Japan Just Put Its $9T Bond Market On-chain

Crypto’s most important infrastructure win is happening inside traditional finance

Hello,

On a Saturday in August 2025, something happened that should have broken every crypto group chat on the internet. Bank of America, Citadel Securities, DTCC, and Société Générale settled a U.S. Treasury repo transaction in real time on a blockchain over the weekend. A repo, for context, is one of the most basic trades in institutional finance, where one party sells a government bond to another with an agreement to buy it back the next day, usually to raise short-term cash overnight.

It’s the plumbing of the financial system. Banks, hedge funds, and central banks use repos every day to manage liquidity, and trillions of dollars move through this market. And for the first time ever, that transaction occurred on a blockchain, outside market hours, with near-instant atomic settlement among some of the world’s largest financial institutions.

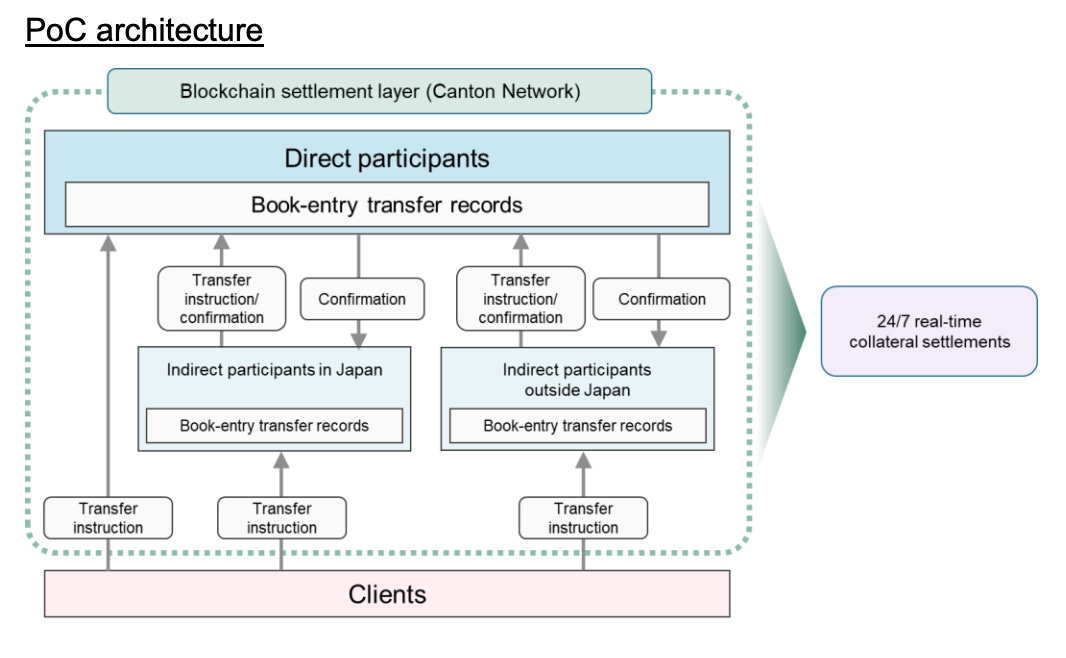

Eight months later, on April 20, 2026, Japan’s central clearing house JSCC, Mizuho Financial Group, Nomura Holdings, and Digital Asset launched a proof-of-concept to move Japanese government bond collateral (JGBs) onto the Canton Network. JGBs are among the most important financial instruments in Asia, with over $9 trillion in outstanding value, and are the single most widely used collateral asset across the region’s institutional markets. When banks and hedge funds across Asia need to back their leveraged positions, JGBs are often the first ones they reach for. And now that the entire collateral system is moving on-chain.

This is probably the most consequential blockchain story of 2026. In this piece, I’ll break down why JGBs are the right asset to tokenise first, why Canton keeps winning institutional deals while public chains fight over retail volume, and what always-on collateral settlement actually changes for global trading desks.

Why JGBs, and why now?

For decades, Japan tried to make the yen a global reserve currency, but it never really happened. Even today, the yen accounts for only roughly 4-6% of global reserves, trailing the dollar, the euro, and even the pound. But somewhere along the way, something unexpected happened: Japan’s government bonds became one of the fastest-growing collateral assets on Euroclear’s Collateral Highway, the infrastructure that moves collateral between the world’s largest financial institutions. Foreign ownership of JGBs has climbed to about 11.9%, or roughly ¥144 trillion, held by institutions outside Japan.

In institutional finance, collateral is everything. Every leveraged position, every derivative, every repo trade needs high-quality assets backing it as collateral. And JGBs, backed by the world’s third-largest economy and with essentially zero default risk, are among the few assets that meet that bar globally. When a hedge fund in Singapore takes a leveraged position, or a bank in London covers derivatives exposure, JGBs are often pledged as collateral. Crypto’s most important infrastructure win is happening inside traditional finance. They’ve become the operational infrastructure in Asian institutional finance without Japan ever having to win the currency war.

The problem is that the entire collateral system still runs like it’s 1995. A JGB collateral transfer between two institutions goes through a tiered holding structure. It starts with the Bank of Japan at the top, then with Hofuri (Japan’s central securities depository), then with custodian banks, then with sub-custodians, with each layer reconciling separately, and each operating only during Tokyo business hours, roughly 9 am to 3 pm JST.

A collateral move that should take a few seconds ends up taking days. And during those days, that collateral is frozen. A desk in New York that needs it at 10 pm can’t touch it until Tokyo wakes up. AGFMA study with BCG estimated that Blockchain could free up $100 billion in stuck collateral globally, and for a single bank running $100 billion in daily repo volume, tokenised settlement could save $150-300 million a year just on operational overhead.

And here’s something that should be very concerning for Japan. The U.S. has already moved on-chain. The Depository Trust & Clearing Corporation (DTCC), the single entity that custodies $99 trillion in American securities and processes $3.7 quadrillion in transactions annually, partnered with Digital Asset in December 2025 to tokenize U.S. Treasuries on the Canton Network. That means the backbone of the U.S. securities infrastructure is now moving towards 24/7 tokenised settlement.

Broadridge is already processing $354 billion daily in tokenised Treasury repos on the same network, and JPMorgan’s Kinexys has moved over $1.5 trillion in cumulative volume through its on-chain payments rail. U.S. Treasuries are quickly becoming always-available, always-movable collateral assets, while JGBs are still locked to Tokyo office hours.

If you’re a global fund manager and you need to post collateral at 2 am for a margin call, and if you have the option to pick a tokenised Treasury that settles instantly compared to a JGB that won’t move until Tokyo opens in six hours, I believe you’ll pick the Treasury every single time. Multiply that decision across thousands of desks, and JGBs risk losing their status as top-tier collateral.

For a country whose sovereign bonds are deeply woven into the collateral fabric of Asian finance, it could even be an existential problem. The four companies behind the JGB on-chain trial used the word “urgent” in their press release, and given how quickly U.S. infrastructure is moving, it’s hard to disagree.

Why Canton keeps winning

Pratik & Tejaswini have covered Canton extensively at Token Dispatch, including its architecture and privacy model, its position in the broader institutional blockchain race, and the competitive debate around its approach. So I won’t rehash the basics here. What I want to focus on is why Canton specifically keeps landing these massive institutional deals, and what that tells us about where institutional finance is actually headed.

When Japan’s JSCC had to pick a network for JGB collateral, they picked Canton, the same chain that the DTCC, Broadridge, and JPMorgan are already building on. And the reason comes down to what sovereign bond collateral actually demands from a network.

Sovereign bond collateral has a very specific set of requirements that most blockchains can’t meet. When Mizuho moves JGB collateral to a counterparty in London, the transaction must comply with Japan’s Book-Entry Transfer Act, which governs how ownership rights are recorded across a tiered custody chain. The blockchain record needs to stay legally synchronised with Hofuri’s official registry.

Every party in the transaction, from the clearing house to the custodian and the counterparty, needs to see only the data they’re authorised to see under Japanese and international securities law. And the whole thing needs to settle atomically, meaning the collateral and the payment move at the exact same instant, or neither moves at all.

That’s an insanely specific set of constraints. And the reason Canton keeps getting picked is that its architecture was designed to tackle these problems. Each institution runs its own ledger, and cross-institutional transactions synchronize only the data each party is legally entitled to see. The smart contracts themselves, written in Digital Asset’s Daml language, encode who can see what and who must authorise what at every step.

So when JSCC, Mizuho, and Nomura run a JGB collateral transfer on Canton, the clearing house sees the full picture; Mizuho sees its side; Nomura sees its side; and nobody sees anything they shouldn’t. Canton is now the only network in the world where the three largest pools of sovereign bond collateral - The U.S. Treasuries, Japanese government bonds, and European government bonds- can move freely, 24/7, across borders in real time. No other network, public or private, is anywhere close to that.

What always-on collateral actually changes

Most coverage of tokenised on-chain settlement stops at making the point that it’s faster. But that’s where it starts, the real change lies in what happens to the system’s behaviour under stress.

Think about what happened during the COVID-19 pandemic in March 2020. Markets crashed, volatility spiked, and initial margin requirements on equity futures jumped 100% in a matter of weeks. Funds that couldn’t meet margin calls had to liquidate assets to raise cash.

But selling assets into a falling market pushes prices lower, triggering further margin calls and forcing more selling. That feedback loop is one of the most dangerous dynamics in finance, and it nearly broke things again during the UK’s LDI pension crisis in September 2022.

Here’s what 24/7 tokenised settlement changes about that.

Right now, when a margin call hits, most funds have to sell assets to convert them into cash before they can post. With on-chain collateral, a fund can pledge JGBs or Treasuries directly to meet the call without first converting them to cash. The forced-selling loop weakens as fewer institutions dump assets into a falling market solely to raise liquidity.

Then there’s the “give-before-get” problem. In a traditional repo, the cash lender sends money first and receives collateral later. There’s a brief window when one side is exposed, they’ve sent their end, but haven’t received the other side. Banks price that intraday exposure into their haircuts and funding costs.

But with atomic settlement on-chain (meaning the transaction either settles fully or doesn’t execute at all, with no in-between state) both legs of the trade, the collateral, and the cash move at the exact same instant, or neither moves. Santander actually tested this in December 2024, executing $50 million in USD and €50 million in EUR intraday repos on JPMorgan’s Kinexys that unwound automatically three hours later. Intraday repo, which used to require complex tri-party setups or committed credit lines, has now become routine.

What’s more interesting is that during the January 2026 Canton demo, London Stock Exchange Group (LSEG) brought its Digital Settlement House (DiSH) into the transaction, which uses tokenised commercial bank deposits as the cash leg instead of stablecoins. This is because banks won’t settle billion-dollar trades in USDC; it’s a private IOU, not money good. DiSH tokens represent actual deposits at regulated banks and are transferable 24/7 on-chain. That solves the cash side of the equation, the last missing piece for institutional adoption, and now Japan wants to plug JGBs into this same infrastructure.

What this means

If this JGB trial works, U.S. Treasuries are already live, and European sovereigns are in the demos, then Canton, to me, is starting to look a lot like the next SWIFT.

A single network that becomes the default layer for moving the world’s most important collateral across borders. And just like SWIFT, once enough institutions are on it, leaving becomes almost impossible. The network effects compound. Every new sovereign bond class that joins makes the network more valuable for everyone already on it, and harder to compete with for anyone trying to build an alternative.

I think that’s worth sitting with for a second. We spent years in crypto debating decentralisation, worrying about single points of failure, building systems where no one entity could control the rails. And now the most consequential blockchain deployment in history is converging towards a single permissioned network governed by the same institutions that already run global finance.

Whether that’s a good thing depends on what you think the point of all this was. If the goal was to make capital markets more efficient, reduce settlement risk, and free up hundreds of billions in stuck collateral, this is working. If the goal was to redistribute power away from incumbent financial institutions, it’s doing the opposite. The same gatekeepers are now running better infrastructure.

I don’t think that makes it less important. The financial system settling government bonds on a blockchain, 24/7, across borders, with atomic execution, is a genuine upgrade to how global finance works. But I do think it’s worth being honest about ‘what kind of’ upgrade this is. It’s an efficiency revolution: the plumbing is being rebuilt, but the plumbers remain the same.

That’s it for today. See you next week.

Until then, stay curious.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.