Hello,

Galaxy Digital’s crypto book continued to bleed through Q1 2026, but its operating businesses are beginning to detach from crypto cycles, and the company is betting that keeping them together is the right strategy. In Q1 2026, BTC price fell by more than 20% and ETH by ~30%. Yet Galaxy’s trading desk volumes held flat. That’s the first sign of Galaxy’s business decoupling from the market’s cyclical nature.

In previous analyses of Galaxy’s earnings, I argued that the Helios data centre could become its hedge against crypto cycles. However, that argument was forward-looking and conditional on the company sticking to its construction schedules and contracted cash flows that hadn’t yet started.

In April, Galaxy delivered its first data halls in Texas to CoreWeave and is showing signs of diversifying its overall business towards the high-margin, non-cyclical nature of the data centre business. Although its revenue from the data centre business is insignificant, expect its financials to start looking different starting Q2 2026.

In today’s analysis, I will show you how Galaxy plans to evolve its two businesses together rather than split them, and how that will help the company achieve the stability few others can boast.

TL;DR:

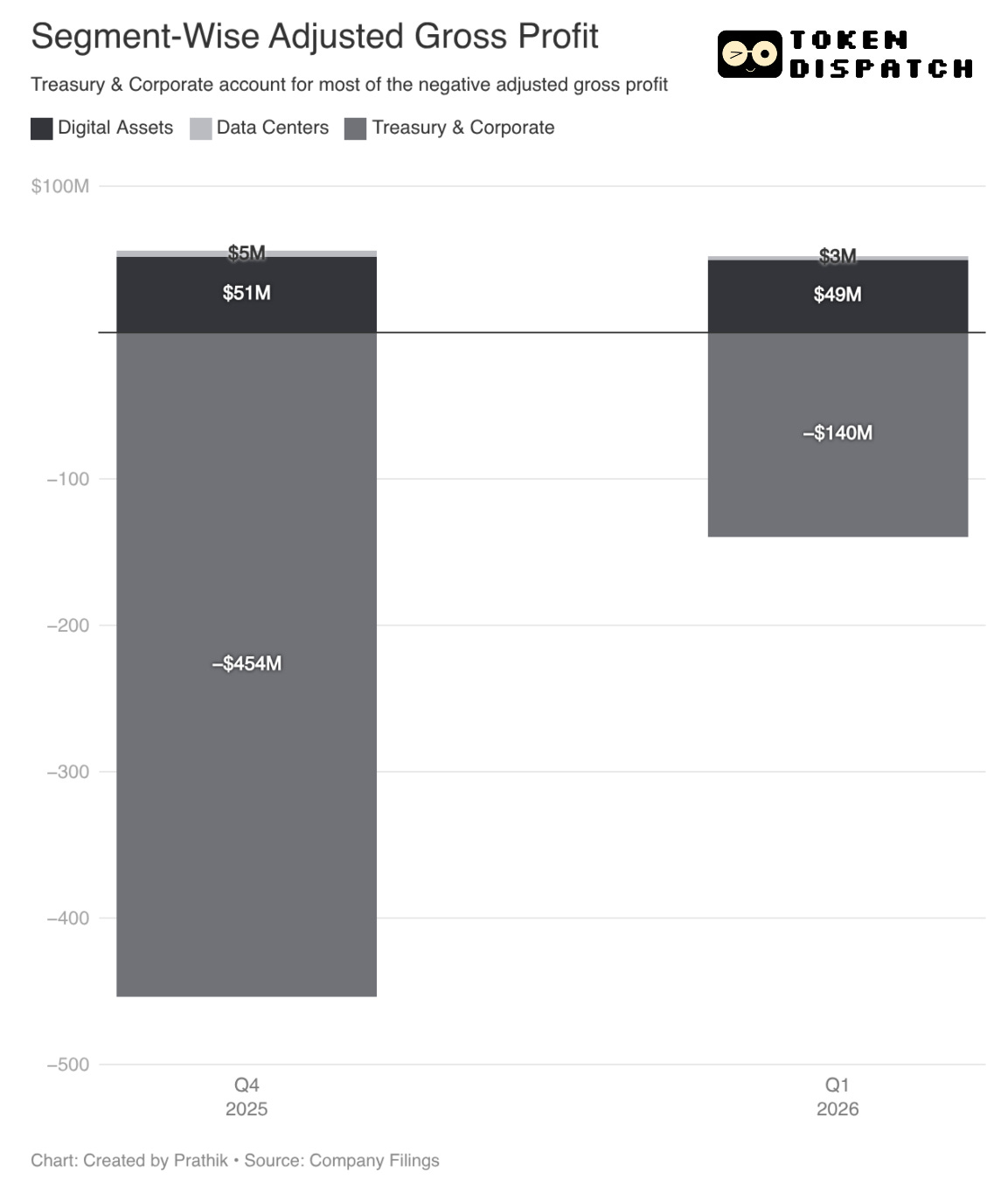

Galaxy’s Digital Assets segment delivered $49M in adjusted gross profit, roughly flat with Q4 ($51M), even as crypto prices dropped by around 25%

Trading volumes at Galaxy held steady while industry-wide volumes declined by more than 20%

Helios delivered its first data hall to CoreWeave, shifting from construction milestone to operational revenue

The First Correlation Crack

Galaxy’s financials still look like those of any other crypto company. Its Q1 adjusted EBITDA of negative $188 million was almost entirely driven by adjusted gross loss of $140 million in the Treasury & Corporate segment. Most of that loss was attributable to unrealised markdowns on its net digital asset exposure. Galaxy trimmed down its digital assets position to $667 million as of March 31, 2026, down 27% from $920 million at year-end.

The Digital Assets segment, which facilitates crypto trades, lends, manages assets, and builds infrastructure, earned $49 million in adjusted gross profit. That was nearly identical to Q4’s $51 million, despite higher crypto prices in that quarter. Lower prices hurt Galaxy’s business by driving away participants and drying up trading volumes. This also shrinks the loan collaterals on which Galaxy earns interest.

Activity in Galaxy’s trading desk also reinforces this trend. It processed roughly the same volume quarter-over-quarter while total industry trading activity contracted by more than 25%.

But what’s holding up Galaxy’s operations during a market meltdown?

The Stable Pillars

Diversifying its risk by expanding its product and client base has been Galaxy’s secret to staying afloat while its peers face the wrath of the market meltdown.

It spent the past 18 months layering fee-based and recurring revenue onto its trading desk. Asset management recorded $69 million in net inflows, although the AUM fell to $8 billion from $11.4 billion due to mark-to-market revaluation of existing holdings. Shortly after the quarter ended, Galaxy also secured a $75 million single-client mandate, one of the largest in its history. Galaxy added new clients and diversified its counterparty base despite the lending book shrinking by 20% due to depreciation in crypto prices and natural loan roll-offs.

In May, it will launch a fintech hedge fund that will invest in companies building tokenisation rails. It will also open its consumer-facing trading app, GalaxyOne, to businesses and allow institutions to trade, manage digital custody, finance, stake, and access crypto research. Both these ventures are expected to generate recurring revenue regardless of where Bitcoin or any other cryptocurrency trades.

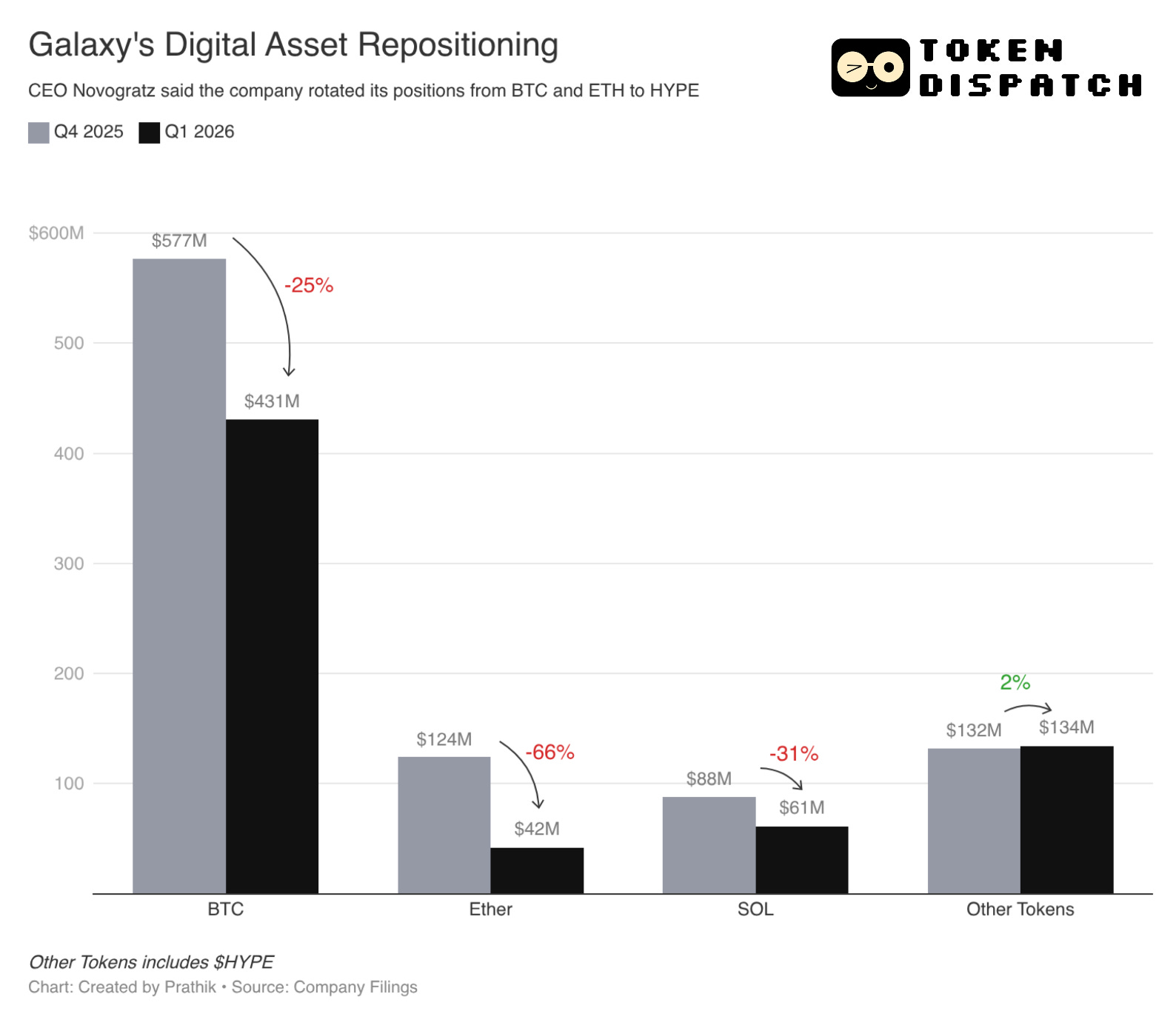

The second move is strategic positioning.

Galaxy trimmed its Bitcoin exposure and rotated a significant portion of its balance sheet into Hyperliquid.

This rotation helped the balance sheet outperform what a pure beta position would have delivered.

But the biggest takeaway for Galaxy’s investors and analysts will be that the lights are finally on in Texas.

Lights, Camera, Data Centres

Galaxy’s Helios data centre site delivered its first set of halls to CoreWeave in Q1, which is expected to bring $1 billion in annualised revenue at full-capacity deployment by 2028.

Read: Galaxy Builds Beyond BTC

What was once planned as a Bitcoin mining site has been converted into a functioning AI data centre with live power distribution, cooling, and network connectivity.

Although the revenue from the data centre business was modest at $3 million, the company has stayed on schedule for its 133-megawatt Phase 1 launch. There are three aspects that I am most excited about in this business segment: the margin, the lack of seasonality and the contract length. These are 15-year contracted cash flows at approximately 90% lease-level EBITDA margins. When Phase 1 ramps fully in H2 2026, proportionate estimates suggest $250 million in annualised revenue entirely uncorrelated to digital asset prices.

For context, the Digital Assets segment generated $49 million in adjusted gross profit this quarter. That’d add up to $200 million in annualised revenue rate (ARR). Helios’ Phase 1 alone would generate more operating profit at $250 million in ARR and 90% EBITDA margins.

Galaxy has also secured approval for an additional 830 MW capacity from the Electric Reliability Council of Texas (ERCOT).

The company is in active conversations with additional tenants beyond CoreWeave regarding this expanded capacity. But why chase new tenants?

Galaxy doesn’t want to repeat the mistake of over-reliance on a single business or a single client. That’s probably why its president, Christopher Ferraro, wants the company to focus on a multi-tenant, multi-campus strategy.

But how will it fund these multiple sites, each requiring capital-intensive computing power, cooling equipment, and other infrastructure?

At Phase-1 of the Helios data centre, CoreWeave’s end customer using the GPUs is a multi-trillion-dollar investment-grade public company. This credit quality flows down to Galaxy’s financing terms for its future data centre projects.

Galaxy Dual Business Mode

Galaxy Digital’s two businesses are evolving with different capital needs, earnings profiles, and visibility. They seem to add little synergy and have no apparent reason to be run under the same entity. So, why not split them?

The company isn’t convinced that the segments will stay uncorrelated.

Most will see Galaxy as a simple crypto company about to spin off a data centre. But they miss out on the link that connects its crypto trading and data centre operations. When Galaxy’s data centre segment generates a billion dollars in annual revenue at 90% EBITDA margins, it can afford to run a crypto infrastructure business through bear markets without flinching.

While the data centre covers the fixed costs, the crypto business provides upside when markets turn. In that model, Galaxy’s cost of capital across both businesses falls because each one de-risks the other. The crypto business doesn’t need to generate enough margin to survive a downturn on its own. It can help the business stay afloat, as it did in Q1 2026, if it just covers its variable costs. The data centre can work independent of token prices, as it gets its demand from hyperscalers rusing to lock up computing power. But sharing balance sheet with a cash-generating crypto business gives Galaxy flexibility to self-fund early-stage development costs and move faster on new sites than a standalone data centre startup could.

None of this is conclusive. It’s the first quarter that gave signs of decorrelation as an observation. For it to be a pattern, the thesis needs to hold across the next 2-3 quarters.

What cannot be debated, though, is that the structure Galaxy is building is in the right direction. While its data centre business offers high-margin, contracted, predictable income, its trading segment offers low-margin, high-volume, cyclical crypto trading.

Three more quarters like this one, and Novogratz says he’ll celebrate.

That’s it for this week’s quantitative analysis. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.