Hello,

You want to sell me a product? Don’t tell me about it; show me if you use it first. Amazon runs on AWS. Every product Amazon sells you is hosted on the same servers Amazon leases to its competitors. If you don’t use the product you are selling, then why would your customers?

Securitize is a company that sells tokenisation infrastructure for a living. Its business is to convince public companies, private funds and asset managers to put their securities on a blockchain. And what better way to convince the world to put their shares on the blockchain than by putting its own stocks on the chain? So it did that.

On July 2, 2026, Securitise co-founder and CEO Carlos Domingo rang the opening bell at the NYSE to mark the company’s public debut. The same morning, the same stock was also available as a token on Solana and Avalanche. It wasn’t in a wrapper format but rather a share whose ownership was recorded on a blockchain, not a centralised register. Roughly $270 million of common stock was held on-chain on Day 1.

Tokenising your own stock at listing invites regulatory scrutiny that most newly public companies prefer to avoid. Securitize chose the scrutiny.

This begets a bigger question. If a company can launch the tokenised equivalent of its share on its public debut, then what stops a private company from doing the same for its Series A fundraise?

In today’s piece, I explore how tokenised stocks fundamentally change what VCs offer private companies in a packaged term sheet.

On to the story…

What’s in a Term Sheet?

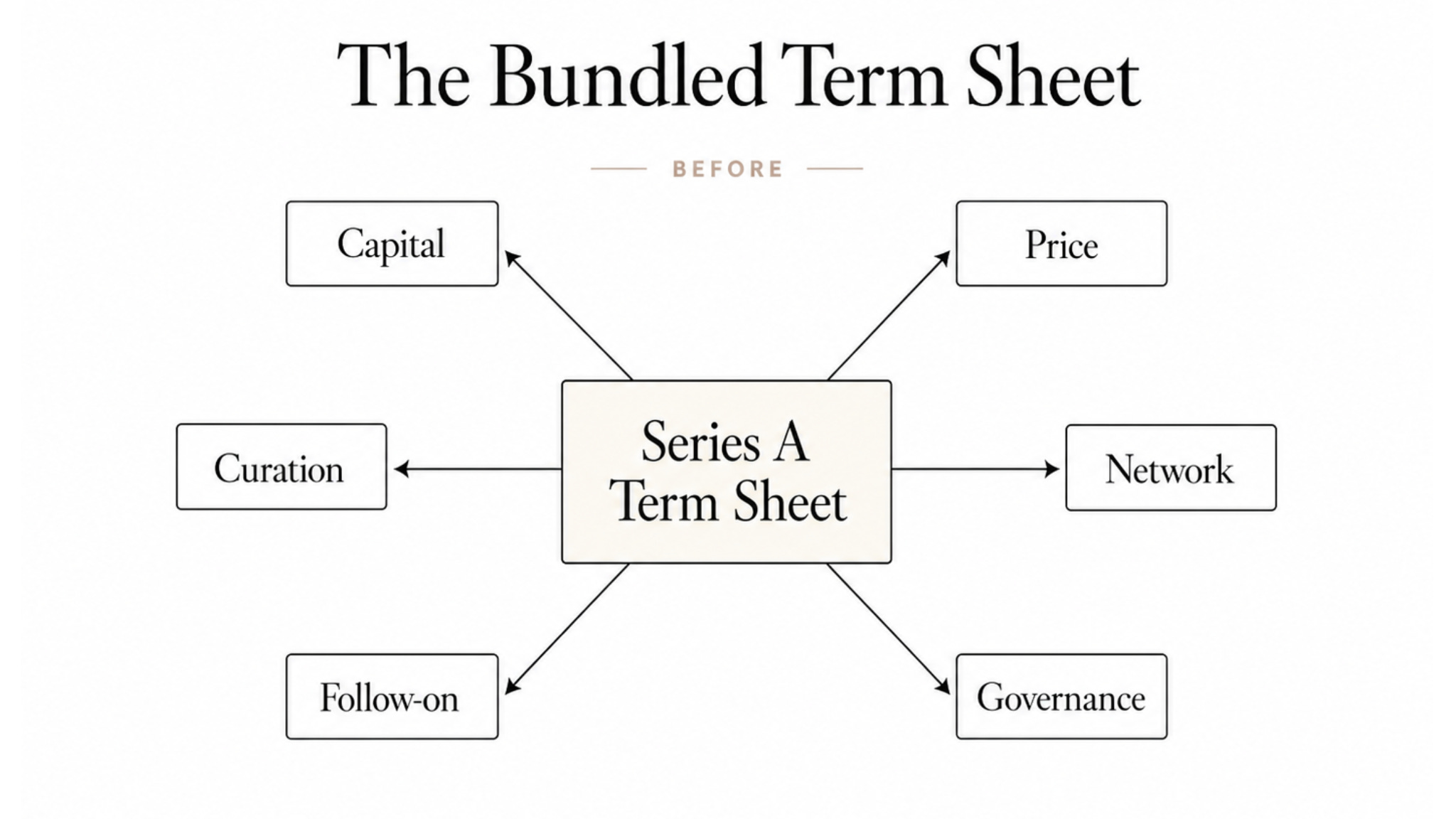

Founders don’t go to venture capitalists (VCs) only for money. Whenever a VC signs a term sheet, they agree to deliver a bundle of services.

First, there is a commitment of capital. The VC agrees to fund the company with the required capital to scale from 0 to 1.

Second, there is a price. Every private company needs a valuation. In private markets, the valuer is usually the lead investor.

Third is curation. A respected name on the cap table tells the world that this company was worth backing. It helps the company attract other investors, customers, and good talent. The VC also helps the company in networking by introducing enterprise clients, senior engineers and the “who’s who” of their industry.

Sometimes the VC also commits to a follow-on round. This is an implicit promise to keep writing more cheques as the company grows.

Lastly, and most importantly, a term sheet also includes a governance clause. As part of the deal, the VCs typically take a board seat, information rights, protective provisions, and the power to set transfer restrictions.

This is the bundled product that the VC sells to the company as part of a fundraising round.

The bundle was untouched all this time because private shares were locked out from the general public. As an individual investor, you couldn’t buy or price them without the company’s cooperation.

A few weeks back, I explained how the walls around private-market pricing were being gradually pulled down.

Read: Pricing the Private

Last month, I wrote about how blockchain infrastructure unbundled banks’ role in underwriting a company’s IPO. The same infrastructure for tokenised stocks now shows that VCs no longer hold a monopoly on pricing private companies.

There’s one catch, though.

Securitize tokenised its stock, SECZ, at a time when the company is already a decade-old business with audited financials, disclosed cash flows and over $4 billion in tokenised assets across its platform. A market can price it because there is enough material to base its valuation on. For a Series-A startup, the market has only a founder’s story, reputation, and a hypothesis to work with. Although equity is the common denominator in both cases, the underlying factors that drive valuation differ.

This is where the curation aspect comes into play on a term sheet. A VC at Series A lends more than a name to the cap table. They underwrite a business for which there’s not enough public data. Late-stage pre-IPO companies like SpaceX and OpenAI are easier to tokenise because they already behave like public companies. Their prices show up on secondary marketplaces, in tender offers, on perp contracts and in analyst notes long before they get listed on public markets.

However, early-stage tokenisation is tricky because the market has less data to base its pricing on. Yet this doesn’t stop the rest of the bundle from coming apart.

The Unbundling

Securitize was not the first American company to put its own listed stock on a blockchain. Exodus did that on Algorand in 2021. Digital asset and data centre company Galaxy Digital has also put a version of its equity on the blockchain. Securitize did it one better by becoming the first company to do it on Day 1 of being public.

Token trading on Solana and Avalanche is legally the same as stock trading on the NYSE. Each token carries the same voting rights, dividends and claim on the company. It is not a synthetic contract tracking a price or an offshore special purpose vehicle (SPV) holding a share on your behalf.

The tokenised shares of Securitize are as good as the off-chain common equity stock, SECZ, itself.

Investors are usually concerned about the nature of ownership associated with these tokenised versions of stock. Vaidik’s Who Actually Owns Your Stocks? walked through the different kinds of “tokenised stock” the market currently sells. Issuer-backed, like SECZ and Exodus, where the token is the share. Custodial wrappers, like xStocks or Robinhood’s stock tokens, are SPVs that hold a real share and issue you a claim on it. Only the first kind carries the rights a shareholder would recognise. That is what the entire thesis of a VC is built on.

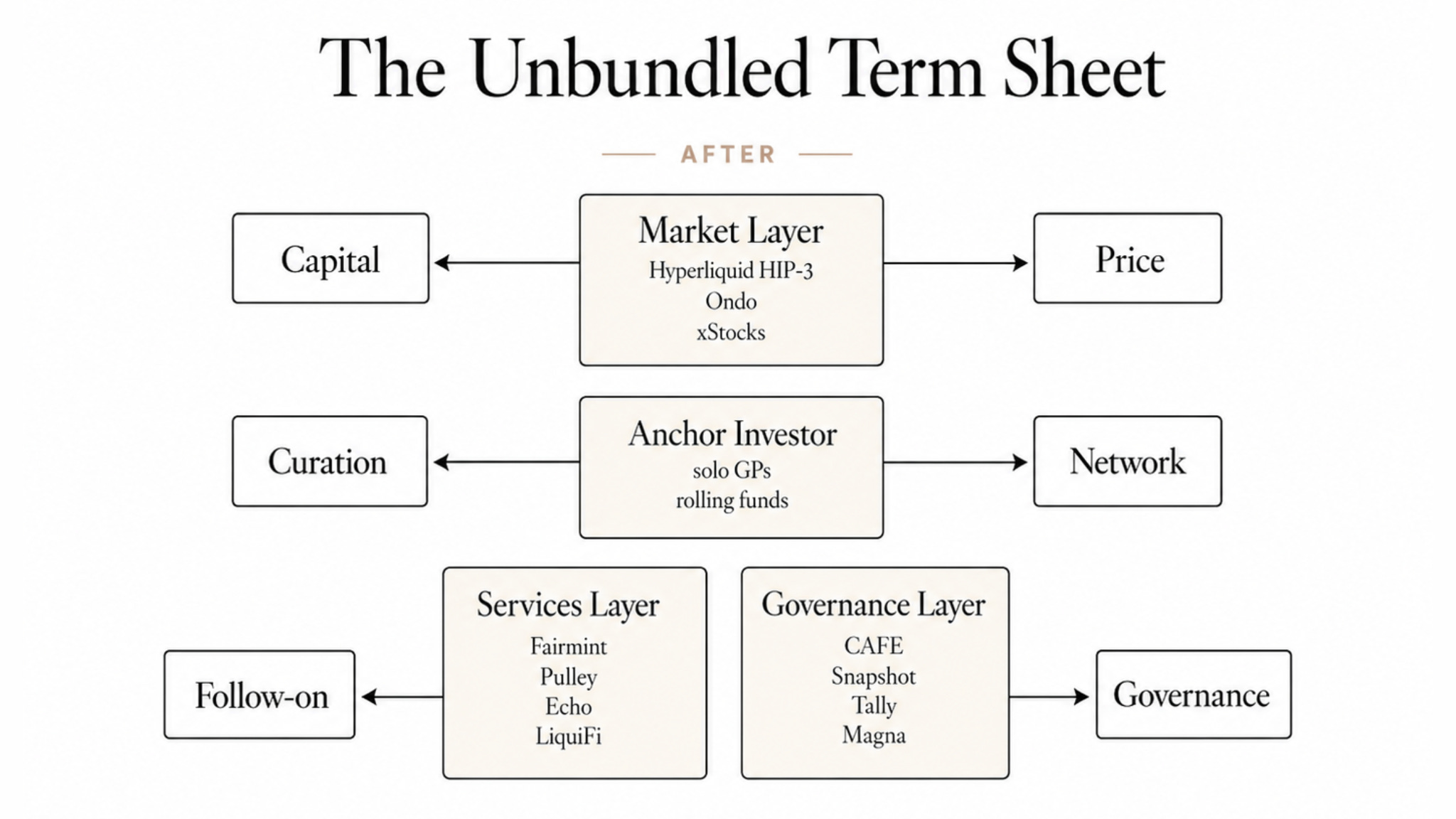

Once the shares themselves become continuously priced and easily transferable, the bundled jobs of a term sheet no longer need to come bundled. The other jobs start finding cheaper, better routes.

Capital and Price start collapsing into a market layer, at least for companies that are mature enough to be priced. The market sets the price, and capital follows it. As of now, Ondo’s Global Markets has surpassed $1 billion in tokenised equity TVL. On Hyperliquid, a pre-IPO perpetual on Cerebras priced within 1.3% of the chipmaker’s eventual Nasdaq opening print.

The curation and network roles still remain with an anchor investor. But the anchor investor no longer needs the institutional machinery of a Sequoia or a16z. Elad Gil raised a solo vehicle of roughly $1.5 billion. The lead cheque and the reputation attached to it can now be delivered by one person and a rolling fund.

Services move to specialists. Fairmint and Pulley for cap tables. Coinbase bought LiquiFi for token vesting in July 2025. Echo, acquired by Coinbase in October 2025, handles fundraising. Magna and Sablier handle vesting streams. A founder in 2026 can assemble the platform team that a venture firm used to sell as part of a bundled deal.

Governance becomes programmable. Fairmint’s structure enables a rolling, SAFE (Simple Agreement for Future Equity)-style raise that converts on its own terms. Vesting cliffs are enforced by smart contracts rather than lawyers.

Secondary liquidity, the ability for insiders and early investors to sell their stake, is growing. Employees and angels at tokenised private companies now have exit routes without waiting for an IPO.

That is what continuous liquidity via tokenised stock trading enables. Continuous liquidity changes what equity means to a founder and an employee. When shares can be sold any day, the equation around vesting cliffs and cash-out windows shifts. An employee who used to wait four years for a tender offer now has a live market to go to. It does have some trade-offs, though. Crypto has already seen this play out with layer-2 tokens like Arbitrum’s ARB and Optimism’s OP, where teams received tokens that traded from day one. Employees dumped them at cliff dates. Token prices decoupled from underlying network activity. Founders spent as much time watching charts as building products.

This is not a perfect example because ARB and OP are governance tokens and not equity, and their prices reflect network usage more than corporate performance. But the incentive problem is similar. Legal restrictions like Reg D 506(c) accredited-investor gating, Rule 144 seasoning, and multi-year lockups slow it down but do not eliminate it. Tokenised equity provides practical exit routes for insiders and opens the door to exit patterns that private markets have historically had time to smooth out.

Even the follow-on cheque, the piece of the bundle that most founders value most, is the last one waiting for a tokenised replacement.

That’s because every regulatory framework announced so far, including the SEC-approved Depository Trust Company pilot, Nasdaq’s tokenised trading, and DTCC’s October launch, is around already-public Russell 1000 shares. None of them accommodates a Series A startup’s tokenised equity trading on their venues today.

What Stays with the VC

When music streaming took the world by storm, it commoditised distribution but did not kill record labels altogether. Anyone can put a song on Spotify. What was not commoditised was the Artists and Repertoire (A&R) division, still deciding which artists were worth betting on, building brands around them, and opening doors that data alone could not open. The labels that survived the transformation became data-driven talent scouts. The bundle they used to sell split into specialists, and the labels held on to the part that was still scarce.

Venture capital will likely go the same way. Tokenised stocks are taking over the parts of the term sheet that were about mechanics, like recording ownership, discovering a price, moving a share from one wallet to another, and releasing a vesting tranche on schedule. Blockchains are better at mechanics than a term sheet can ever be.

What stays scarce is the person whose name on a term sheet convinces the next round to happen, an enterprise buyer to switch vendors, or a senior engineer to leave Google and join a startup. Tokenisation cannot underwrite a founder.

But every unbundling invites a rebundling, often controlled by new owners. The London Big Bang of 1986 broke apart the city’s brokers and jobbers. Within a decade, universal banks had absorbed the pieces.

For decades, founders walked into a VC’s office because it was the only place where they got access to capital, pricing, curation, and governance in one place. Tokenised stocks are like a hallway with multiple doors. One gives the founder access to capital, another gives them pricing, and another addresses governance. The founder still needs all of them, but no longer from the same person.

That also fundamentally changes the questions a founder asks at the start of their company’s journey. The founder will no longer be forced to think in terms of the one fund they would want on their cap table to solve all their problems. It gives them the freedom to choose which layers of their company they want the market to run and which they’d rather bet on a human to run.

The mechanics in a term sheet are the first to get tokenised because that is what markets can adopt well. Judgment gets tokenised last, or probably never, because it is what markets need someone else to provide. A Series A startup will eventually put its shares on a chain, but will still need someone to decide if the shares are worth putting there.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.