Hello,

I love discussing how crypto is changing the way money moves. It feels nice, but the reality is nuanced. One look at how the big institutions have been moving money for the past decade tells you the story.

A bank wire transfer across the Atlantic still takes one to two days. It needs to pass through intermediary banks, generates reconciliation entries at each point, and costs the client about $25 to $45. It’s the same architecture from the 1970s, except email replaced telephone communication and SWIFT replaced the tangled cables. Of course, the databases got faster, too. But that’s that. Timelines didn’t shrink proportionally.

You might think this is a technology problem, but I think it’s more of a coordination problem.

We have had blockchains and stablecoins for over a decade now. Yet they never resolved all the problems at once. Some offered the speed institutions needed, but put all data in public by calling it transparency. Others ensured both speed and privacy but created siloed systems that couldn’t talk to each other.

The thing with new technologies is that they easily scare away large institutions operating in highly regulated industries. Think banks. For them to migrate to new technologies, they need to see all their pain points addressed in advance. None of them can be issues that are “can be taken care of after we migrate”.

It took a while, but this is finally changing. Ironically, banks are now resorting to blockchains to avoid ceding ground to digital assets.

Last month, five US banks with over $750 billion in combined assets launched Cari Network. This system will convert ordinary deposits into digital tokens that settle instantly, operate 24/7, and remain FDIC-insured.

In today’s deep dive, I will tell you how blockchain builders have tried to build solutions for institutions in the past and what makes this time different.

Swings and Misses

About a decade ago, consortia like R3 and Hyperledger built private blockchains for institutions with ambitious roadmaps and membership lists that included the BNPs, Citis and Barclays of the world. Although these chains worked and updated the ledgers accurately, they were siloed and couldn’t interact with anything outside the walled infrastructure.

Such efforts died a slow death. Some others pivoted to other approaches.

Then, the banks tried the public blockchains - mostly Ethereum. It immediately solved the composability problem. A shared, neutral ledger that everyone can access enabled banks to interact within their ecosystem. But solving one problem gave rise to another. On a public chain, every counterparty, every transaction, every balance was visible to anyone who knew where to look, just using a browser.

What banks needed was a single system that offered them privacy, compliance, speed and connectivity.

What Changed

Two breakthroughs came in 2025: one technological and another - necessity.

First, let’s understand the technology. Zero-Knowledge (ZK) proofs caught people’s attention for what they offered. ZK proof is a cryptographic method that lets you prove a transaction is valid without revealing its details.

Read: The Privacy Correction 🔐

Although the technology has existed for years, it has only got cheaper and faster recently. Generating these proofs used to be expensive enough to make the whole system impractical to deploy from a business perspective.

The number of transactions processed per second has jumped from as low as 400 to at least 15,000. The time taken for a transaction to reach finality has dropped below a second. All this while keeping the transactions and the details of the parties involved private. For context, traditional financial infrastructure still takes at least a day to process these transactions.

ZK proofs also solve what enterprises saw as another deterrent.

A bank evaluating blockchains in 2018 had to hire engineers, build a chain from scratch, figure out how to generate proofs, run its own servers, and then see if all this translated to business gains. So much for a system they weren’t even sure would work.

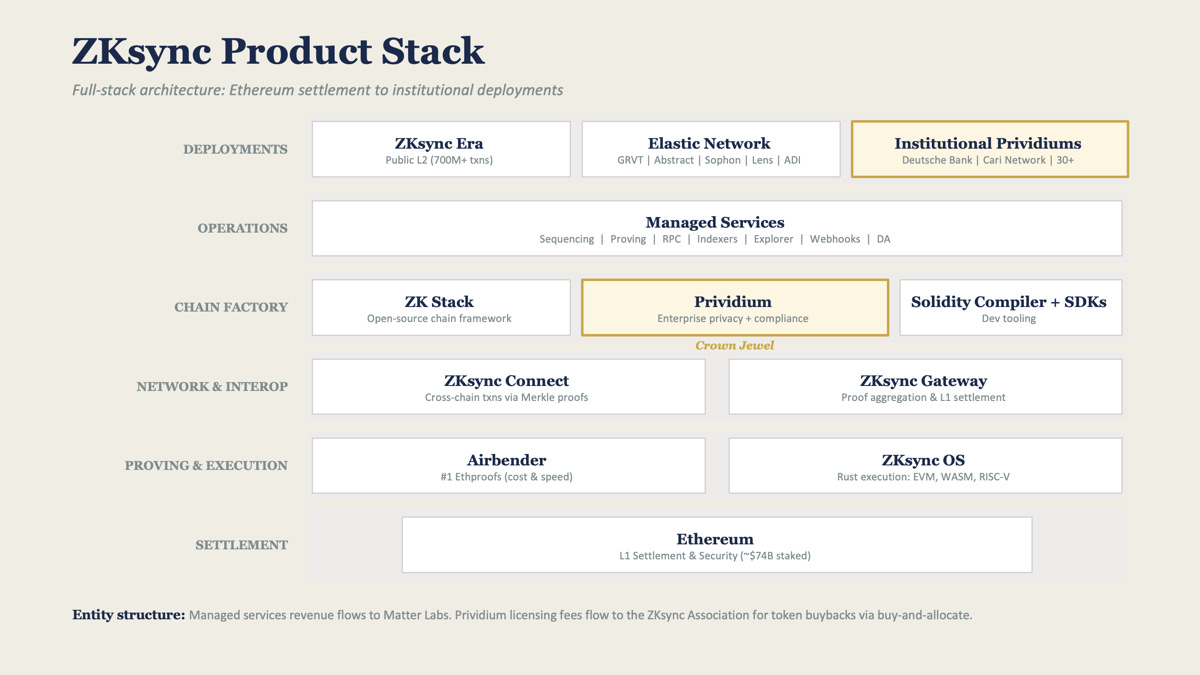

ZKsync, an Ethereum-scaling platform built by Matter Labs, addresses this by giving enterprises a blockchain equivalent of AWS. Its institutional product stack, including Prividium, Connect, Gateway and others, offers chain deployment, transaction processing, proof generation, compliance tooling - including KYC checks, role-based access, login controls, and connectivity to other chains.

The stack allows an enterprise to tailor its configuration and get started with deployment. Think of it as buying blockchain-as-a-service.

ZKsync isn’t the only one here. Canton Network, backed by Goldman Sachs, DTCC, Citadel, and BlackRock, takes a different approach to the problem. Instead of ZK proofs, it uses a permissioned model where approved validators coordinate private transactions between known counterparties.

They are both building connective layers that institutions need. But they disagree on whether trust should come through cryptographic proof or from contractual governance between known parties.

If you ask me, there’s little to separate between permissioned and permissionless approaches so far. Both want to solve the same problem for institutions. In fact, Canton even has better institutional partners than ZKsync.

Read: Wall Street’s Stealth Chain

Yet there is something about it that could prompt institutions to flip over to ZKsync. Canton’s permissioned network works fine as long as the interaction and movement of money is happening between known parties in familiar jurisdictions. But when an enterprise wants to expand across jurisdictions and transact with parties outside Canton’s walled-off jurisdiction, ZKsync is what helps achieve composability there.

It’s this technological breakthrough that convinces banks to adopt blockchains.

But why would banks move away from their age-old, battle-tested systems, no matter how slow they are? Just because there’s a cheaper alternative that works faster?

Do you really think banks went from “blockchains are interesting but impractical” to “blockchains make business sense” just because a technology they knew little about suddenly became economically viable? It’s funny how every technology becomes “strategically important” when businesses start losing money.

Deposits Under Siege

In the past decade, stablecoins have grown into a $300-billion market. They did what banks had refused to do for years: move money fast. Today, each of those digital dollars in circulation left the banking system at some point.

The infrastructure I described above, ZKsync’s Prividium and Canton’s permissioned rails, are what is helping these banks take the fight back to the digital assets. With these blockchains-as-a-service, banks can move their existing deposits just as stablecoins do. They can process and settle transactions with the same speed and finality. There’s also a bonus. Banks can do all this while guaranteeing their depositors with regulatory protections and balance-sheet advantages that only they can offer.

This is already happening in real-life cases.

The Cari Network, launched last month by five US regional banks (Huntington, First Horizon, M&T, KeyCorp, Old National), is tokenising bank deposits on ZKsync’s Prividium. The deposits stay on the banks’ balance sheets, are FDIC-insured, and settle in seconds.

Cari Network isn’t an isolated event.

In February 2026, the UAE’s Central Bank approved DDSC, a dirham-backed stablecoin running on ADI Chain, built with ZKsync’s proving engine.

In June 2025, Deutsche Bank began building a tokenised platform on a ZKsync-powered chain that compresses the timeline of setting up a new fund from months to weeks.

Future of Institutional Finance

There’s one core thought I often come back to when I write on finance: “How will money move in the future?” It’s an interesting question to ask oneself because it tells you about the financial behaviour of individuals and corporations.

I don’t think a majority in either category cares too much about the cardinal principles that crypto stands for. Banks care even less. I am sure the banking leadership team doesn’t sit in a boardroom debating decentralisation versus centralisation. They are surely not bothered if their transactions are processed on Ethereum, Solana or a private network based in Timbuktu.

They care most about privacy, composability and speed. If a system delivers these to an enterprise by making them save a couple of extra dollars, then you’ve got their attention. It helps further if there’s a “strategically important” reason to adopt a new technology (like a stablecoin revolution waiting to steal your business).

So, I expect the convergence of Web2 and Web3 finance to happen around the technology that helps move money more efficiently. That could be via ZKsync or Canton-powered chains that move tokenised versions of fiat currencies. Or it could even be through payment-specific chains that payment companies like Circle’s Arc, Stripe’s Tempo, and Stable are building.

I don’t think there’s going to be a winner between the two approaches. That’s because for banks that want to avoid adopting stablecoins, ZKsync’s blockchain-as-a-service will be the most obvious choice for evolution. Those already integrating stablecoins in their payments will choose digital dollar-supported chains.

But I surely know who will be the biggest loser: the one who stays adamant about using the technology that still moves and settles money based on the date and time.

That’s it for today. I will be back with another deep dive.

Until then, stay curious!

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.

The real story here isn’t tokenization - it’s the rewiring of settlement itself.