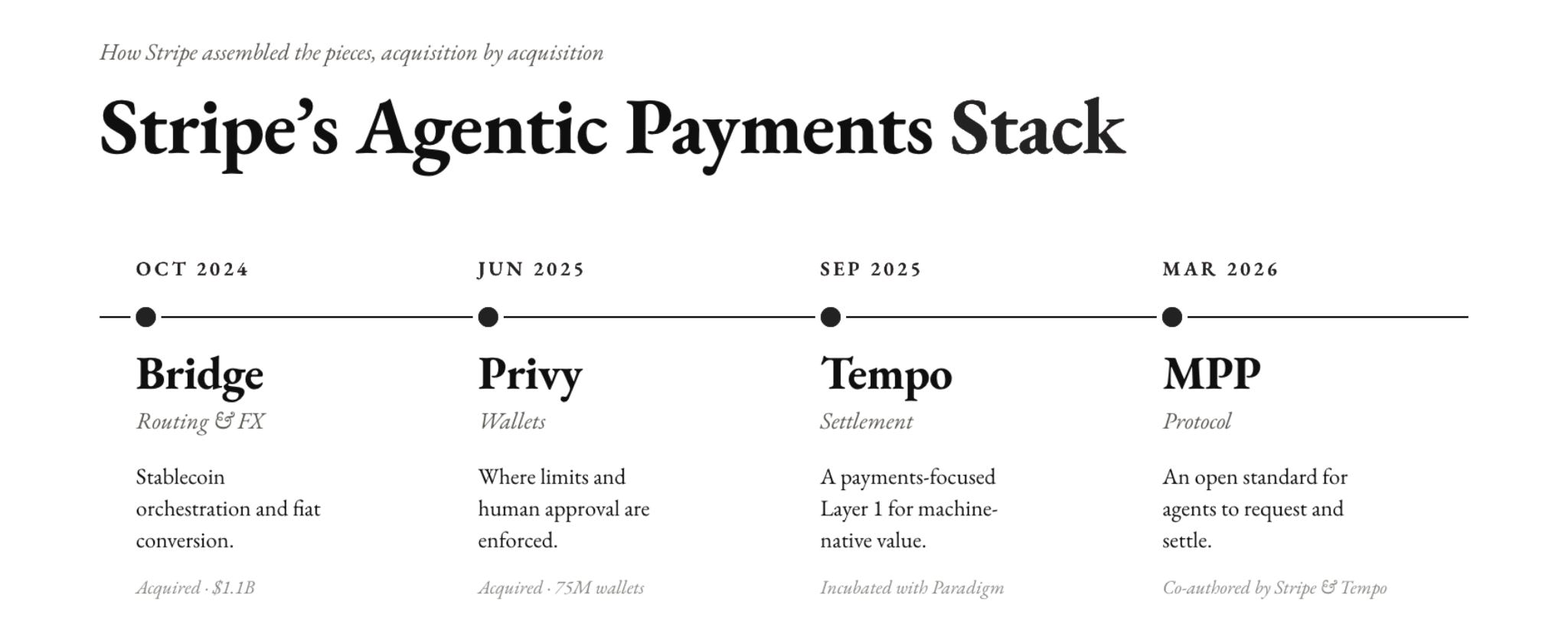

Every dollar that an agent spends passes through the wallet. This makes it the best point to enforce spending limits, identity checks and human approvals. Once you control the wallet, you control the governance. Stripe, the payments infrastructure company, learned this early on.

In June 2025, Stripe acquired Privy, a company that built embedded wallets for consumer crypto apps. Through the acquisition, Stripe inherited 75 million wallets across 1,000+ developer teams. These wallets now sit at the very chokepoint where every policy, spending limit, and human approval can be enforced before any money moves.

Stripe has also assembled an entire agentic payments stack. It acquired Bridge to handle stablecoin orchestration and fiat conversion. It also partnered with Paradigm to incubate Tempo, a payments-focused Layer 1 blockchain. Stripe and Tempo co-authored the Machine Payments Protocol (MPP), an open standard for how agents request, authorise and settle payments.

Read: Why Stripe built its own chain

Stripe’s agent-ready financial stack now lets software check balances, pay invoices, store funds, create virtual cards and send money. An agent can execute routine payments on its own, but escalates anything outside its policy parameters for human review. Treasury balances are backed by noncustodial Privy wallets across more than 150 markets.

Even when Amazon had to allow its developers to give AI agents the ability to spend money, it chose two wallet companies - Privy and Coinbase. Not seasoned financial players like banks or card networks, but a wallet provider that is barely five years old.

This is because the wallet serves as the ideal checkpoint, allowing the right level of human intervention to ensure the necessary checks and balances.

In its report ‘Who Pays the Agent’, Keyrock argued the agentic commerce market will “settle in the middle, where agents operate with significant autonomy but within cryptographically enforced boundaries that humans can audit and revoke.”

This is the position Privy occupies inside Stripe’s stack. The wallet enforces the boundaries within which the agent has to operate.

Here’s how the governance strategies on this stack function.

Privy offers two models for agentic wallets. In the first, the agent controls the wallet entirely and executes transactions within policy constraints without requiring human approval. This model works best for fully autonomous agents like trading bots and portfolio managers. In the second, users retain ownership of the wallet but grant the agent restricted permissions to operate as a signer. Users can revoke access at any time.

Stripe’s MPP follows a similar governance strategy.

MPP introduced a feature called sessions for high-frequency agent tasks. Under sessions, an agent pre-authorises a spending budget and then streams payments within that limit continuously without needing a separate request for each individual on-chain transaction. The MPP has implemented sub-cent billing for LLM inference and per-query pricing for data APIs.

This is the governance granularity that card networks cannot support.

Vertically Expanding the Stack

Although Coinbase’s x402 leads AI agentic payments today, Privy has an advantage that has little to do with crypto. It’s the distribution moat via Stripe.

Coinbase has 3,900 merchants that accept agentic payments. For every Coinbase merchant accepting agent payments, Stripe has roughly a thousand. In February, Privy said that if every Stripe merchant chose to accept machine payments, agentic commerce could scale through Privy wallets today. Stripe merchants don’t need to build bespoke crypto infrastructure.

While the race between Stripe and Coinbase is tightening, other traditional giants are also joining the race to expand vertically across the stack.

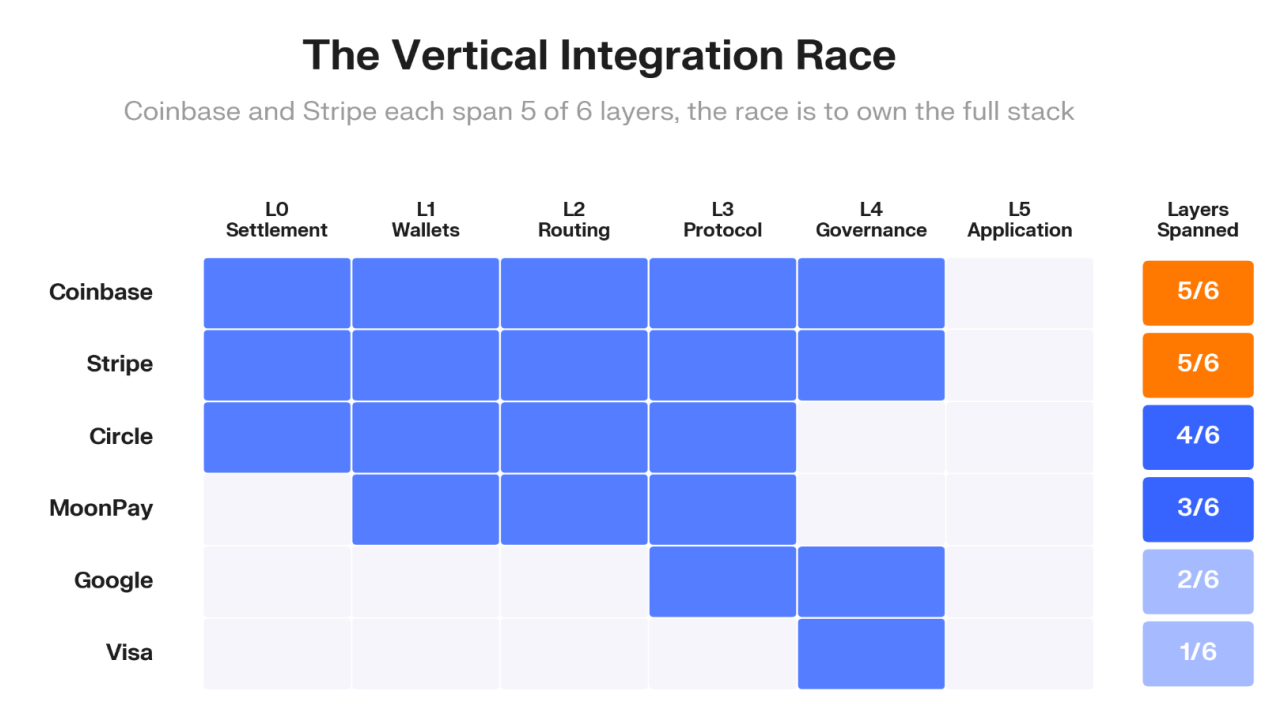

Keyrock mapped 179 projects across six layers of the agent payments stack: settlement, wallets, routing, protocols, governance and applications.

Coinbase and Stripe each span five of those six layers. Circle covers four. Despite their scale, Google covers two layers and Visa just one.

The incumbents spent over $8 billion in twelve months filling gaps in their stacks. Capital One acquired Brex, an AI-native software platform, for $5.15 billion. Mastercard acquired BVNK for $1.8 billion. Among these, the wallet layer and the AI software layer attracted the most aggressive acquisition activity. Stripe bought Privy, Fireblocks bought Dynamic, and Arbitrum bought ZeroDev. In each case, payment infrastructure bought a standalone wallet provider.

These deals collectively suggest that the market has picked a scarce layer. Settlement has become cheap and interchangeable, but programming permissions, budgets, and liability are where the value lies.

Vertically integrating across multiple layers also has a compounding effect.

Whoever owns this checkpoint can set the rules for spending, capture the float before it moves, decide which merchants, agents, and applications get trusted access and earn a fee to enable all these things. We saw it with the Privy-Stripe distribution moat.

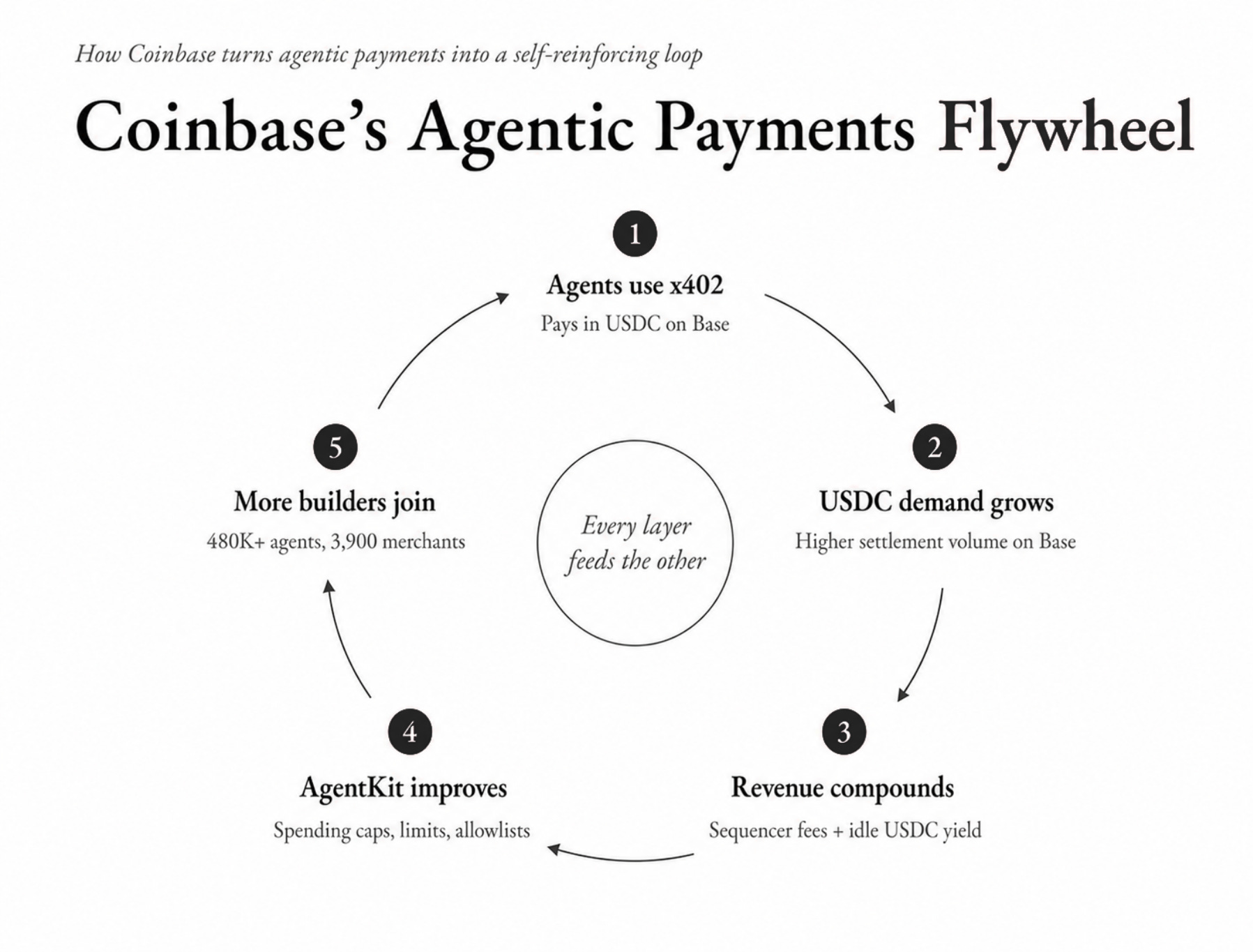

Even Coinbase’s position shows how this works. Every x402 payment creates USDC demand on Base, its Layer 2. That generates revenue on float. That revenue funds more agent tooling through AgentKit, which ships with session caps, per-transaction limits, and allowlists that restrict transfers to vetted contracts. More agents on AgentKit means more x402 payments. Every layer feeds into the other.

There’s a lot more investment activity by the incumbents.

Coinbase Ventures has also invested in Catena Labs, Skyfire and Payman, the three most prominent standalone governance startups. Circle’s cofounder Sean Neville founded Catena, and Circle invested in Skyfire. a16z led rounds for both. Visa backed Payman and partnered with Skyfire.

The same names that built the payment settlement infrastructure are funding the governance layer. The idea is that if governance remains a feature within the existing infrastructure, as Privy has built it with its two models, then incumbents can maximise their revenues. If governance becomes a standalone layer, they win through their portfolios.

What’s in Owning the Governance Layer?

Processing payments has never been the most valuable position because, at some point, financial rails commoditise. Once that happens, the margin shifts toward the layers that decide whether a transaction is allowed to happen and under what conditions.

Historically, many industries have gone through the same commoditisation.

Consider what happened when the internet commoditised cable. All internet service providers (ISPs) became indistinguishable and interchangeable. So the telecoms had to expand vertically to stay competitive.

India’s top telecom networks - Jio and Airtel - started bundling hundreds of TV channels, subscriptions to half a dozen OTT platforms, unlimited voice calling, a set-top box and a free router into a single broadband plan. Similarly, AT&T acquired Time Warner for $85 billion to become an integrated media and telecom giant. The idea was to combine Time Warner’s premium content, like HBO, Warner Bros., and CNN, with AT&T’s massive distribution network to compete with streaming platforms like Netflix and Amazon.

When broadband connection - the underlying infrastructure - became the least valuable part of the package, the value shifted to the content, the relationship and the bundle of offers that best attracted customers.

We saw this play out in crypto, too.

Settlement was supposed to be at the protocol level. Think of Ethereum as the shared ledger everyone settles on. When Coinbase launched Base as a faster, less congested Layer-2 chain, the company began earning money from gas fees on every transaction it settled on its own chain. Coinbase now earns roughly $60 million in annualised sequencer revenue by processing transactions on Base.

The players building agent payment rails have learned from watching this.

In The Agentic Float, we explained how an economy can emerge by controlling the stablecoin balances agents hold between transactions. This allows the companies that capture the wallet layer in the stack to add a revenue stream.

The governance layer adds another revenue stream, and possibly a larger one.

Visa earned 0.28% on $14.2 trillion of its annual payment volume. That take rate not only includes a processing fee but also an implicit governance fee for the trust the payments company has built by preventing fraud, resolving disputes, and enforcing network rules.

Applying even a fraction of that take rate to agentic commerce, it tells us the magnitude of value it adds to the companies building on the governance layer. At McKinsey’s projection of $3 trillion in agentic commerce by 2030, a governance take rate of just 0.1% (about 35% of what Visa charges) would generate $3 billion a year. For context, Coinbase’s entire subscription and services revenue stood at ~$2.8 billion in 2025. The revenue from the governance layer on agent transactions alone could rival what Coinbase currently earns from staking, custody, and Coinbase One combined.

A company that has a presence across the wallet, settlement and governance layers of the agentic finance stack can earn yield on idle agent balances (revenue on float), fees from settlement (sequencer revenue on every transaction), and compliance fees (from enforcing the governance).

This is why vertical integration across the stack will be the only business model that lets a company remain competitive in the agentic era.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.