Value creation and value capture are two different things. Value creation is making something the world needs. Value capture is keeping some of what the world pays you for it.

Most of the time, the two are assumed to go together. You build something valuable, you charge for it, you keep a portion of what you charge. This is the normal shape of a business.

What is less often discussed is how many of the most consequential companies in history spent their formative years aggressively creating value and systematically refusing to capture it. They gave the product away, or nearly away. Their entire claim to eventual profitability rested on one assumption: that distribution would one day convert into pricing power. Sometimes it did.

AWS ran for years at effectively no margin while Amazon figured out that nobody would want to rip out their cloud infrastructure once it was embedded. Stripe processed billions in payments before it became undeniable enough to start layering in new products at healthy margins. Yes, we are going back to the zero-capture conversation.

That has generated $256 million in fees and kept almost none of it, because the infrastructure trap makes charging feel dangerous once enough institutions have built on top of you. It did not choose to give the money away.We pick up where last week’s piece on Morpho left off — a protocol

Read: Morpho Is Becoming the Backend

When does the distribution convert? When does giving away the value stop and capturing it begin? Most companies that play this game successfully have a clear answer. The ones that do not have a clear answer have an interesting problem.

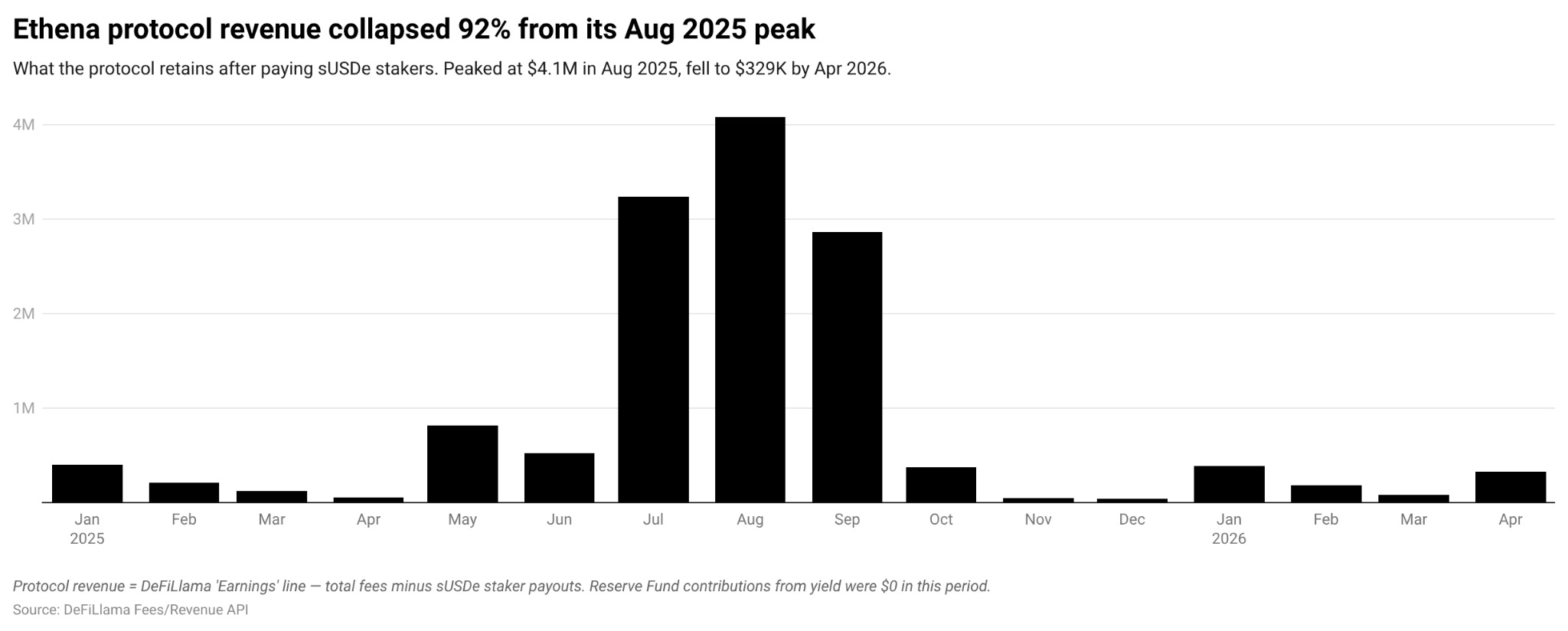

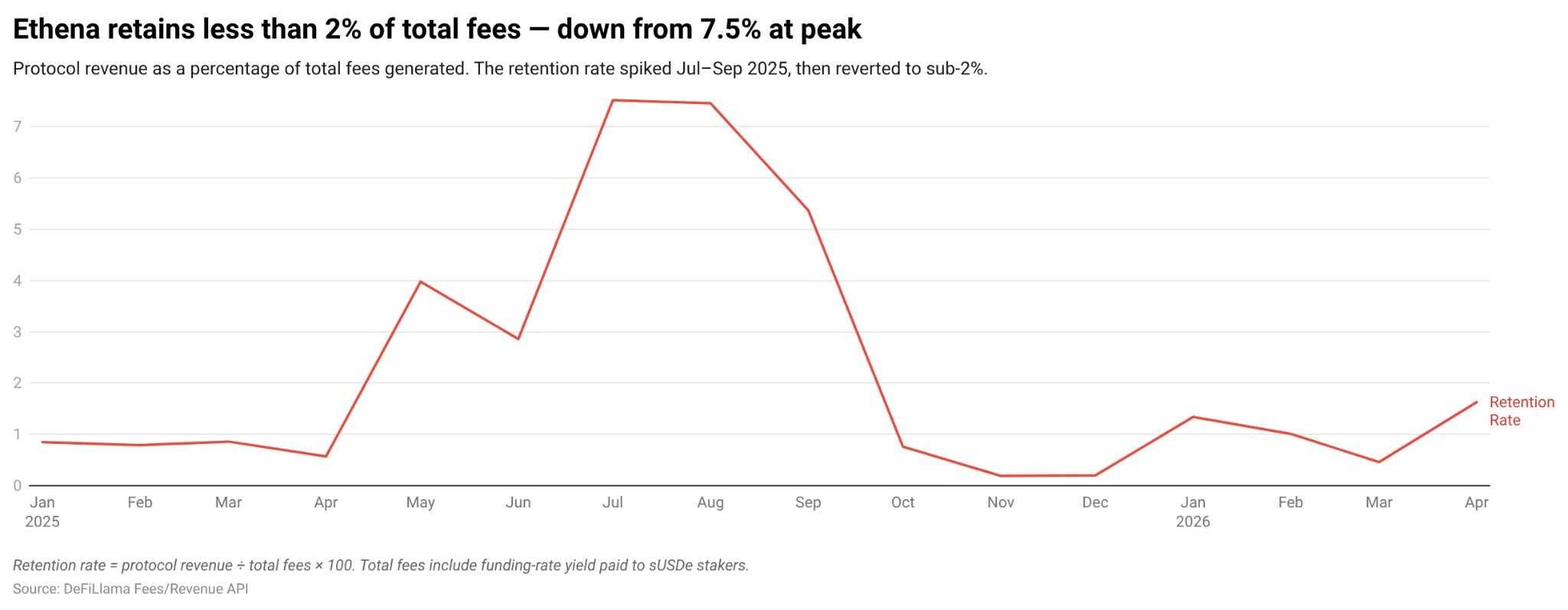

Ethena is now in that conversation. It has built the third-largest stablecoin in the world. Of the $470 million in fees collected over sixteen months, the firm retained $13.8 million, representing a 2.93% retention rate. Every hundred dollars the protocol generated, it kept three. The rest went to sUSDe holders as yield, by design, on purpose, as the product. Ethena doesn’t have the same problem as Morpho; this one is different.

That’s what we’ll unpack today.

Starting with what Ethena built, USDe is a synthetic dollar that holds no bank reserves. Instead, for every dollar of USDe minted, Ethena holds crypto collateral and opens an equal short position in perpetual futures. Long spot, short perp, net position stays approximately flat regardless of what Bitcoin does. Paid by long traders to short traders in perpetual markets, ETH staking rewards on collateral, and interest on liquid stablecoins held as backing. That yield goes to sUSDe holders, people who stake their USDe to earn the protocol’s income. Ethena keeps a small slice for a reserve fund and some mint and redeem fees. Everything else flows through.

Read: When the Yield Runs Out 💵

In 2024, when funding rates averaged between 8 and 11% annually, the protocol was new, and everyone was bullish, and perpetual traders were paying generously to maintain leveraged long positions. This was a very good deal for sUSDe holders. Average APY was 18%. USDe grew from zero to $6 billion in ten months.

By August 2025, Ethena was generating $54.7 million a month in total fees and keeping $4.08 million of it. Peak protocol revenue. Everything looked like it was working.

Then October happened. The October 10 crash was the largest single-day liquidation event crypto had seen in years. Over $19 billion was wiped out in leveraged positions. USDe briefly lost its dollar peg on Binance before recovering within hours. That part gets reported. But what was sitting underneath the stablecoin when the market lurched?

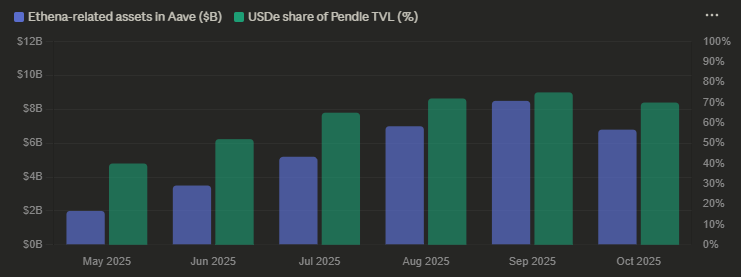

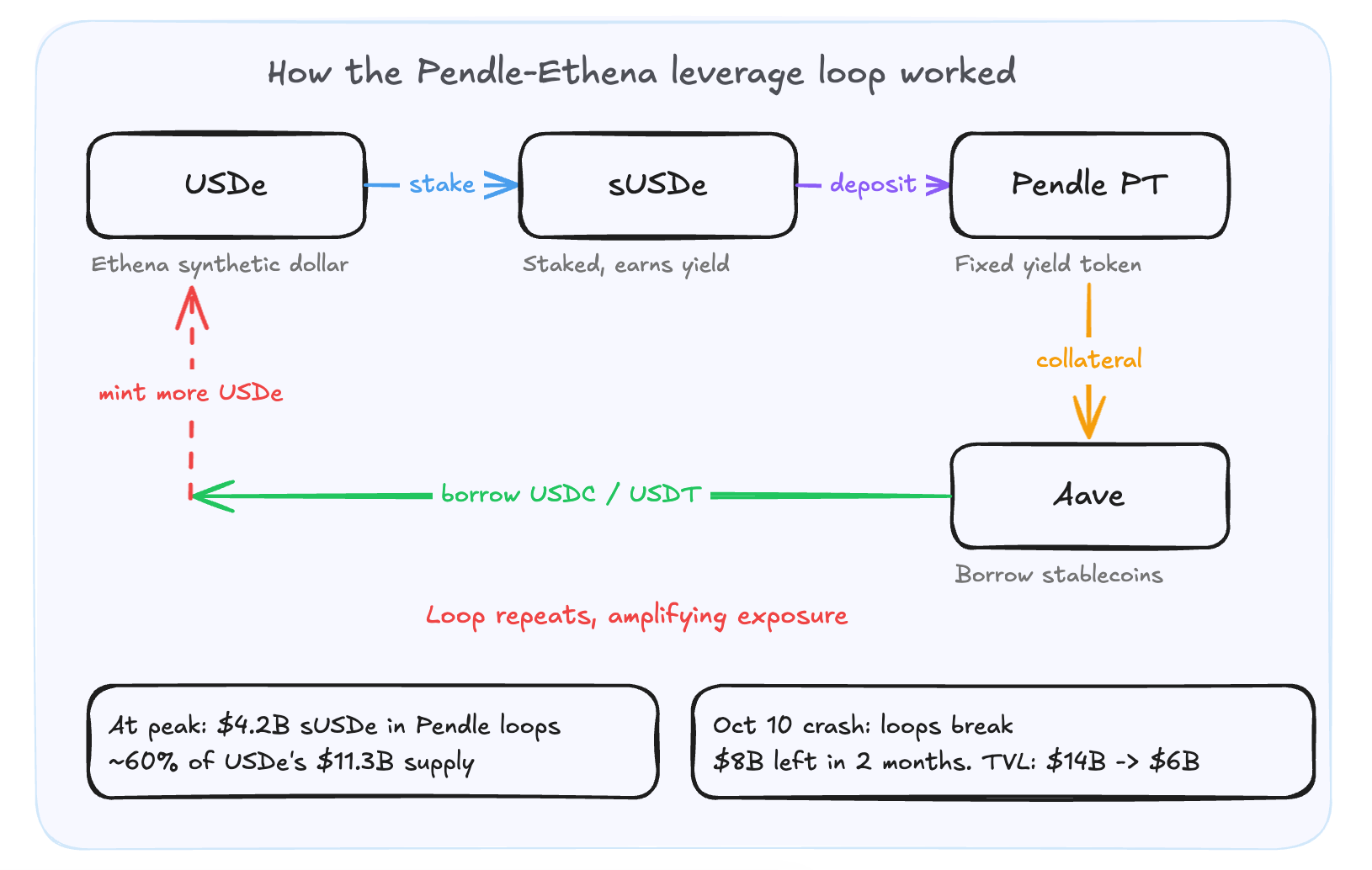

At peak, over $4.2 billion of sUSDe was locked in Pendle, representing roughly 60% of USDe’s $11.3 billion supply. Structured yield products that let users lock in fixed rates on sUSDe and borrow against those positions on Aave.

These were yield tourists running leveraged carry trades, extracting the maximum possible return from sUSDe’s high APY, and holding nothing when the trade unwound. When October happened, the loops broke. $8 billion left in two months. $5.7 billion in October alone.

The people who stayed were not running leverage. The staking ratio (the percentage of USDe held as sUSDe) went from roughly 60% at peak to approximately 47% in early 2026. The proportional loyalty barely moved. In absolute terms, staked supply went from $8.4 billion to $3.3 billion because the underlying supply collapsed. But the holders who remained held. The people who wanted a yield-bearing dollar stayed, while the yield tourists left.

But Ethena lost its distribution strategy in October.

The protocol passes almost all yield to sUSDe holders and retains only mint and redeem fees, which is a fraction of total activity. Ethena generated $65 million in total fees in Q1 2026 alone. Its net profit for the quarter was $614,000. Tether made $5.2 billion in the same period. Both are called stablecoin issuers. But that’s a different story. The Gross Protocol Revenue figure is not what Ethena keeps.

At the start of 2025, perpetual futures accounted for 93% of USDe’s backing. As of early 2026, perps are 11% of backing, with 89% in liquid stablecoins and lending positions. Ethena has converted from a delta-neutral trading operation to something that looks considerably more like a T-bill wrapper distributing Treasury yields to sUSDe holders. The yield it offers (approximately 3.5% as of early 2026) is now comparable to that of a decent money market fund, without the complexity of delta-neutral hedging. The backing composition has shifted.

At 18% APY, sUSDe offered something USDC did not. At 3.5%, the difference is smaller, and the complexity of the underlying mechanism starts to look like a liability.

BaFin’s March 2025 ruling classified it as an unregistered security, forcing Ethena’s German entity to wind down and giving EU holders 42 days to redeem. Ethena later confirmed that Ethena GmbH had no whitelisted users or direct customers at the time the ban took effect, and that most USDe was issued outside Germany before MiCA took effect. Rather than capital flight from the EU, the primary driver was the unwinding of Pendle loops.

The Fee Switch Problem

Ethena plans to activate a “fee switch,” which redirects 10% to 20% of the protocol’s earnings away from sUSDe holders (users) and toward sENA stakers (token holders).

The waterfall is structured. The reserve fund gets topped up first, and sUSDe must maintain a yield the Risk Committee deems competitive — only the revenue remaining after those two conditions clear flows to sENA stakers. The Risk Committee retains discretion to set and adjust the benchmark, which means there is no hard floor that can be cited with precision until the governance vote finalises.

ENA stakers only get the leftovers.

Currently, because market interest rates are low, there is no profit left over. There is no money to move.

The fee switch takes from the same pool that feeds the sUSDe yield. At peak revenue and a 15% funding rate, a two-percentage-point reduction in sUSDe yield makes no difference. At current rates, when sUSDe sits at 3.5% and the benchmark sits around 4.5%, the hurdle protection kicks in, and nothing is distributed to ENA stakers.

Ethena needs higher funding rates to generate revenue that makes the fee switch worth activating. Higher funding rates stem from a bull market in crypto derivatives, the same condition that made Pendle loops possible and created the $8 billion outflow. The monetisation strategy and the stability risk run on the same fuel.

Tether’s theory is that trust is built through institutional permanence. If you have been here long enough, have survived enough cycles, have never lost a dollar, they will hold your stablecoin because the cost of doubting you is higher than the cost of staying. Tether keeps everything. Its holders know this. They stay because the alternative is uncertainty, and uncertainty is expensive. This is loyalty built through a track record.

Loyalty built through alignment. In this model, the holder who receives the yield and the protocol that generates it are on the same side. There is nothing to trust because there is nothing hidden. Ethena’s theory is the opposite. If you align your interests completely with your holders — pass them the yield, keep almost nothing, make your success and their success the same thing — you build a different kind of loyalty.

The problem with the alignment model is that it cannot survive the moment the protocol needs to capture value for itself.

When the protocol begins capturing value for itself, the relationship shifts from shared success to a standard transaction. Holders who stayed because their interests were identical to the protocol’s will find that alignment severed. This transition reveals whether users believe in the product or simply tolerate the mechanism for its returns. Tether avoids this conflict because it never claimed to be on the same side as its users. The fee switch threatens this alignment.

Ethena built a system that relies on faith, and the fee switch determines exactly how much of that faith remains.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.