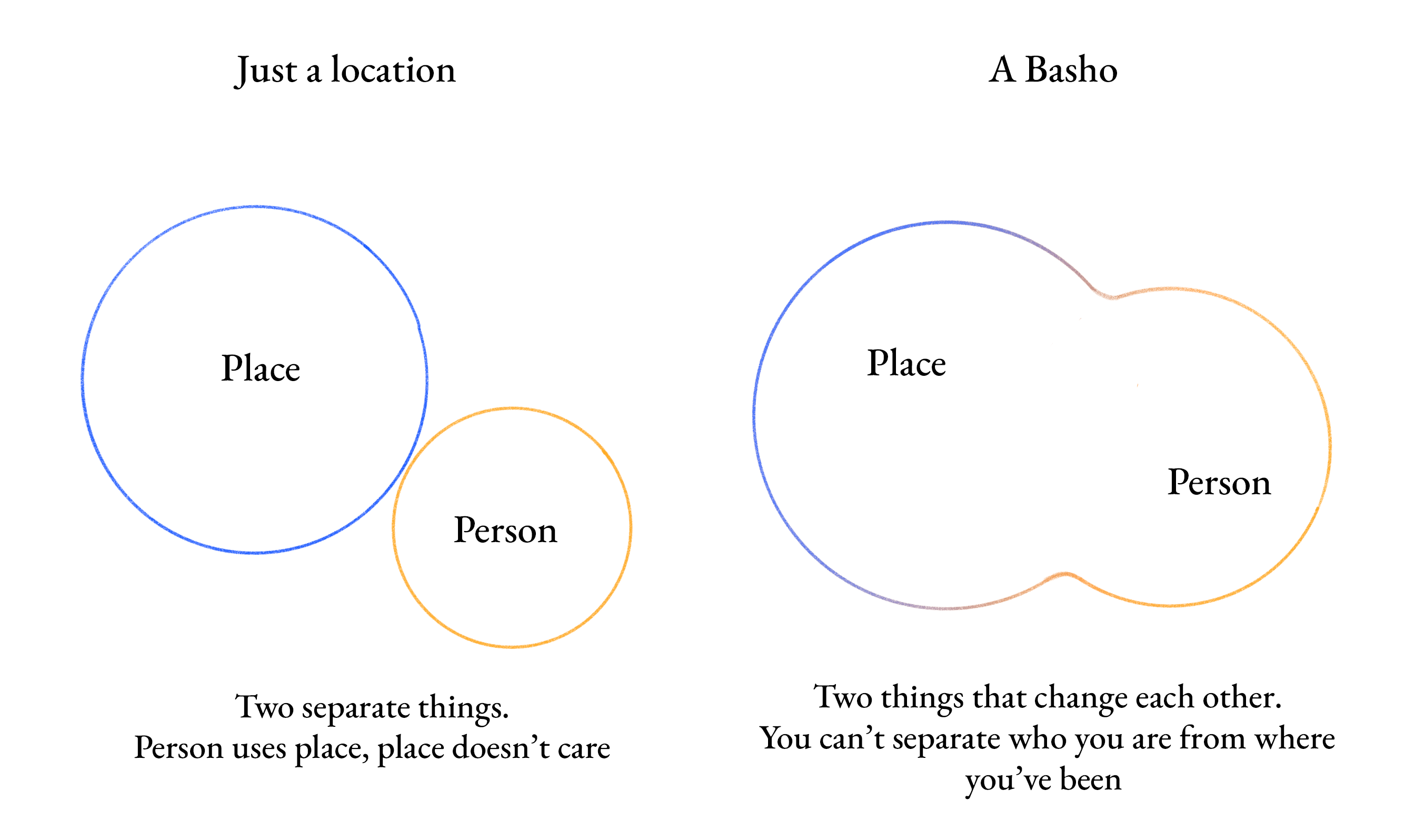

A few days ago, I was reading about basho, a concept in Japanese philosophy. Loosely translated, it means place, but the philosopher Kitaro Nishida meant for it to be something much harder to pin down than a location. More like a condition. The field in which things became themselves through it.

To clarify, let me explain it this way: a person is not someone who happens to be somewhere. Rather, they are shaped by the place they inhabit. Nishida was writing about consciousness and being. Sounds like a silly commonsense packaged in sophisticated words to some of you, but apologies, I am going to use this theory today.

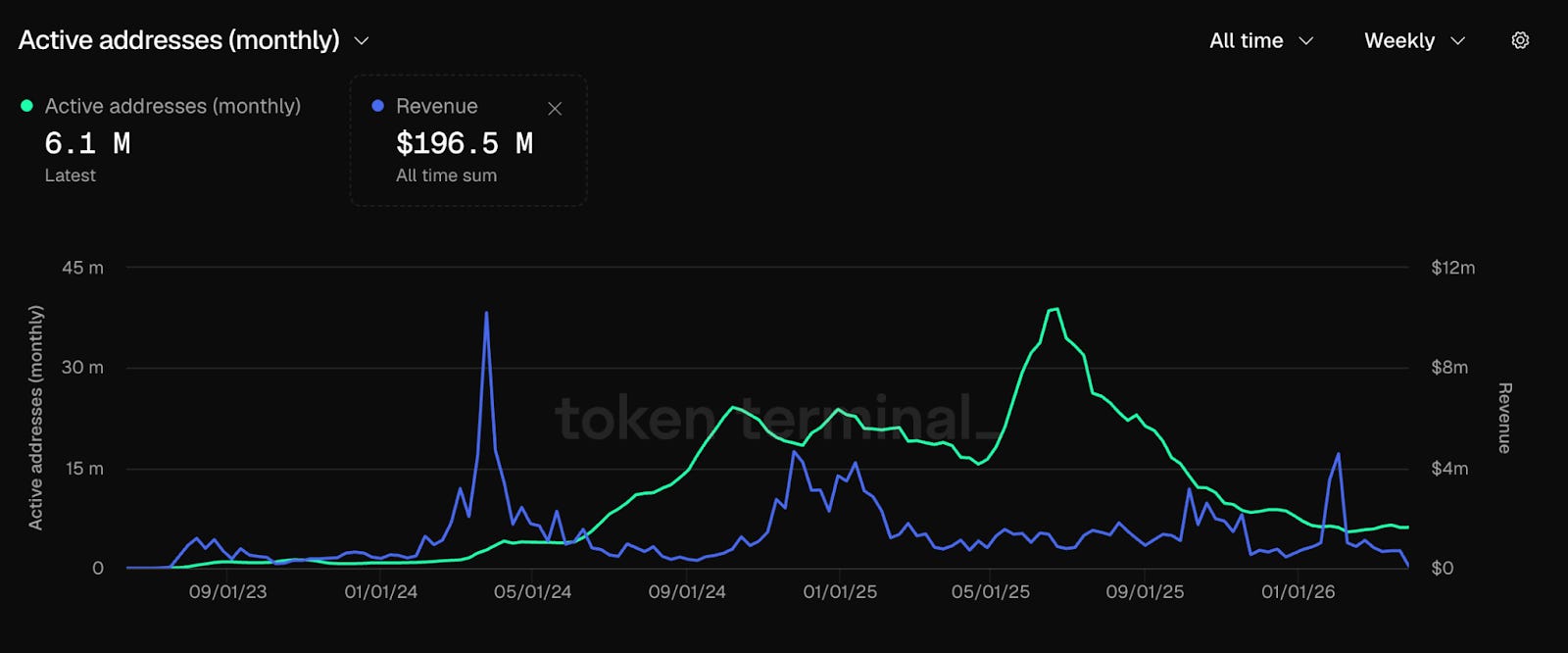

Talking about Base here. The active addresses hit an 18-month low last month. Reflecting on it, I realised what Base built was a location, but what it never built was the conditions for something to grow and become.

When Coinbase launched Base in 2023, the crypto-native believed, and “belief” is not very common for us. Here was the answer to the oldest problem in Ethereum. All this infrastructure, but no users. Coinbase had its 100 million users and unmatched distribution, which had a unique advantage. When the door opened, the users were already waiting.

For a while, the belief seemed justified. Base grew faster than any Layer 2 (L2) before it. Total Value Locked (TVL) hit $5.6 billion in October 2025. Fee revenue was unmatched across the entire L2 layer. Given that, the token confirmation in September 2025 felt like a moment when a successful experiment became permanent. Yes, a location becoming basho. (Now you know what it means.)

Then, the users left.

To get to the numbers. Active addresses on Base are back to where they were in July. The token confirmation delivers exactly what airdrop farmers needed it to. A final paycheck and nothing more.

Base’s 2025 bet on the creator economy didn’t help either. The mechanism was Zora, a protocol that tokenises content by default. By the end of the year, 6.52 million creator and content tokens had been issued through Zora on Base. Of those, only 17,800 showed sustained activity throughout the year, representing 0.3%. The other 99.7% were gone before anyone came back for a second look.

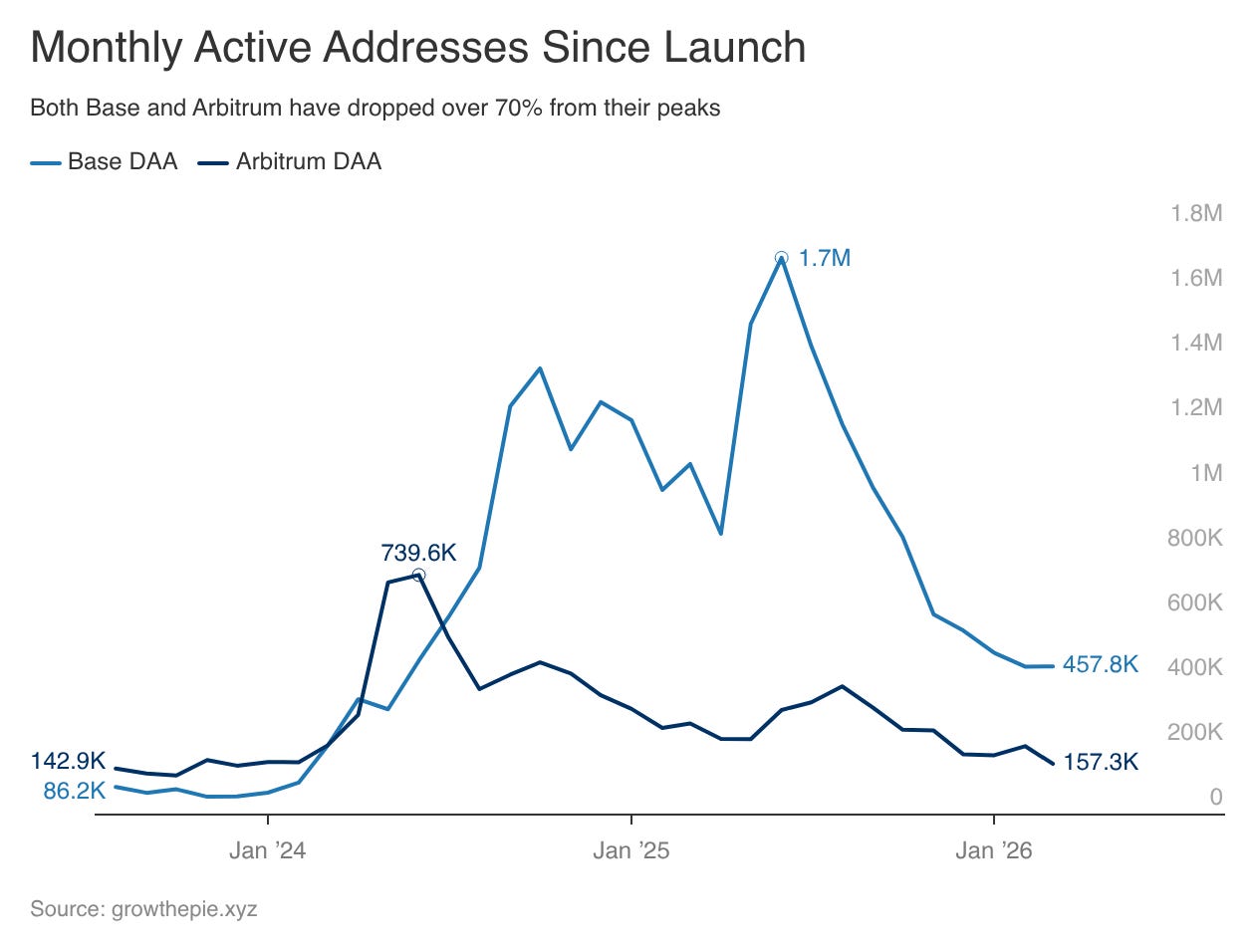

Base peaked at 1.72 million daily active addresses in June 2025. By March 2026, it is at 458000- a 73% drop from the peak. After Armstrong’s September 2025 statement that Base was exploring a token, Base contracted 54% in active addresses over the following six months, meaning the speculation had left.

The sociologist Ray Oldenburg studied what makes people return to a place without being paid to. He called them third places, which include bars, barbershops, and town squares. Not productive spaces, but places that gave people a reason to come back that had nothing to do with an incentive. The whole point was that the wanting to return cannot be manufactured. It has to emerge from what the place makes possible over time. Crypto designed its places for extraction and then wondered why nobody stayed.

This is what a location without a basho looks like: people pass through, extract what they need, and leave because there’s no cost to leaving. No identity was formed here. Or no capability built that could not be rebuilt elsewhere in three weeks. Nothing that makes departure feel like a loss rather than a simple redirect. Is there a relationship that exists only on this chain? We did not build stuff that way, did we?

You cannot build basho with financial incentives. You sure can use incentives to get people through the door. Cannot use them to make people want to stay. The wanting to stay has to come from what the place makes possible over time. Nishida called it the logic of place, which is the way a field of relations shapes what emerges within it. Crypto designed the field for extraction and was surprised when extraction was all that emerged.

Brian Armstrong publicly said that the Base App is now focused on being the self-custodial, trading-focused version of Coinbase.

The social and creator vision, the one that was supposed to make Base sticky, was supposed to give users an identity on the chain that was worth protecting, but it is gone. It is a rational call given what the data showed. It is also an admission. The condition never formed. Base has a location, and it is now optimising for people passing through, because that is what it has.

One chain, one category

Base is the most visible example of a pattern seen across the entire L2 landscape.

Usage across smaller L2s has declined 61% since June 2025. Most chains outside the top three are now zombie chains. Active enough not to be shut down, not active enough to matter. The L2-to-L1 daily active users ratio dropped from 15x in mid-2024 to 10 to 11x today. Most new L2s saw usage collapse after the incentive cycles ended. The whole layer is cooling, not just Base.

Read: Vitalik Didn’t Blink 👾

The rollup-centric roadmap used to be a theory about how adoption would work. Lower the cost of participation, users arrive, ecosystems form, and everything compounds. The Ethereum Foundation published a 38-page mandate this year about what Ethereum wants to be. The biggest L2 just hit an activity low and left the OP Stack. The second biggest is flat.

Read: What Ethereum Wants to Be

Lowering the cost of arrival is not the same as creating the condition for something to become. They solved the access problem and assumed belonging would follow. It did not follow. It cannot follow automatically because belonging is not a feature you ship.

Farcaster is the closest crypto has come to building it. Because a specific group of people built a specific culture on top of it. Builders sharing work, arguing about Ethereum, forming opinions about each other over months. That takes time, and it cannot be replicated by a competitor offering higher rewards. Friend.tech tried the incentive version of the same idea. It peaked in a week and died in a month. Same mechanic, no culture. The difference was not the product. It was a question of whether anyone stuck around long enough for something to form.

What holds?

The chains holding users through the cooling are not holding through better incentives.

Arbitrum peaked at 740,000 daily active addresses in June 2024 and is now at 157,000, also down 79% from peak. So both chains are falling.

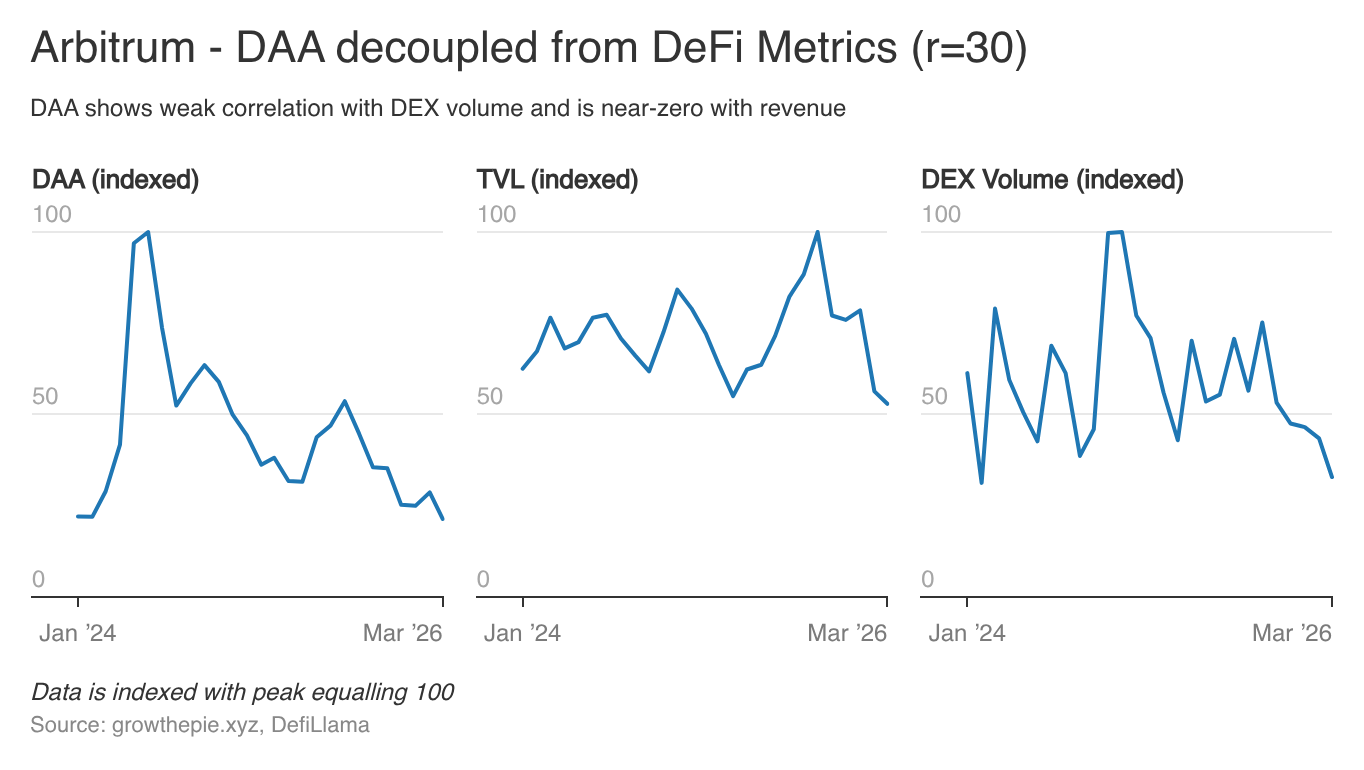

But the mechanism is different. Base's users show up to trade. When trading slows, they leave. Arbitrum's users are there regardless of fee levels. The correlation between its user count and fee revenue is near zero. Base attracted tourists. Arbitrum, somehow, kept locals.

Hyperliquid holds because the trading experience is different, and the community around it has developed an identity that exists nowhere else. Token incentives hardly matter there. Being there has become part of how they operate and what they are. Something is shaping the users, and the users are shaping it back.

The crypto industry is still optimising for arrival. The question of condition is only asked after the numbers go wrong, never before the chain is designed.

I would argue that Base has the distribution to solve this better than any chain that has ever existed.

Right now, it is a trading app. That is a legitimate thing to build. It is also the thing that 40 other products already are, and trading apps do not produce basho. They produce sessions. Users come when they have a trade to make and leave when it is done. The condition for becoming requires something more continuous than that. It requires the kind of relationship that builds between visits, making the next visit feel like returning rather than arriving.

Armstrong’s pivot is a lot about what Base learned from the data. The social layer, the creator economy, the on-chain identity that was supposed to make Base a place people inhabited rather than used - those required patience that the metrics did not reward. Quarterly active addresses and TVL are measures of location. And so the condition was never prioritised.

The Ethereum ecosystem needs Base to be more than a trading venue. The whole L2 thesis rests on the assumption that chains can become the kind of infrastructure people build lives around. If the best-distributed L2 in the history of crypto settles for being a fast Coinbase, the thesis answers itself.

Nishida believed that the deepest basho is one where the distinction between self and place begins to dissolve. Where you cannot fully separate who you are from where you have been shaped. That sounds abstract. But then think about what it would mean for a chain. A user who cannot imagine their financial life without a specific chain. A developer whose entire toolkit is native to one ecosystem. The identity hardly exists somewhere else.

That has never been built on an L2, to my knowledge. It might not be buildable on an incentive schedule at all.

I know I stretched “basho” a bit too much. The point is easy. You can have 100 million potential users and still end up with an empty room if there is nothing worth staying for. Base knows this now.

It hasn’t figured itself out yet.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.