“The farther backward you can look, the farther forward you are likely to see” - Winston Churchill

Hello,

The current state of Digital Asset Treasuries (DATs) bears a striking resemblance to America’s closed-end funds of the 1920s. People purchased shares in closed-end funds, which then bought stocks in the public market. Indirectly, investors gained beta exposure to these stocks in the market and paid a premium in return for those shares. The speculative premiums on these funds peaked at 30% above the net asset values (NAV) of the funds until the stock market bubble of 1929 turned them into discounts. Investors learnt it the hard way that the math didn’t add up.

When I read this, it felt like déjà vu about what we saw unfold in the DATs ecosystem over the past few months. Hard not to draw parallels.

Bitcoin-based DATs, like Strategy, offered leveraged beta on BTC’s price. Investors paid a premium for it. The flywheel worked as crypto rallied, but it fell apart when the markets slumped. The trick to making DATs sustainable across market cycles is in what the token’s appreciation is linked to. Most crypto treasuries around BTC and ETH were leveraged bets that the prices of the underlying cryptocurrencies would go up.

But what if the token price were closely tied to the revenue generated by its ecosystem? What if it had little correlation to uncertainties? Even better, what if it were negatively correlated to how other asset classes behaved during macroeconomic uncertainties?

In today’s deep dive, I will explore why asset selection for DATs could decide how sustainable their treasury strategies are, using the case of a HYPE-based digital asset treasury (DAT) company.

Hyperliquid Strategies (ticker: PURR) started its DAT journey by incorporating Rorschach LLC, a Special-Purpose Acquisition Company (SPAC), and hold. It then reverse-merged the SPAC with Sonnet BioTherapeutics, a struggling Nasdaq-listed biotech company whose flagship cancer drug had spent years seeking a commercial partner.

It’s the same playbook that Twenty One Capital had used for BTC, backed by Tether, Cantor Fitzgerald, and Softbank.

Read: SPAC to the Future ⌛️

At launch, PURR held 12.6 million HYPE tokens, valued at $583 million, and $305 million in cash. Earlier this year, it deployed $129.5 million to purchase an additional five million HYPE tokens.

But why does Hyperliquid Strategy deserve a better outcome than the previous DATs?

A Different Jar

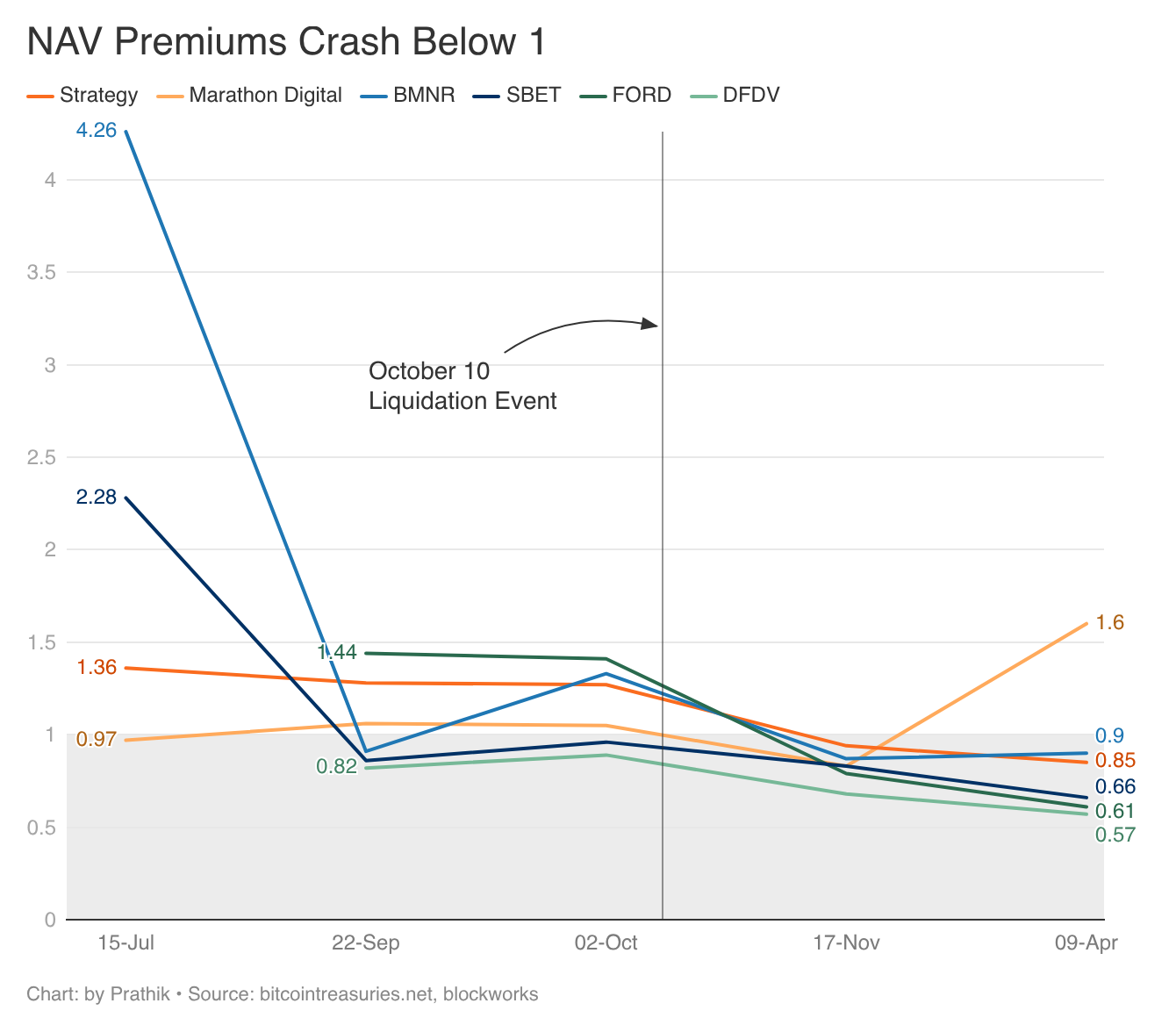

In the first wave of DATs, the wrapper itself was the innovation. A company could swap BTC for ETH, ETH for SOL, and the playbook worked just fine. That’s because the flywheel was built around the premium on net asset value (NAV) of the companies. It didn’t matter what the underlying asset was. As long as DAT shares traded at a premium, investors bought in, expecting more upside beta on the token’s price appreciation.

However, that bet flipped when the market struggled to recover from the crypto industry’s largest single-day liquidation.

Although the liquidations were sudden and followed US President Donald Trump’s new trade tariff threats against China, what happened with the DATs was not unexpected.

A couple of months before the liquidation event, we wrote about the risks that the leader of the BTC treasury pack, Strategy, carried in its DAT model:

“The strategy works well during Bitcoin bull markets, as it is a conducive time for accretive capital that funds additional purchases while reported earnings soar from mark-to-market gains. However, the model’s sustainability depends on continuous market access and Bitcoin appreciation. Any significant crypto downturn would quickly reverse the Q2 results while fixed obligations by way of debt interest and preferred dividend payments continue.

Fast forward to mid-November, and we saw what had been feared about DATs for months unravel in real time: sliding mNAVs, slowing treasury purchases, and falling DAT company share prices.

Read: Where’s DAT Beta? 🎁

The problem with the playbook was that all top three treasury assets - BTC, ETH, and SOL - were tied together by a common, awkward feature. They didn’t generate cash flows. Their price appreciation was linked to how people traded the cryptocurrency. And that trading was driven by multiple factors: ETF flows, institutional interest, conversations on online forums and communities, and investors’ perceptions of BTC’s role as digital gold in the macroeconomic landscape.

Surely, ETH and SOL generated staking rewards to offset their slow token appreciation. But staking rewards are paid in newly minted tokens. Each time ETH and SOL staking rewards are paid, they dilute current token holders to pay validators.

A treasury holding any of these assets, whether BTC, ETH, or SOL, acts like a closed-end fund with a single non-dividend-paying position. The only way it makes money is if the token price rises or if the premium to NAV widens. The first is beta, and the second is driven by narrative.

Although Ethereum and Solana generate fees, a comparatively small portion of revenue gets routed back to its holders. In 2025, Ethereum generated about $515 million in chain fees, while Solana collected $645 million. Most of it didn’t reach token holders; it was either captured by validators or offset by fresh issuance.

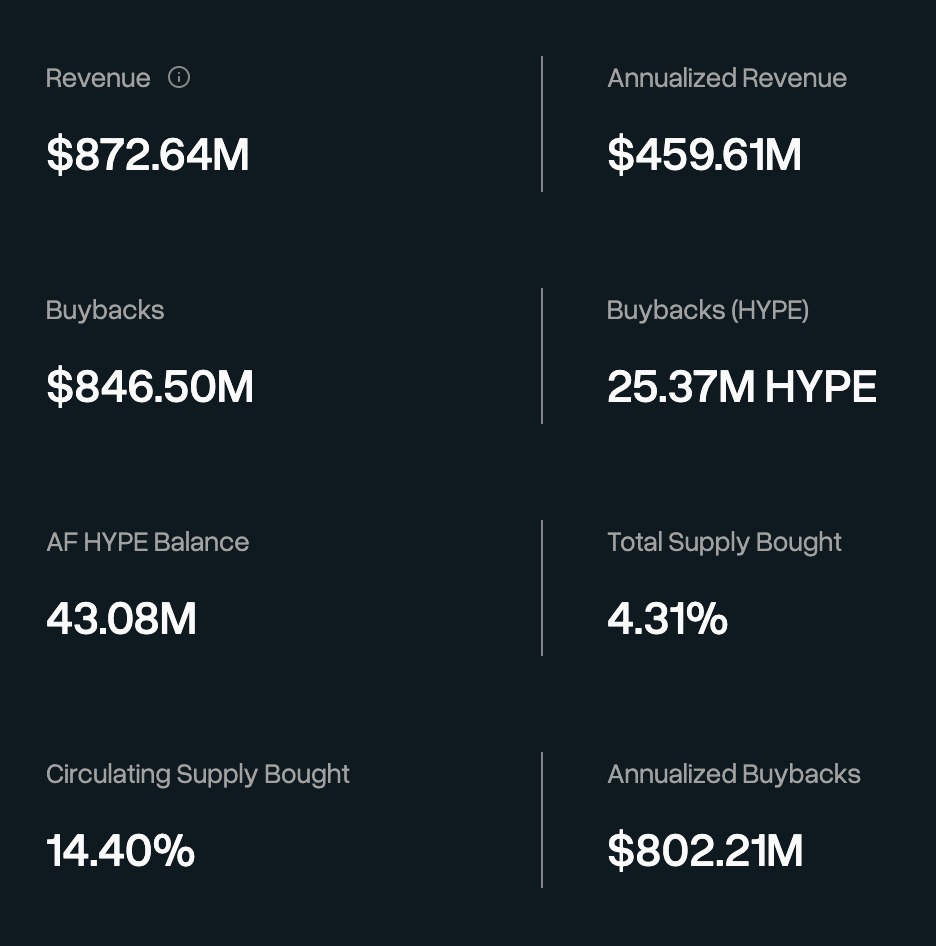

Compare that with almost a billion dollars in fees that the Hyperliquid protocol generated last year. It becomes even more convincing when you factor in that 97% of those fees were routed back to HYPE holders through buybacks via the Assistance Fund.

Read: Burn, Baby, Burn 🔥

Hyperliquid now runs $5-7 billion in daily perp volume, roughly $200 billion a month, generating around $730 million in annualised fees from trading activity. So, each dollar traded on Hyperliquid contributes toward strengthening the underlying fundamentals of HYPE’s pricing.

This makes HYPE treasuries feel less like holding BTC or ETH in a vault and waiting for the market to value it. Instead, it feels like holding a receipt against the fee stream of a derivatives exchange.

Any listed wrapper holding HYPE, including the most recent bet by PURR, is still fundamentally a bet on HYPE’s price. Its corporate structure is the same as that of a BTC, ETH, or SOL treasury company. This makes it easy to look at them through the same lens. Yet I am more optimistic about a HYPE treasury company given the underlying factors driving the token’s price movement.

The share price of PURR reflects an indirect claim on the present value of all cash flows that the Hyperliquid protocol can generate from its derivatives business.

You don’t have to take my word for it. Hyperliquid has shown it multiple times recently.

A Proven Case

During the US-Israel-Iran war last month, risk assets and traditional markets stumbled. HYPE rallied 40%, while S&P and BTC lingered. The former fell by 3-5%, while the latter gained 5%.

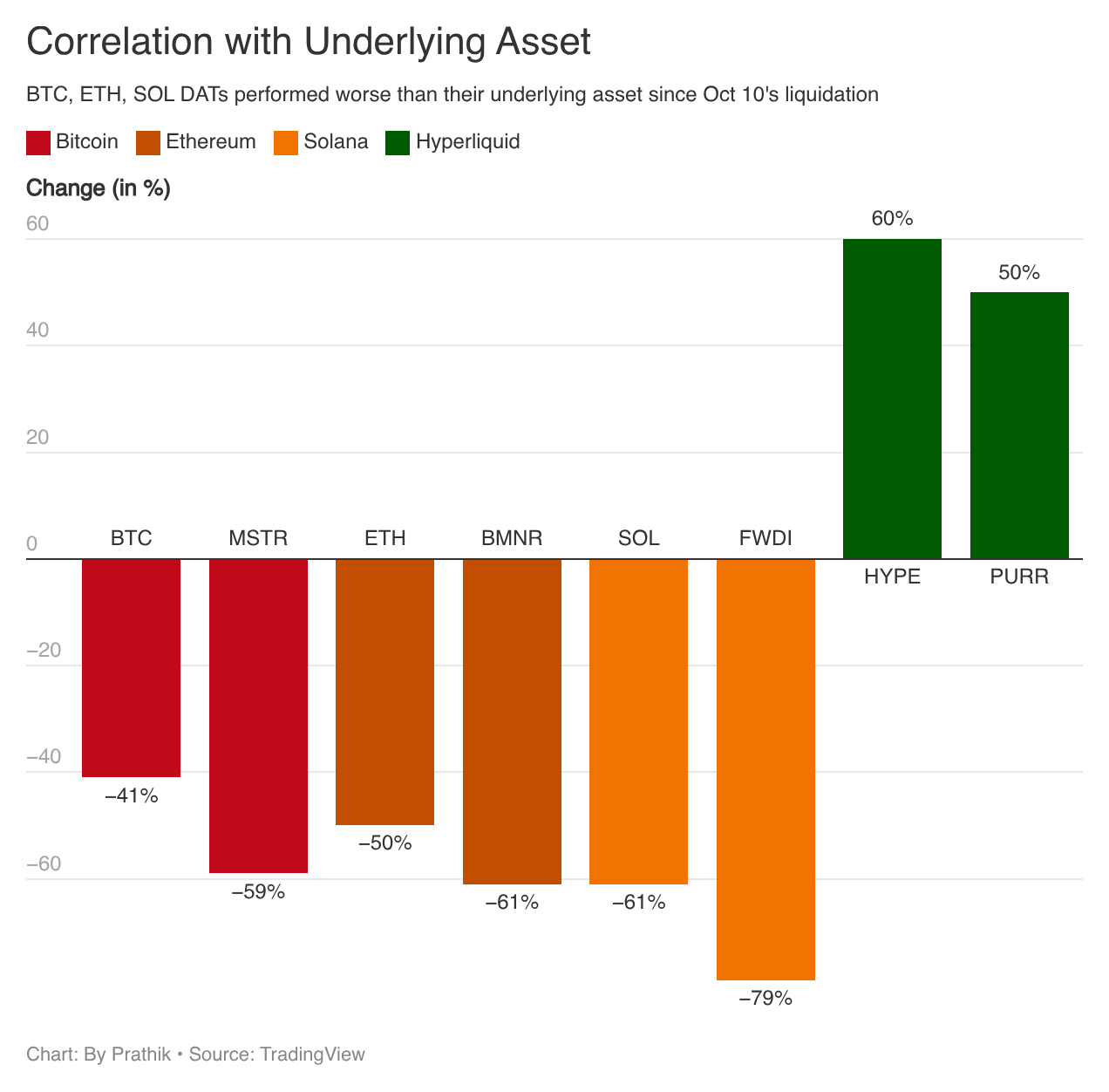

Since the largest crypto liquidation event on October 10, HYPE has appreciated by about 60% while BTC slid by 40%.

It wasn’t just a coincidence. Volatility driven by uncertainty is bad for a passive store of value and excellent for a derivatives exchange. Uncertainty drives perp traders to hedge their positions. Liquidation events generate fees on both sides of the trade. The same conditions that eat into the mNAVs of BTC treasuries become conducive for printing more money for a perps venue.

The bear market that rang a death knell for BTC and ETH treasuries brought record volume and fees for Hyperliquid’s ecosystem. While the former have no option but to wait out the market meltdown, Hyperliquid’s P&L thrives in these conditions.

Hyperliquid’s HIP-3 markets have only strengthened this thesis by bringing traditional assets, including metals like Silver and Gold, on the blockchain and enabling investors across financial markets to express their opinions across asset classes.

Read: Hyperliquid is Taking on CME, not Binance

This is the single biggest reason I believe HYPE’s DAT strategy stands apart from the rest.

Nobody’s Safe

PURR’s DAT strategy is still a bet on HYPE’s price. Hyperliquid could lose its perp market share to competitors like Lighter, Aster, or some yet-to-be yet conceived protocol.

PURR’s institutional backers pitched their DAT strategy as “the only way US investors can access HYPE”. But if fundhouses get approval for their pending HYPE spot ETFs, it could make the entire wrapper obsolete. Both 21Shares and Grayscale have filed their applications.

However, what inspires confidence despite these challenges is the choice of the underlying asset.

The older DATs had to worry about retaining the premium on their NAVs. This is a function of market psychology and investor confidence in the model. A HYPE-based DAT has to answer a simpler question: will Hyperliquid keep earning? This question is more a function of weekly fee data, perp market share, protocol’s roadmap - which also has HIP-4 lined up.

Read: Why HIP-4 Will Take Over Finance

All of these are numbers an analyst can use to make informed decisions. The analyst can still falter, but there’s data that backs the answer.

There’s a counterargument here.

What if Ethereum and Solana overtake Hyperliquid in terms of fees generated? That’s not impossible. But it becomes far more difficult when you consider the revenue ploughed back to HYPE holders through buybacks.

Although Ethereum routes a portion of its fees back to ETH holders, it is offset entirely by the new ETH it issues to validators. Solana’s fees accrue to validators, who keep them. Little trickles down to Solana holders. For either Ethereum or Solana to match what Hyperliquid does with its token, they would need to rewrite the underlying tokenomics. Along with that, the network activity will also have to multiply several times from the current level. None of them is an overnight process.

Even if it happens, I expect the same thesis to hold true. I don’t claim that HYPE will always be the only successful asset for DATs. I believe that DATs built on assets whose ecosystem generates consistent revenue for its holders will outlive DATs built on assets that do not generate consistent income.

Both these models are significantly different. The first wave of DATs expected investors to underwrite by believing in a narrative. The second expects investors to believe in the cash flows.

The closed-end funds that survived the 1929 bubble were those whose stocks continued to pay dividends during the drawdown. Everything else was simply a wrapper around a bet.

HYPE-based DATs might still end up in the same graveyard as the other DATs. Nobody knows for sure. But their critique will most likely be an argument about market share, fee durability and other fundamental business metrics. At least it won’t be another debate that ends with “I told you so,” as we saw with the collapse of BTC DATs.

That’s it for today. I will be back with another deep dive.

Until then, stay curious!

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.