Hello,

A clock is a bad place to hide a delay. For decades, financial markets were built around the speed of incumbent communication. They introduced closing bells, batch settlement, and regional exchanges, which made sense when information moved slowly. But that has all changed. Capital doesn’t wait. Just like water always finds a crack, so does capital. Financial gravity pulls it toward the fastest route to price information. That’s the law of markets. Its constituents don’t tolerate inefficiencies forever.

This is what I observed when I zoomed out from the financial market developments over the last fortnight.

In today’s piece, I will help you understand what’s breaking down the old, bundled structure of financial markets into a more efficient, unbundled one across venues, wrappers, and time.

Change of Guard

I have been studying finance for over a decade now. In the first half of my journey, I viewed a traditional stock exchange as synonymous with markets. For most of their evolution, it was the one place where everyone, and everything, came together. Buyers, sellers, regulators, and the technology driving the market. It had indices tracking its constituents and a clock that told everyone when they could and could not trade.

But that has changed in the past few years. In fact, just in the past fortnight, we have seen multiple developments that confirm this shift.

On March 18, S&P Dow Jones Indices licensed the S&P 500 to Trade[XYZ], allowing the HIP-3 market deployer to launch the first and only perpetual derivative contract for the S&P 500 on Hyperliquid’s exchange. The S&P 500 is the most-tracked gauge of U.S. large-cap equities across the globe. It tracks the 500 leading U.S. companies, covering ~80% of total U.S. market capitalisation, totalling over $61 trillion. The index covers at least half of the entire global equity market.

That’s nearly a 70-year-old index being listed on a market that’s barely six months old.

Read: Everything Is a Ticker 📊

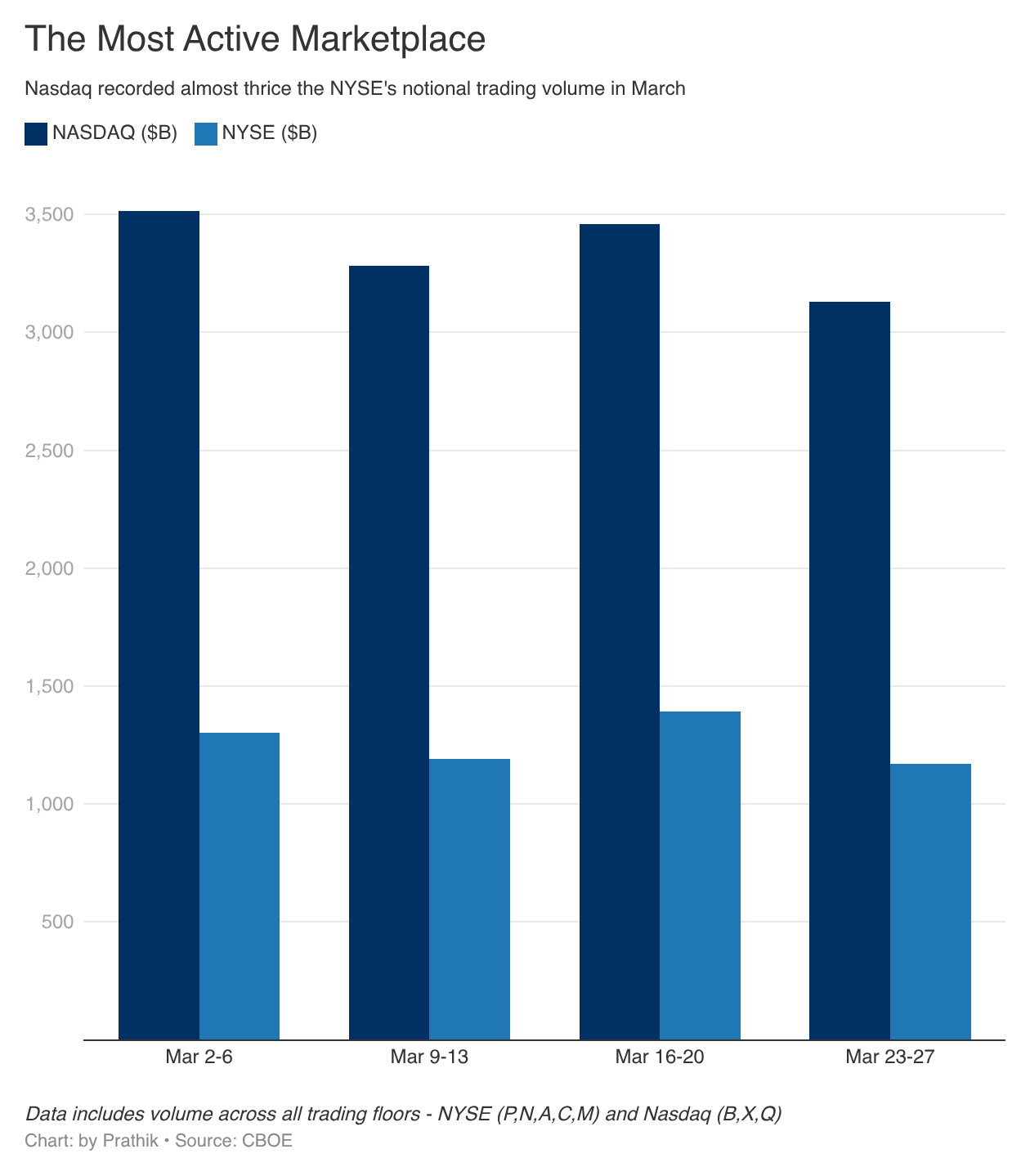

A day after S&P’s announcement, the U.S. Securities and Exchange Commission (SEC) approved Nasdaq’s request to trade and settle certain stocks in tokenised form. Nasdaq is one of the most active trading venues in the world. Its notional trading volume often exceeds that of the NYSE, the world’s largest exchange by market cap.

On March 16, Cboe Global Markets submitted a proposal to the SEC to launch “near 24x5 U.S. equities trading”. The biggest operating engine behind American financial exchanges said it was ready to deliver around-the-clock equities trading as early as December 2026.

But why? More people are demanding extended trading hours for U.S. equities.

All three developments collectively target the outdated bundled structure. Hyperliquid’s perp market on the S&P 500 index challenges the decades-old practice of investors being able to trade traditional indices only via traditional markets. It also makes trading on one of the most-tracked large-cap indices possible 24/7 worldwide.

Nasdaq’s tokenised equity trading move is targeting the infrastructure. It introduces a new wrapper that allows the same share to be traded differently. Earlier attempts at tokenised equity faced criticism from the industry.

The investors questioned whether these tokens would offer the same rights as the original shares. I wrote about this here.

But what if I offer the same equity exposure via a token on a blockchain, without losing the voting rights and legal protections that came with the original dematerialised share, won’t you take it?

Why should you, and what’s in it for you?

Now, what if you were an investor outside the U.S. who wanted easier access to the equity market of the world’s largest economy? What if that tokenised share made it easier for you to integrate it with collateral and lending systems?

The benefits compound when you factor in round-the-clock trading.

That’s what the Cboe is attacking. Its near-24/5 trading proposal is its way of acknowledging that capital doesn’t wait for office hours. Traders would always want to express their opinions as soon as they receive information. If Cboe didn’t give them a market to express at that time, then the traders would flee to the market that does.

None of what I claim is a hypothesis or “could happen in the near future”. It’s happening as we speak.

An Unbundled Future

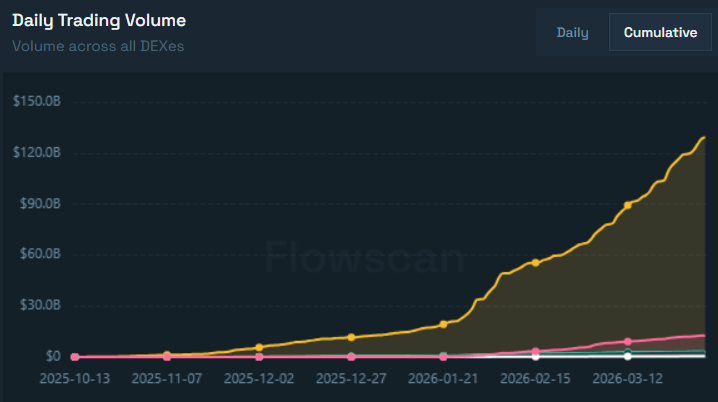

Nowhere is the adoption of unbundled pieces of finance more evident than in Hyperliquid’s HIP-3 markets, which launched only in late October 2025.

In the past month alone, HIP-3 markets added $72 billion to cumulative trading volume. In the preceding four months, the cumulative trading volume stood at $78 billion.

In March, Trade[XYZ]’s perp markets on traditional financial commodities and stocks consistently accounted for 90% of the daily trading on HIP-3. But that’s not even the most interesting aspect.

More than half of Trade[XYZ]’s trading came from just perpetual markets on silver, crude oil, Brent oil and gold. I wrote an entire piece at the start of this year when this trend first began to emerge.

Read: Hyperliquid: House of Finance 🏦

In that piece, I explained why traders prefer to trade commodities on-chain. Hyperliquid offered a single venue for trading both spot crypto and perpetual contracts on crypto and traditional assets. This provided not just ease of trading on a unified platform, but also better liquidity, a single user interface, and tighter bid-ask spreads.

Traders still wanted to trade on some of the largest and most popular assets across commodities, listed companies, large private companies and indices. You could be wanting to trade Silver, Gold, Oil, Tesla, Apple, Amazon, Google, the indices tracking the top 100 U.S. non-financial companies, and the S&P 500 - and do all of it on Hyperliquid.

HIP-3 unbundled the ability to invest in these assets from the existing exchange infrastructure, while still tracking the underlying assets from their original base. So, when you go long on a perp contract for Silver on HIP-3, the underlying asset it was tracking was still linked to the value of one troy ounce of silver on Pyth’s data feed.

What made traders switch to trading Silver on HIP-3 from their earlier platforms was that HIP-3 didn’t discriminate between U.S. and non-U.S. traders. It didn’t follow any one clock. Whenever there was an event that made traders want to express their opinions by pricing assets, HIP-3 offered them a market. Irrespective of the trader’s geographic location or time zone.

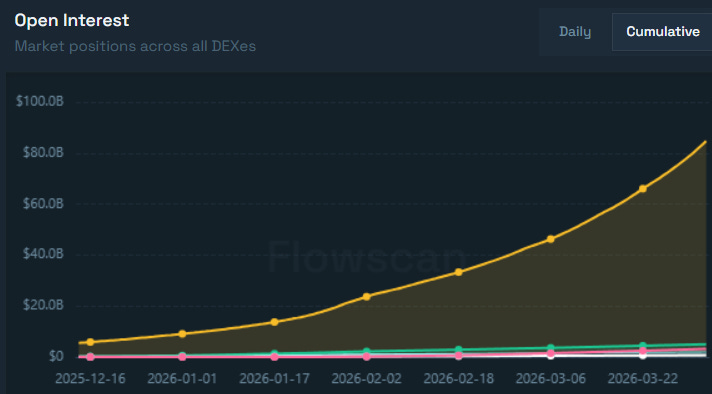

The result is evident in the growth of Open Interest (OI) on Hyperliquid over the past few weeks. OI measures the total value of outstanding derivative positions. Unlike trading volume, which captures activity, OI reflects commitment.

OI doubled from $1.13 billion on March 1 to $2.2 billion on April 1. This shows the conviction with which traders are locking in their money on Hyperliquid’s perpetual contracts.

These metrics demonstrate that when you make access to markets easier with fewer frictions, traders will not remain loyal to a platform or one asset class. They will adopt whatever gives them volatility, convenience, and liquidity.

That’s why legacy institutions like S&P, Nasdaq, and Cboe are making moves to acknowledge this behaviour.

At least two recent incidents prove how important round-the-clock trading and volatility are for traders.

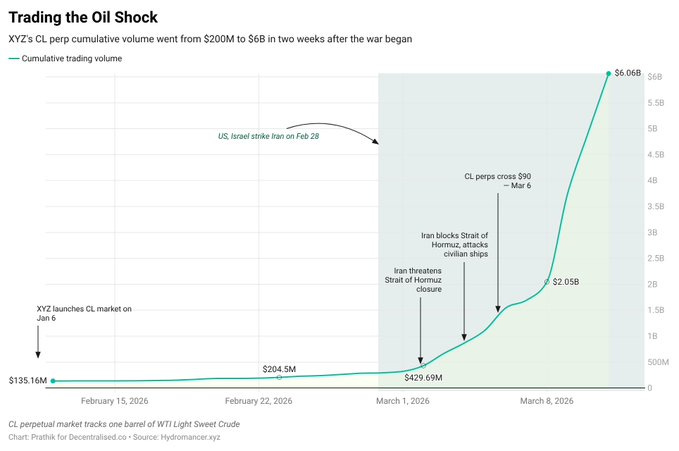

Saurabh wrote in his tweet for Decentralised.Co: “On February 28, the U.S. and Israel struck Iran when the traditional markets were closed. Within hours, oil-linked perpetuals on Hyperliquid surged 5% as traders priced in the shock in real time.”

Trading on oil-linked perps shot up from $200 million to $6 billion in cumulative volume within just two weeks after the war began.

One of the concerns with newer platforms is liquidity. If there’s not enough liquidity, the bid-ask spread could widen, leading to worse pricing for traders than on other platforms.

Hyperliquid demonstrated its depth of liquidity last week, when U.S. President Donald Trump and Iranian officials were going back and forth about having “productive talks”. The newly launched S&P 500 perp on HIP-3 tracked the sequence of moves of the underlying S&P 500 on CME’s E-mini futures down to the minute.

Although the on-chain perp sat about 50–70 points below ES, the magnitude of the moves was similar.

What This Means

For decades, traditional markets remained bundled and controlled the venue (exchange), the time (trading hours), and the wrapper (indices/contracts).

They preferred to maintain the status quo because they failed to introduce infrastructure to address inefficiencies such as time delays, restricted trading hours, and regulatory limitations for non-U.S. investors. Instead, they disguised these inefficiencies and offered them to investors by calling them procedural systems put in place to offer a trustworthy and credible institution.

People traded and invested anyway. Not because they were foolish or bought into the story that bundled legacy financial markets sold to them. They did so because they had no other option. That started to change when blockchain offered the world on-chain markets that made trading and investing easier than ever before.

People saw the option and took it.

They did not and will not care if the market structure changes. They wouldn’t care less whether the new structure was bundled or unbundled. Whether the incumbents like it or not, the trader and investor communities will adopt the new market structure as long as they have better access to express their opinions through financial instruments. It won’t matter whether that structure comes from traditional giants such as Nasdaq, Cboe, or the S&P 500, or from permissionless platforms running on blockchains.

Finance, as it always has, will continue to evolve and adopt whatever structure narrows the gap between the occurrence of an event and the expression of an opinion through price.

Important events happen round-the-clock across the globe. Why, then, should a price wait for a clock to start ticking on a Monday morning in a glassed building in New York?

That’s it for today. I will be back with another deep dive.

Until then, stay curious!

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.