Hello,

Moving money shouldn’t be a skill you need to master. You shouldn’t have to understand how the underlying technology works before sending dollars.

There are 550 million people worldwide holding over $185 billion in USDT circulation. That’s more than the GDP of at least 120 countries. For many of them, stablecoins are the most reliable form of money they can access without a bank.

Today, Tether remains the dominant stablecoin issuer. Yet, for over a decade since its launch, it moved money on congested, costly rails built for other purposes.

This is the gap Stable.xyz is building into.

The Accidental Dollar

Adoption of USDT has shot up since its launch in 2014. Although Tether launched it as a bridge between fiat and cryptocurrencies, people used it as a trading pair on crypto exchanges.

Few could have imagined it becoming a safe store of value.

In 2014, Venezuelans saw their local currency, bolivar, depreciate by 99%. In 2024, Argentinians faced 300% inflation. Neither wanted a digital dollar to trade on exchanges. They just wanted to hold their money with minimal friction. USDT allowed them to do that on their phones, without requiring a bank account.

Twelve years after its launch, USDT has evolved into a tool for financial inclusion. Although that’s not what its founders had initially planned.

In October 2025, Tether’s CEO, Paolo Ardoino, called Tether’s USDT “likely the biggest financial inclusion achievement in history” when it crossed 500 million users. Earlier this month, that number surpassed 550 million users across emerging markets.

The product was perfect — but there was a problem: inefficient infrastructure.

The Borrowed Rails Problem

The people in both Argentina and Venezuela were running their financial lives on blockchains that were not designed to do that.

Ethereum was built for decentralised applications. Tron was built as a decentralised platform with high throughput to enable creators to own, share, and monetise content without intermediaries. Stablecoins used these chains, but lived with frictions.

For example, if you choose to send USDT from your MetaMask wallet, you must pay a gas fee in ETH. You could hold a million dollars in USDT and still be unable to move it without a few dollars’ worth of volatile assets you didn’t want in the first place.

I also wrote about how crypto’s technical sophistication drives people away. That’s when you see 716 million global crypto owners, with less than 10% of them transacting actively every month.

Read: The Ownership Gap

What would a payroll team do if they didn’t have enough ETH to pay the gas fees? Figure out how to bridge or swap some ETH? I’d bet they’d give up and go back to moving money via SWIFT or banking channels. Maybe they are slow and annoying, but at least you know what timeline to expect.

What’s more frustrating is that the payroll team might not break a sweat to receive some stablecoins, only to be stuck with them without understanding why the payment wouldn’t go through.

The general-purpose chains have issues beyond just paying gas fees.

When a memecoin launch spikes network activity on a general-purpose chain, it forces a Nigerian freelance artist awaiting their monthly payment to compete with speculative trades for the same block.

It gets worse for the institutions. When blockchains become congested with DeFi activity, like lending and trading, the payroll has to either pay higher gas fees or wait. Businesses running vendor settlements and treasury operations can’t build their payment flows around fees that fluctuate by double-digit percentages in a single day.

A U.S. business sending $1,000 to an Indian contractor via SWIFT pays at least $50 in wire fees, intermediary charges, and FX margins. But who are we fooling if we replace these cost savings with uncertain gas fees?

Read: Making Blockchains Great Again

Then, there’s also the privacy problem.

Public blockchains are transparent by design, making them auditable and trustworthy. But the boon turns bane for businesses. Transparency of a treasury team’s wallet flows can reveal its strategy to competitors.

General-purpose blockchains like Ethereum and Solana offer higher speed and cost efficiency than traditional SWIFT payment infrastructure, but they do not provide confidentiality for sensitive information. That’s because they were never designed to solve this.

However, the demand for stablecoin infrastructure was only exploding.

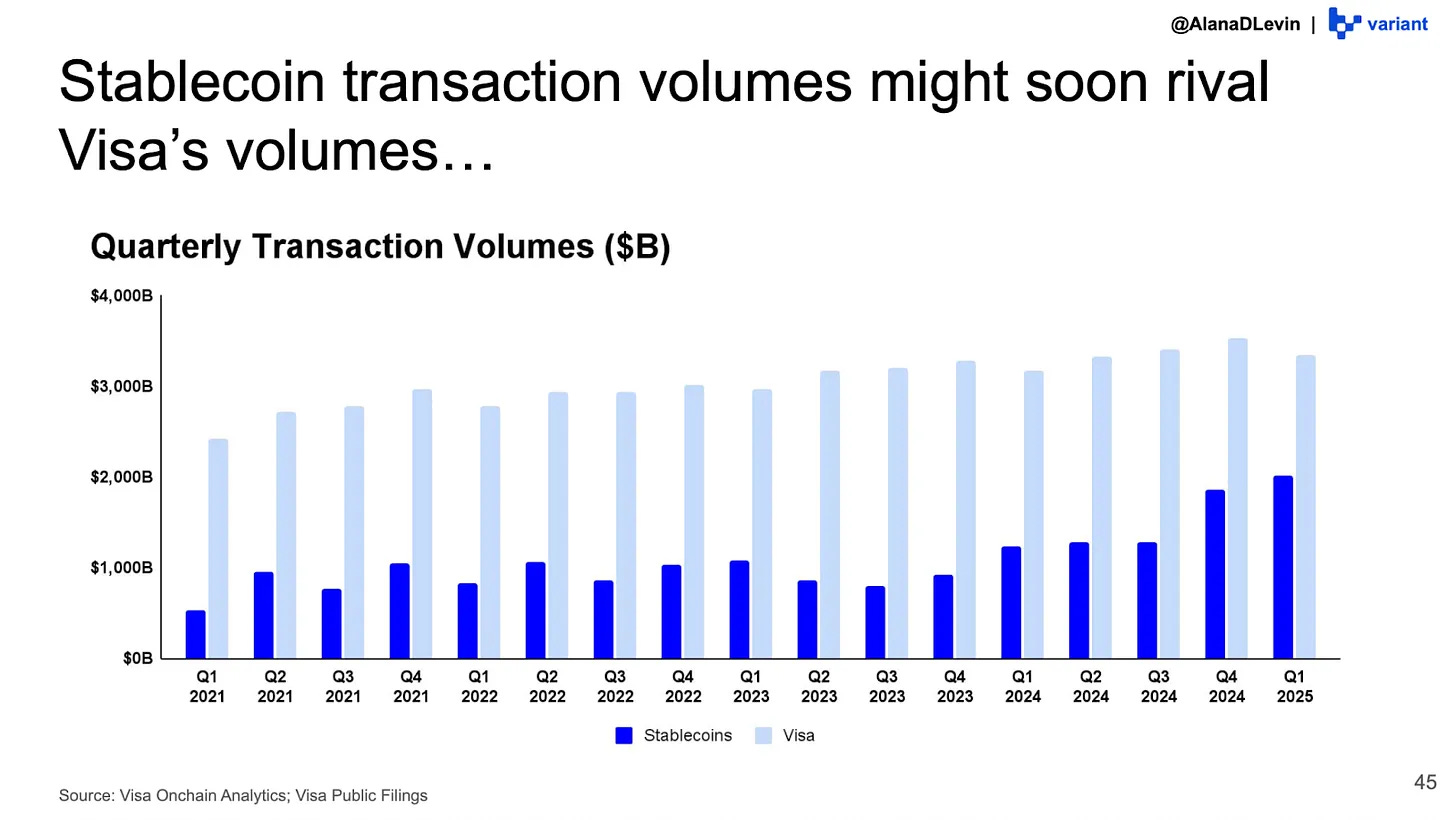

In 2025, adjusted stablecoin transaction volume reached $10.1 trillion, up 75% from the previous year. The gap with payment giant Visa is only shrinking with each quarter.

Yet, the infrastructure couldn’t keep up with the growing number of digital dollars they carried.

Need for New Rails

In the past year, a new category of blockchains has emerged specifically to facilitate stablecoin transactions.

The idea was that the masses deserved infrastructure built from the ground up if they were to adopt stablecoins as the default way to move money.

Each blockchain offers unique features.

In September 2025, Plasma launched a blockchain that enabled payments using zero-fee USDT transfers and a Bitcoin-secured foundation. It offered an open ecosystem for developers to build geo-specific financial tools on a neutral settlement infrastructure. Two weeks ago, Stripe and Paradigm-incubated Tempo launched a stablecoin-agnostic Layer-1 network to facilitate payments. This network supports any dollar token and has partnered with institutional giants like Visa and Mastercard to establish a payment standard for AI agents.

Then, there’s Stable.xyz.

Plasma supports payments across multiple stablecoins, including USDT, while Stable.xyz is building its entire chain’s economy around USDT as its foundational layer.

Stable’s payment blockchain uses USDT0, LayerZero’s omnichain version of USDT, as the native gas token. This means validators earn USDT, the treasury holds USDT, and every transaction on the chain pays fees in the same asset. The chain’s security, governance, and fee mechanics are denominated in the asset that half a billion people already use to move money. Businesses and individuals don’t need any other cryptocurrency to pay gas fees.

This architecture is designed for a specific use case, making it stand out from other payment-specific blockchains.

Plasma focuses on building a composable financial ecosystem for developers to build geographically specific applications on top of the blockchain. This is a developer-first bet on what stablecoin infrastructure should look like.

Stable, however, is solving a more foundational problem involving the payment corridor itself. It’s targeting the infrastructure that powers the $900 billion remittance market, cross-border vendor payments, and treasury operations moving millions of dollars in USDT every day.

For these transactions, users value predictability more than composability. They need infrastructure that can handle high volume without failure.

This is where Stable’s USDT Transfer Aggregator helps.

Most blockchains process transactions individually. When volume spikes, transactions can get stuck in a queue. The Aggregator solves this by bundling multiple USDT transfers into a single operation and processing them together. This reduces the per-transaction overhead.

Think of it as the difference between a highway where every vehicle pays a toll passing individually through a single lane versus a highway that allows 10 vehicles to pass through a toll booth at a time.

The aggregator saves processing overheads and cuts congestion.

The cost adds up quickly and bites hard in high remittance corridors, where peer-to-peer or retail USDT transfers occur in high volumes and with thin margins. A payment processor in a business running thousands of daily transfers cannot absorb unpredictable per-transaction costs.

In 2024, India topped the list of remittance recipients with $129 billion, followed by Mexico with $68 billion and the Philippines with $40 billion. Nigeria received about $20 billion. These four corridors collectively moved over a quarter of a trillion dollars in a year, almost entirely using infrastructure that still averages 6.5% in transfer costs.

The Aggregator makes those costs flat, predictable, and low enough to make stablecoin-based remittance competitive with incumbents in the real world.

Businesses need predictability to prefer stablecoins to traditional payment routes. Predictability not just in calculating the cost of making a payment, but also in knowing if the network is going to be as available as the traditional routes.

Stable’s guaranteed blockspace feature gives enterprises the reassurance that general-purpose chains can never provide. The feature reserves a fixed portion of every block for institutional and high-volume users, regardless of what else is happening on the chain.

The institutional support is evident from the fact that Stable has attracted backers, like Franklin Templeton, one of the largest asset managers. When a fund house that manages over $1.6 trillion is on the cap table, it speaks to their conviction in Stable’s direction.

Franklin Templeton’s involvement also includes a live $100 million tokenised U.S. Treasury position on the chain, through a consortium that includes Wellington Management and Standard Chartered.

This bet has a far-reaching impact.

Last month, we wrote about how when U.S. Treasuries move on-chain, the instruments built on top of them follow. “Lending protocols gain access to higher-quality collateral. Stablecoins get anchored to verifiable on-chain reserves rather than off-chain attestations.”

Franklin Templeton’s position on Stable shows that institutions that once managed only the assets backing stablecoins (tokenised treasury funds) are now interested in owning a share of the infrastructure that powers them.

But there are things Stable will have to watch out for.

A chain whose gas, treasury, and entire economic logic runs on USDT inherits every regulatory problem USDT carries. Tether had to shut its euro-based stablecoin, EURT, because it was not MiCA-compliant. Post-GENIUS Act, US-regulated entities face compliance questions building on a stablecoin sitting outside the federal regulatory perimeter.

Also, businesses won’t use stablecoins for payroll and vendor settlements if they require businesses to share sensitive information on general-purpose blockchains.

Stable’s privacy layer offers to solve this using zero-knowledge (ZK) cryptography, which masks the transfer value and discloses only the sender and receiver addresses. But that promise is still a work in progress.

If Stable is to become the default choice for businesses to move money, it will have to move quickly on its privacy promise.

What This Changes

People often think the digital dollar story is about crypto. I think the story is more about financial inclusion - about how one can access money as they navigate geopolitics and the economy.

Today, Tether holds over $120 billion in U.S. Treasury bills as a reserve asset, more than what most sovereign nations hold. Over half a billion people across the world’s fastest-growing economies choose to hold stablecoins because of the ease with which they can hold and transact them. Not because they are trending and part of the crypto narrative.

Such is the scale of financial inclusion USDT has enabled.

The world kept using traditional infrastructure for decades because it had no other option. Now, we see them opting to transact using stablecoins despite broken infrastructure. It tells us a thing or two about users’ belief in the digital dollar. And now, the infrastructure is catching up to the demands of the users.

There are many builders in this space trying to bridge the gap. They all have unique economic models. Stable might not be the best-funded chain, or the most technically ambitious one. But it has definitely adopted a smart approach by taking its product where users already are: to USDT. Over half a billion of them adopted the product even when it moved money over broken infrastructure.

Stable does have questions to answer and intense competitors to see off. But it’s on the right direction and counts an envious set of financial giants as its ecosystem partners.

What will guarantee success? Nobody knows for sure, but I’ll try anyway. It’s really marketing 101.

Stable needs to offer people a way to move their money without worrying about when the plumbing beneath it will crumble or which currency to hold beyond stablecoin to pay fees. People care most about the comfort of moving money. Crypto, stablecoins or fiat - it doesn’t matter. What matters, though, is how smooth that journey is.

Stable is aspiring to transform that journey into a comfortable one. Just comfortable enough to make payments an invisible, forgettable experience. Because moving money isn’t a skill to master.

That’s it for today. I will be back with another one soon.

Until then, stay curious.

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.