Hello,

Stability can be a mirage. This is often true in finance. You bet on a boring financial instrument thinking it’d offer you steady, reliable returns. It does stick to the template until the underlying fundamentals wobble. These ‘steady bets’ are often more deceptive than the speculative ones. People expect the latter to be risky anyway. But few expect that to happen with steady, boring bets.

We saw this play out about 75 years ago.

In the 1940s, dollar-denominated deposits accumulated in European banks following the Great Depression and World War II. These allowed account holders to hold U.S. dollars at non-U.S. banks as a hedge against local currency devaluation. They offered attractive yields and led to some out-of-the-box thinking. Some account holders, like American companies, got creative by parking dollars abroad to dodge capital controls at home.

The European banks welcomed them all. They accepted these deposits and lent them further at higher interest rates. The glut of these deposits in Europe led to the Eurodollar market, a parallel dollar system that was not regulated by the U.S. Federal Reserve. Things began to unravel as the Cold War started in the late 1940s. More people started demanding their U.S. dollars back, but the banks didn’t have enough physical dollars on hand. The entire cycle crashed.

We see a similar trade happening now in the stablecoin market. Except that the digital dollar issuers seem to have learned from history.

In today’s deep dive, I will explain whether Ethena’s reliance on traditional equity markets can save its stablecoin reserve strategy.

The Initial Act

In early 2024, Ethena launched USDe as a synthetic stablecoin that was different from the rest. USDe was issued as a dollar-pegged asset without actually holding dollars in bank reserves. Instead, it held crypto assets like bitcoin and ether, for every dollar of USDe minted. Simultaneously, it shorted an equivalent amount of crypto futures.

The two positions balanced each other. If BTC goes up, the short position on futures loses what the spot gains. And vice versa. Eventually, the USDe was always worth $1, even without an actual physical dollar in the bank account.

But why should people hold USDe over incumbent cryptocurrencies like USDT orUSDC? They were rewarded for doing so.

The incentive was tailor-made to align with how crypto derivative markets are wired. In a bull market, more traders bet on prices rising. Exchanges charge those bullish bettors a small continuous fee, called the funding rate, and pay it to whoever is on the other side. Ethena was permanently on the other side. It collected those payments and passed them on to USDe holders as yield.

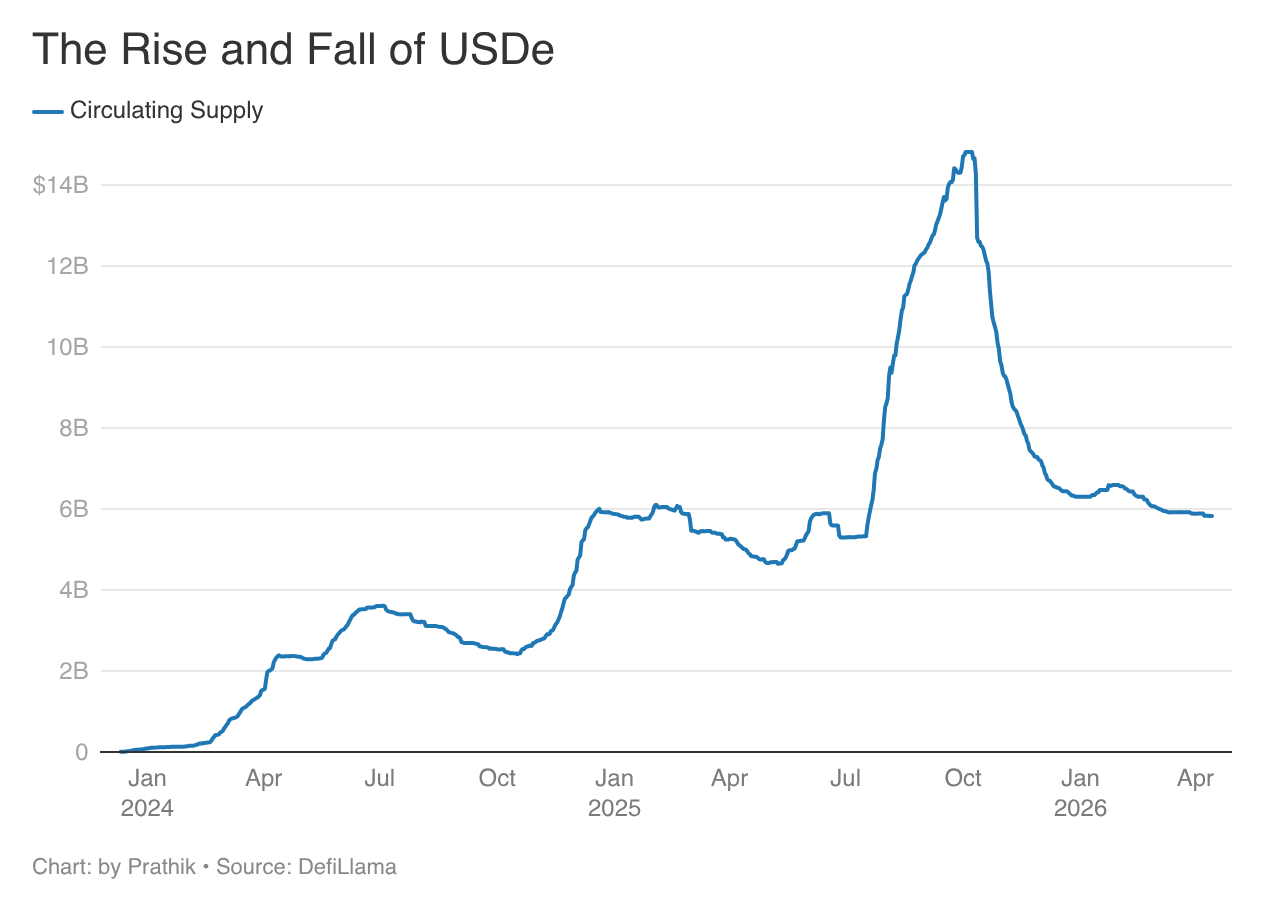

At its peak, the yield crossed 20% annually. In 18 months, USDe’s circulation grew sevenfold to approximately $15 billion, the fastest growth ever recorded by any stablecoin.

Read: The Ethena Speed Run 🏎️💨

I loved the design, except that it was heavily reliant on the crypto markets holding the status quo. It worked in bull markets because they were getting paid for being a minority holding a short position against a majority that were long. But markets flip with time; they always do. When they did, the cracks appeared. On October 11, a day after the largest crypto liquidation wiped out over $19 billion, USDe briefly lost its dollar peg. Ethena’s synthetic stablecoin fell to 65 cents against the dollar on Binance.

USDe’s circulating supply fell from about $15 billion to under $6 billion over five months, starting on October 10.

A Lesson Learned Too Late?

More than $9 billion was redeemed. Perpetual futures, which once accounted for almost 100% of the model’s reserve backing, now represent only 11% of it. The bigger irony is that all of this was avoidable. Ethena should have seen it coming.

The signs were telling. Markets always move in cycles, and crypto was no exception. We have seen it over the past 16 years. A reliance on a single collateral source via perpetual futures, which was closely tied to market movements, was always a ticking bomb.

Even other stablecoin issuers had begun adapting. As the U.S. Fed started reducing interest rates, the top two stablecoin issuers increased their activity to supplement their reserve income. Tether diversified its reserves by adding record levels of gold to its coffers. Circle, the USDC issuer, has been aggressively building its infrastructure revenue stream through Arc, its Layer-1 network, and the Circle Payments Network, a full-stack internet payment system.

But Ethena was slow to act. The slide would have been worse had it not addressed the situation at all. That’s not my observation, but what its founder, Guy Young, admitted in a post on X.

Guy also listed out the measures Ethena has started taking to adapt to the regime change.

The TradFi Fix

Ethena would expand its collateral base to include equities and commodities basis trades, overcollateralised institutional lending, prime brokerage services, and a broader set of real-world assets (RWAs).

Ethena started as a crypto-native synthetic dollar, unlike pioneers like Tether’s USDT and Circle’s USDC, which back their digital dollars by holding physical dollars or equivalent treasury bills in their coffers.

Life has come a full circle for Ethena. It’s now going back to wiring itself into the traditional finance infrastructure to keep paying yield to its holders. And not one, but multiple such sources.

With an equities-basis trade, it pockets the gap between buying spot S&P 500 exposure today and simultaneously shorting its futures. The same strategy that Ethena used with BTC and ETH earlier. That’s a small, but predictable return that is independent of crypto market movement.

Now imagine Ethena following a similar trade across multiple asset classes: commodities such as gold, silver, wheat, and oil, indices, lending markets, and more. Every asset will have a spread that is driven by market supply and demand dynamics. Ethena can run delta-neutral trades across all of them and collect spreads around the clock, regardless of what retail feels about crypto or Bitcoin.

While this reduces dependence on crypto markets, it now moves in line with equity, commodity, or other asset markets. Each time volatility in these markets spikes and liquidity in futures markets dries up, these strategies could also fail. It could squeeze USDe’s revenue further.

But that pessimism is the same as expecting a portfolio well-diversified across asset classes to fail. It can still happen, sure, but it’s rare. Yet that’s how the finance world works; on probability and math. People don’t diversify their portfolios expecting to see a green balance when the entire market is drowned in red. The expectation of diversification is to reduce the likelihood and intensity of losses.

For Ethena, diversifying across uncorrelated yield sources will do the same thing. It will reduce the likelihood that its yield will be squeezed out completely when either one or two of these asset classes underperform.

The Liquidity Test

Ethena’s diversified strategy is the logical solution to tackle market cycles. Spreading exposure across equities, commodities, credit and crypto makes the income stream more resilient. That’s probably the only edge it will have over a T-bill-backed USDT and USDC, which pays its holders no yield.

But the new strategy still faces a strong headwind.

The liability side of USDe is fully liquid, meaning any holder can redeem it at any time. But the assets generating the yield are not perfectly liquid during periods of stress. Equity basis positions could take time to unwind cleanly. Institutional loans have fixed tenors. Collateralised Loan Obligations are not always liquid in choppy markets. This gap between liquid liabilities and imperfectly liquid assets can become a structural tension for any yield-bearing stablecoin. It’s a gap that even a diversified yield strategy can’t fix.

In calmer markets, different asset classes can move to different signals. Gold moves up on inflation fears. Good earnings drive up equities. A geopolitical crisis involving oil-producing nations can inflate oil prices, as we are witnessing now. Crypto funding rates are high because retail is bullish.

But that’s not how they move in extreme stress scenarios. The correlation assumptions can fall apart, cancelling out the diversification advantage. The common denominator tying all these assets is liquidity.

And when things go south across the board, everyone wants to cash out of their positions.

Harry Markowitz won the Nobel Prize for showing that diversification reduces risk. Yet, the 2008 crisis needed no Nobel Prize to show us an anomaly to Harry’s Modern Portfolio Theory (MPT). Academician Nassim Taleb had argued the same in his book The Black Swan. The contention is that correlation is not a constant property of asset pairs. It’s a variable that changes with market conditions.

Despite all these anomalies, it’s important to recognise that these are black swan events that are unavoidable and rare. There’s little anyone can do to predict or control them. A diverse portfolio across asset classes is still likely to outperform a concentrated portfolio reliant on one single asset class. We saw it happen during the money market meltdown in 2008.

The Reserve Primary Fund held short-term corporate debt instead of Treasury bills because the spread was attractive. When Lehman Brothers failed, that paper became worthless overnight.

Overcollateralisation of loans is one of Ethena’s responses to this. If borrowers post more collateral than they borrow, losses are theoretically absorbed before they reach USDe holders. But overcollateralisation ratios are calibrated to historical volatility ranges. Stress events can spill outside those ranges.

No strategy will be free from risk. Ethena’s task will be to inspire enough confidence in investors to believe that its new, diversified strategy is better positioned than the earlier model , which depended on a single crypto market dynamic.

That’s it for today. I will be back with another deep dive.

Until then, stay curious!

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.