Hello,

Kalshi just launched markets on GPU compute prices, meaning you can now bet on where GPU rental costs will be three months from now. And for the first time, compute has a forward curve. In Part I & Part II, I covered how compute is becoming tradable and how it is being financed underneath. Today, I want to complete the picture by walking you through every layer of the market forming around it.

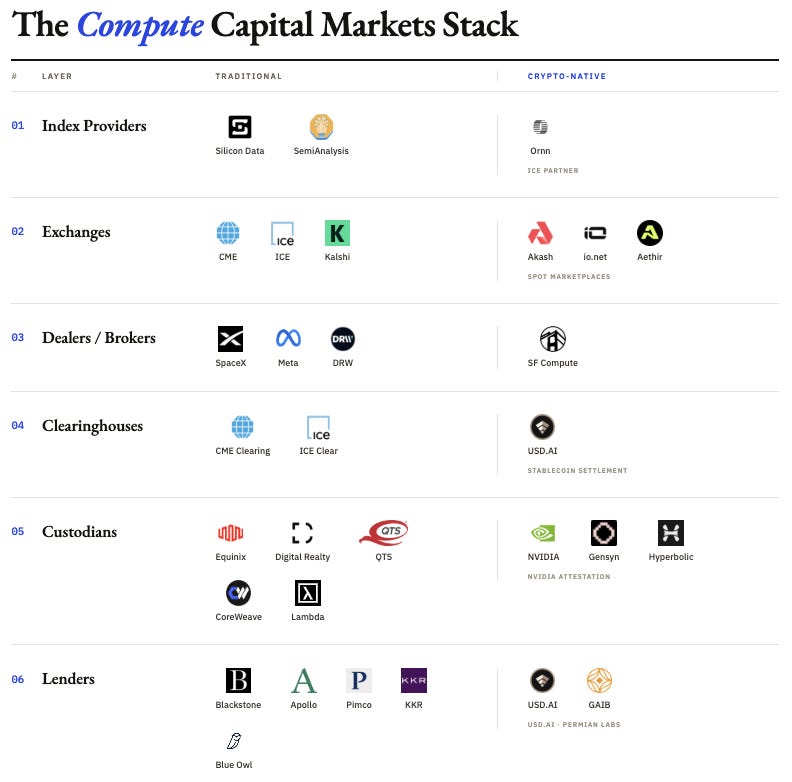

Each layer of compute being built is either held by the oldest financial institutions or crypto-native startups that didn’t even exist a few years ago. We’ll map each layer to see where crypto infrastructure is genuinely load-bearing versus where traditional players have an advantage. Let’s dig in!

")

The Pricing Stack

Let’s start with price. All commodity markets in the world begin here because everything that comes after futures contracts and lending covenants gets settled against this one reference number.

In oil, for instance, the number is published by firms called price reporting agencies. The largest of these agencies today is Platts, which is now part of S&P Global. What Platts basically does every day is survey traders and refineries, collect the prices at which crude is sold, and publish a single reference price. This price is then used in all futures contracts and cargo deals. Warren Platt started this back in 1909 as a trade magazine with $2,500. And over a century later, Platts remains the dominant reference price for physical oil.

Platts survived for a century because once a benchmark is set for the first generation of contracts, switching away from it later becomes almost impossible. You would be surprised, but even Platt’s most vehement detractors still use it because they have legacy contracts and other derivative instruments based on Platts, and adopting any other price source would create a basis risk across their entire book. The benchmark is more permanent than even the companies trading around it.

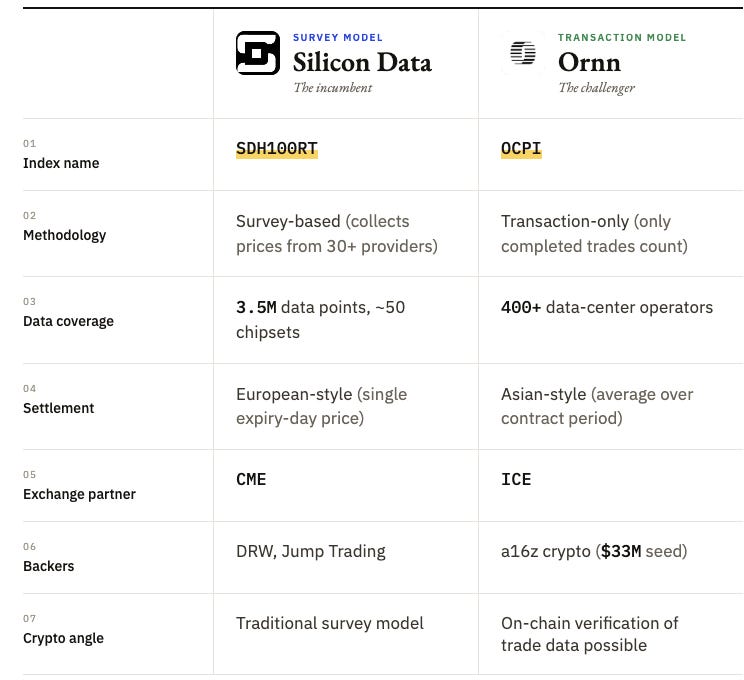

In Compute Markets, two firms are racing to become the Platts of compute. The first is Silicon Data, which I introduced in Part I. It collects rental-price data from over 30 GPU cloud providers, covering 3.5 million data points, and publishes a daily index, called SDH100RT, on Bloomberg terminals. CME has announced that its compute futures will settle against this index.

The second firm is Ornn, which, instead of surveying providers on what they charged, only counts prices from transactions that actually completed on its own exchange venue, where over 400 data-centre operators and AI companies trade. This is very different from how Silicon Data does it because benchmarks built on surveys can be gamed. In oil, traders have manipulated Platts assessments for decades by submitting inflated quotes during the assessment window to push prices in directions that benefit their positions.

Ornn’s approach of using only completed transactions makes it far harder to pull off, and crypto infrastructure gives an edge: if those transactions settle on-chain, the raw trade data becomes verifiable to anyone who wants to check the ledger. You never have to trust that the benchmark provider filtered the data correctly.

This model of verification does not exist anywhere in traditional commodity markets and could help make compute benchmarks more trustworthy. Ornn has over 400 data-centre operators on its platform and has also announced an integration with ICE to settle their compute futures on Ornn’s index.

Now, the exchange side of this layer is barely developed. The first-ever compute swap was cleared in December 2025, and that too on Ornn’s own venue. The biggest reason is that 78% of compute supply is still concentrated among the four hyperscalers, and there is no standardised, tradable unit. A rating system for GPU clouds was tested that grades providers on networking quality and uptime. Because buyers are willing to pay significantly more per GPU-hour for higher-rated clusters, the annual revenue difference between the lowest and highest tier on the exact same hardware can reach up to $15 million. This tells you how far off compute still is from being a fungible commodity where one unit equals any other.

DePIN platforms like Akash and io.net sit on the other side of it. They provide spot markets where compute can be traded at hourly rates, for a fraction of what hyperscalers charge. But the problem with these is that they are not yet very reliable. A developer who had tested four DePIN providers had two of them shut down on him in just eight months of setting up. But trades here are visible and on-chain, so if DePIN continues to grow, these platforms could become another raw source of verifiable price data, making compute benchmarking more credible.

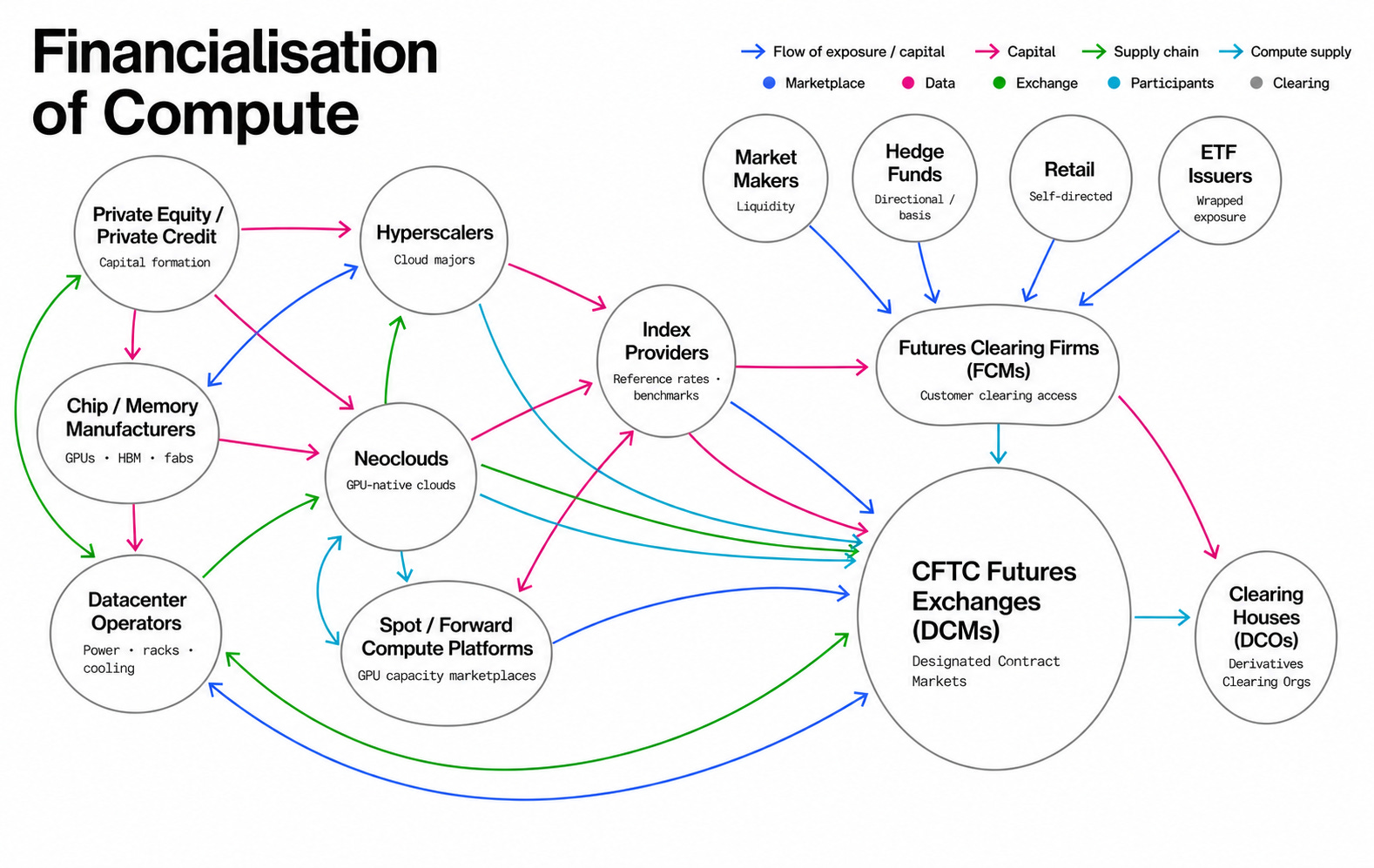

The Intermediary Stack

Once the pricing is in place, someone then has to sit between the GPU owner who wants to sell capacity and the AI lab that wants to buy it. In commodity markets, these middlemen are called dealers. Their job is to take a custom request on one side and match it with the available supply, by managing the price risk in between. In compute markets, the dealer layer has split into two tiers with completely different economics.

At the top, we have the hyperscalers who charge a hefty premium for immediate GPU capacity. For example, Google’s deal with SpaceX runs at $920 million a month for 110,000 GPUs; that pricing is roughly 4x what a typical neocloud will charge for the same 5-year contract. The premium is for getting the capacity now rather than in eighteen months.

Google needed capacity immediately to meet its surging demand for Gemini Enterprise while its own data centres were still being built, and that urgency is what creates the 4x premium. Only a handful of companies can serve this tier because offering large-scale compute on short notice requires owning the hardware outright, without carrying any debt against it.

Next below the hyperscalers, we have the commodity tier, where all the neoclouds and brokers compete on price. Neoclouds have to cover every cost from GPU-hourly revenue alone. This means everything from data-centre construction to daily operations, and for many of them, the unit economics just don’t work without raising additional capital.

Brokers, on the other hand, run live order books without owning any hardware. The biggest example of this currently is SF Compute, which manages over $100 million in GPUs and processes orders as low as $0.25 per GPU-hour from clusters that would otherwise sit idle.

And all the financial infrastructure being built today for Compute is to serve this same commodity tier. Because if you are Meta and your customer is Google, you don’t need a futures market or a clearing layer; Google’s credit is sufficient to make that deal happen. But if you are a neocloud borrowing against hardware that depreciates each year, you need to lock in revenue months in advance and prove that the hardware is performing as promised.

Once a trade is matched, there are two more things to take care of. First, someone has to guarantee that the trade will settle regardless of any party defaulting, which is what a clearinghouse does. Second, someone has to prove that the physical assets exist and are not encumbered. This is done through custody and verification. But in Compute, the clearinghouse does not exist yet because the futures themselves are not live.

For verification, we discussed in Part II how a unique cryptographic key can be used to prove that the chip is genuine. But since compute is a flow good, verification cannot just be a one-time inspection, as it is for metals. GPUs switch workloads every hour, so verification must also be performed continuously. This is why on-chain infrastructure becomes critical here: it allows the asset to self-report its status directly to the ledger, where it can be verified instantaneously.

At the bottom of all this is the Lending layer built around the same collateral bifurcation — whatever the lender actually underwrites as collateral is completely different depending on which tier the borrower sits in. With a hyperscaler, the lender is not really underwriting the GPU. It is underwriting the revenue contract behind it, which is essentially project financing. But with a Neocloud at the commodity tier, the lender doesn’t have that luxury. It has to underwrite the hardware itself and explain why you need everything else above in the stack being built.

Every commodity market that has gone through this cycle has eventually concentrated most of its durable value not in producing the commodity but in the companies that control the financial instruments around it. The oil majors built the wells and the refineries, but the exchanges and the clearing firms ended up with the better economics because they earn on volume and do not have to worry about the price moves.

Compute is still early in that transformation, building all of its financial infrastructure at once, some of it on traditional rails and some of it on-chain. The on-chain part comprises three distinct layers. First is pricing: on-chain transaction settlement makes benchmark data verifiable without trusting that the provider filtered the numbers correctly. Next is on-chain verification, which gives a shared ledger combined with the GPU’s own cryptographic identity, allowing it for continuous, real-time proof that the hardware is genuine and unencumbered.

And lastly, the settlement layer, where stablecoins are the only payment rail that works for AI agents buying compute per inference call, since it doesn’t require them to have a legal identity. At every other layer of this stack, the lenders and traditional infrastructure have an advantage.

That’s all for today!

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.