Hello,

After the 2008 financial crisis, banks pulled back from middle-market lending. Private credit filled that void with pooled capital from pension funds, insurers and wealthy individuals, and lent it directly to borrowers. The private credit industry grew almost tenfold from 2007 to approximately $2.4 trillion by 2023.

The problem, though, has been that these lenders retained all of banking’s frictions. Think of the multi-day settlement windows, agent banks reconciling positions over email, and the “2 and 20” fee model that survived intact.

The new system is larger than the one it replaced, but also more susceptible to risk due to its high leverage.

The stress is already showing. In Q1 2026, redemption requests at non-traded BDCs exceeded new fundraising for the first time in the sector’s history. Blue Owl had to sell $500 million in bonds and restrict redemptions across its retail vehicles to address rising redemption activity. Blackstone’s flagship BCRED fund has already received $4.4 billion in redemption requests in the second quarter, accounting for 10% of its outstanding shares, compared with 7.9% in the preceding quarter. Capital is moving from smaller, software-heavy lenders to larger balance sheets. Ares Capital and Blackstone’s BXSL have held up. The rest are bleeding.

Blockchains can help address some of these frictions, and the world has begun to take notice.

In January this year, Apollo, the world’s largest private credit manager, put a slice of its diversified credit fund on six blockchains. The product, ACRED, settles redemptions daily. The traditional version settles quarterly, on paper, through a transfer agent.

In today’s edition, I look at how private credit’s $2.4 trillion empire is being rewired and who gets to capture the value from the new infrastructure.

Onto the story,

Prathik

What Concerns Private Credit?

After the 2008 financial crisis, regulatory guardrails were put in place to protect the banking industry from future financial shocks. The Dodd-Frank regulation in 2010, the Volcker Rule, and Basel III’s capital framework required banks to hold more capital against leveraged loans, while interagency guidance discouraged such deals.

The lending business is dominated by half a dozen key players. Apollo manages over $1 trillion in assets, with ~80% in credit. Ares has $422 billion in AUM. Blackstone’s Blackstone Private Credit Fund (BCRED) holds roughly $79 billion in assets. Blue Owl manages roughly $160 billion

Most of these institutions retained the old “2 and 20” fee structure, in which the banks charged a 2% management fee on AUM and a 20% carried interest above a predetermined profit threshold.

The mechanics behind processing a direct lending transaction are worse. The Loan Syndications and Trading Association (LSTA) targets seven business days to settle par syndicated loans and twenty for distressed loans. In reality, it often takes longer due to time-consuming paperwork.

In its market practice documentation, the International Securities Association for Institutional Trade Communication (ISITC) calls the process “highly manual (fax, email).” NAV calculations are performed quarterly by fund administrators, who are paid specifically for this.

At some levels, this system looks worse than the 2008 banking system. In 2008, the failing assets on bank balance sheets were backed by FDIC insurance. The US Fed’s emergency liquidity facilities (TAF, PDCF, TALF) plus TARP capital injections were available as the last resort. The problematic securities were still being traded, so the market priced in the stress as it unfolded.

Today’s private credit risk is entirely different.

The IMF’s October 2025 Global Financial Stability Report flagged that more than 40% of companies that borrowed from private lenders had negative cash flow from operations at the end of 2024. US life insurers are roughly 33% allocated to private credit.

This is the core problem that worries the private credit industry today. The system that replaced banks is bigger than the banks it replaced, more leveraged to insurance capital, and yet regulators have done little to change it.

Moving the Plumbing On-Chain

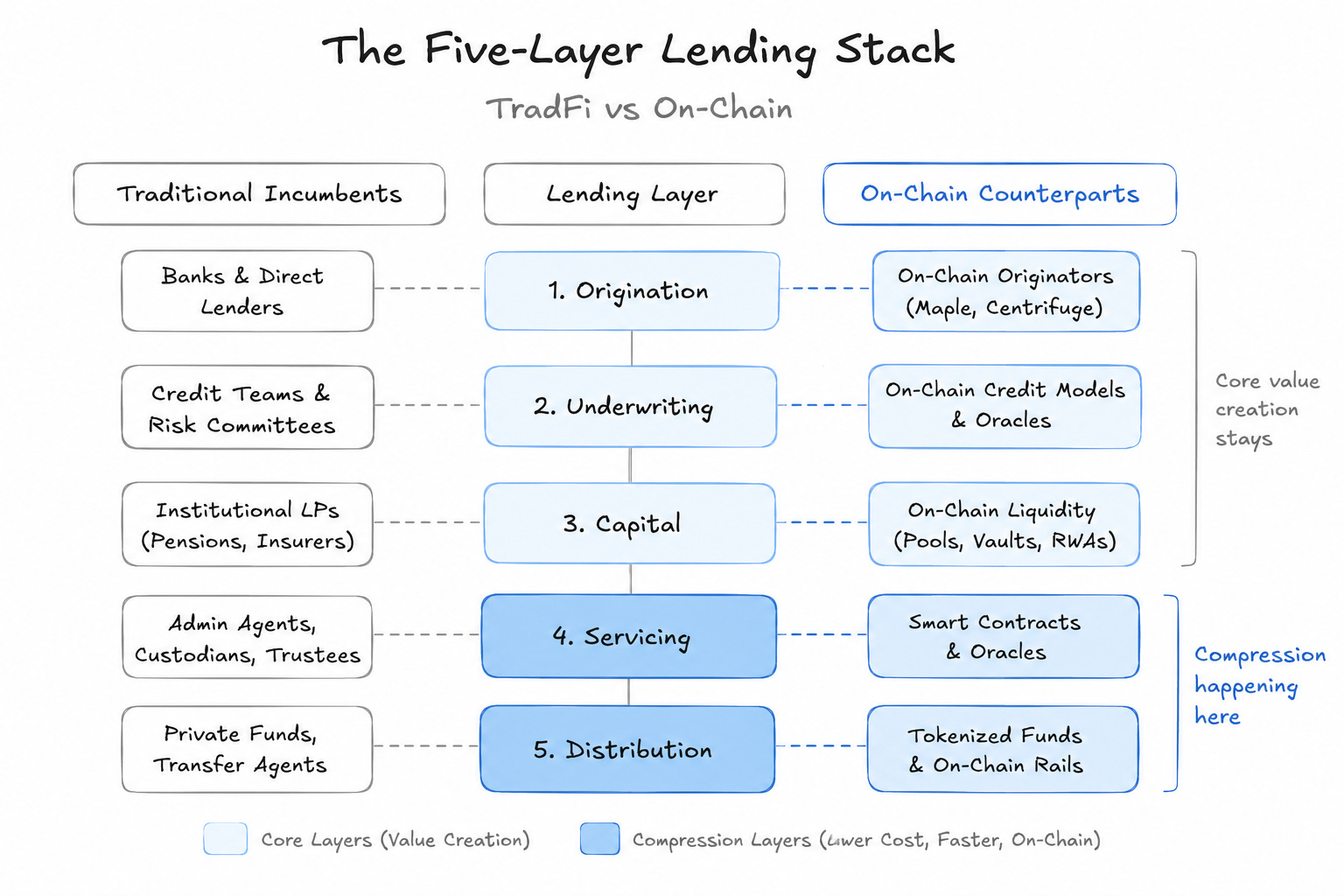

Lending has five layers: origination, underwriting, capital, servicing and distribution. A private credit fund collects a single fee for doing all five. Blockchains force them apart. Once they’re apart, you can see which ones still earn their fee.

Consider Maple Finance, an on-chain asset manager. Maple started five years ago as an undercollateralised institutional lender on-chain. When FTX collapsed in late 2022, so did Maple. Its largest borrowers walked away from loans they couldn’t repay. Active deposits fell by over 90% in a matter of months.

But Maple rebuilt. It brought underwriting in-house, tightened collateral and disclosure rules, and put walls between pool delegates and borrowers. By the end of 2025, it had originated over $20 billion in loans on-chain, with withdrawals settling in under five minutes.

Compare this with a 20-business-day window in the traditional market. Maple’s rise from a near-death experience shows that on-chain lending is not necessarily fragile. If on-chain lending adopts the same institutional safeguards as traditional credit, a robust model is achievable. Maple showed this by rebuilding its underwriting layer while skipping the agent bank, correspondence via fax or email, and the 20-day wait.

Securitize is experimenting at the distribution layer. Its tokenised feeder for Hamilton Lane’s Senior Credit Opportunities Fund cut the minimum investment from $2 million to $10,000. That opens up lending opportunities to a much wider range of investors. The product still requires a qualified purchaser status, but the operational cost of qualifying has been compressed.

In traditional rails, a private credit position is an inefficient, passive position on the balance sheet. The company holds it to maturity, sells it at a discount, or worse, pledges it through paperwork that could take weeks. On Aave’s Horizon, a private credit position can be used as live collateral. An institution can borrow stablecoins against it on the same day. This is because NAV updates flow through an oracle without waiting for an agent bank to apply them manually once a quarter.

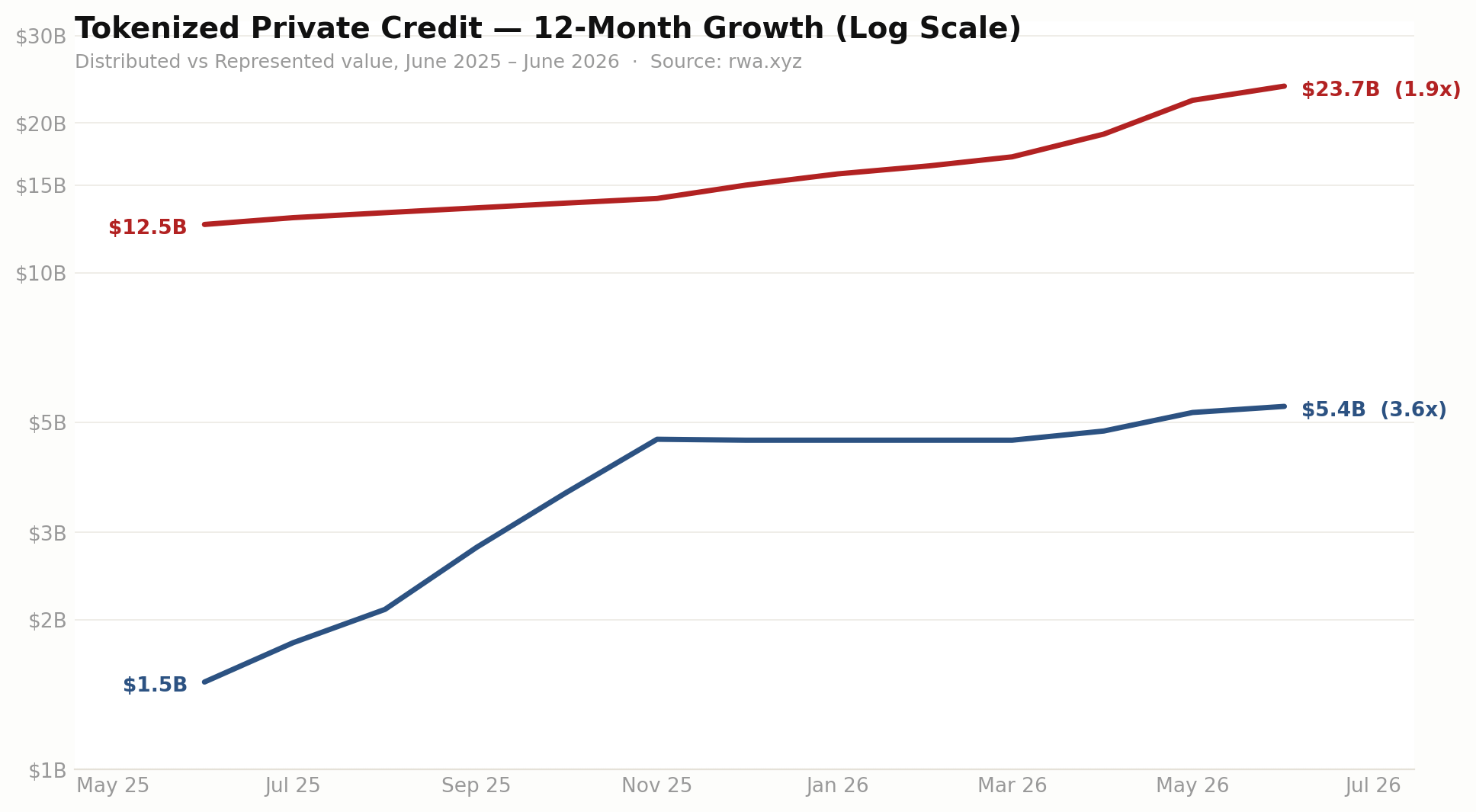

There’s one caveat to all this, though. Most institutional tokenisation today is just a wrapper around traditional permissioned rails. Only two out of every 10 dollars in tokenised credit is distributed through blockchains. The remaining eight dollars is represented and recorded on-chain only for reconciliation, but is distributed using traditional lending mechanisms.

But the trend over the past 12 months indicates that the proportion is increasing rapidly. While the represented value of tokenised credit doubled in the last year, loans originating on-chain more than tripled, from $1.7 billion to $5.3 billion.

Capturing Value On-Chain

For decades, banks charged fees for ‘features’ that should have been considered as frictions. Think of the time-consuming paperwork, 20-day processing windows and the human labour involved to manoeuvre all the procedures. Blockchains promise to eliminate most of these frictions. So, where will the lending protocols earn from once blockchain commoditises the lending infrastructure?

Consider Charles Schwab, the financial services and brokerage firm. For decades, Schwab undercut every full-service brokerage in the US on trading commissions. Eventually, it charged nothing at all. Yet, Schwab didn’t get poorer. It made money elsewhere. Revenue from commissions got replaced by net interest income on idle customer cash.

BlackRock built a trillion-dollar empire on this very trade. The asset manager built Aladdin as the tech platform that unifies the investment management process. This platform became a moat for BlackRock.

In private credit, too, Apollo’s relationships, Ares’ workout expertise, and Blackstone’s deal flow remain unique to each firm. No matter what aspect of private credit tokenises, these aspects won’t. Blockchains unbundle different layers of lending. So protocols that can bundle these layers on-chain by vertically integrating across the stack can capture maximum value across the lending infrastructure.

Securitize is mimicking what transfer agents like SS&C Technologies and Apex Group did in the traditional private credit industry. They act as intermediary between the fund or lender and its investors. For decades, they have maintained investor records, processed subscriptions and redemptions, paid distributions and handled the tax paperwork. Without them, no private credit fund could operate. But that’s also why this was the largest cost centre. With Securitize, the transfer agent is turned into a smart contract.

Aave Horizon is acting like a prime broker for on-chain lending. They provide secured financing, leverage facilities, asset custody, and liquidity solutions to help funds optimise their capital structure and execute complex lending structures. Maple gives us an early peek into what an on-chain BlackRock might look like.

We are seeing similar patterns emerge with the dollar deposits. Earlier this week, I discussed how banks are reinventing to defend their deposit.

Read: Defending the Deposit

The deposit is being unbundled into yield, settlement, insurance, and convertibility, and those who can bundle those layers back again using blockchain at the lowest cost can capture maximum value from their customers.

Private credit is in the same place now. Blockchains split the single fee that used to pay for both underwriting judgment and back-office procedures into two parts. The value emerging from capturing the back-office half is what the new infrastructure will fight for.

But there is one counterargument here. One reason investors hold private credit is that it doesn’t trade frequently. Quarterly NAVs make it seem like the volatility doesn’t exist. Once blockchains make the asset liquid, volatility returns. So blockchain does not make all private credit better. It compresses the operational layer. But that’s where it offers advantages. Blockchains can affect how the asset behaves by making it less likely to default or more likely to recover.

Consider the First Brands and Tricolor bankruptcies from last September. They were cases of fraud where executives pledged the same collateral to several lenders at once. The traditional lenders overlooked the duplicate pledges. On-chain collateral records make that mechanically impossible. The IMF, the FSB, and the Fed have all flagged opacity as the central systemic risk in private credit. Transparency is the feature regulators should demand the most from private credit.

As an industry, private credit was supposed to be a better alternative to the loopholes in banking. Now, an alternative to traditional private credit is emerging in on-chain credit.

This pattern will keep repeating wherever there are inefficiencies to address and value to capture. We saw it with banks that were equivalent to deposit businesses until Merrill Lynch unbundled them and offered much more than just a savings-account-level return; exchanges were synonymous with the trading business until perpetual and event contracts forced them to become multi-asset brokerages.

The impact of blockchain infrastructure on lending extends beyond the asset class itself.

Lending is one of the oldest businesses in the world. Most of what makes it expensive is not the lender’s judgment but the friction around it, including agent banks, transfer agents, lawyers, and quarterly cycles. Once you compress these, lending gets cheaper to deliver.

Additionally, on-chain dollars can be routed to a tokenised loan book that earns the holders far more than 0.6% in a savings account. This is a big win for a retail user with dollars.

The infrastructure that rests between the underwriter and the borrower is up for grabs. Whoever expands across different layers of that infrastructure will stand to gain the most.

Securitize already owns the distribution layer, with BlackRock, Apollo and Hamilton Lane using its infrastructure. Aave Horizon operates on the composability layer. But Maple is the only on-chain native that already does credit underwriting at scale. It is also the only one of these three that owns both judgment and infrastructure. Its in-house credit team underwrites the loans, its smart contracts settle them, and its syrupUSDC product distributes the returns across DeFi pools at Aave, Pendle, Kamino and Sky. This is similar to what BlackRock does with capital, judgment and platform under one roof. Maple’s balance sheet is also the only one that has been stress-tested in the aftermath of the FTX collapse. That episode has forced Maple to build institutional discipline that others have not yet had to develop.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.