Making Capital Reallocate Faster

Crypto offers superior transparency and tools for repricing assets

Hello,

The job of any financial market is to move capital out of declining businesses and into those likely to do well. Every other function in the market, including trading, wrapper products, and research, exists to serve that one job. The faster a market does this job, the more efficient it is considered.

For most of financial history, capital movement has been slow for numerous reasons. Investors could have enough information to know that a business was in trouble, but they had to wait for proof. They often had to wait to see quarterly earnings, guidance cuts, and analyst notes before they moved their capital.

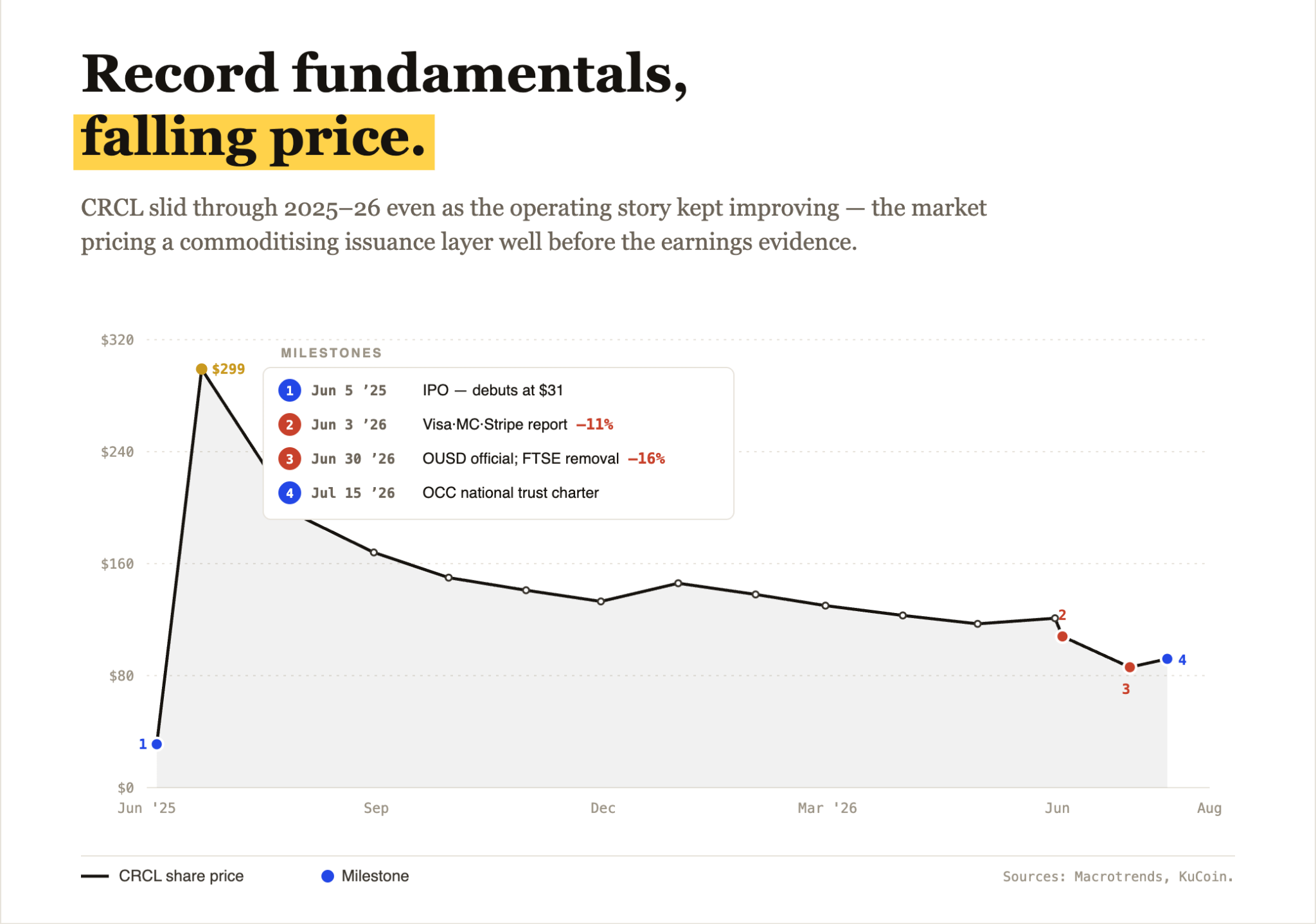

On June 30, Circle’s stock fell 16%, its worst day since listing. Nothing had changed in Circle’s business. In fact, that same month, USDC settled a record $1.21 trillion in transactions. The cause was a press release from a consortium of 140 firms announcing a rival stablecoin. Just an announcement of a nonexistent digital dollar. Yet capital moved.

In today’s piece, I will explore how crypto rails have compressed the time between information and capital movement, and why this tells us about crypto’s maturity into fintech.

On to the story…

Waiting for the Proof

In 2000, financial economist Jeffrey Wurgler measured how quickly capital moved into growing industries and out of declining ones across 65 countries. Jeffrey’s research found that the speed at which financial markets moved capital distinguished developed markets from undeveloped ones.

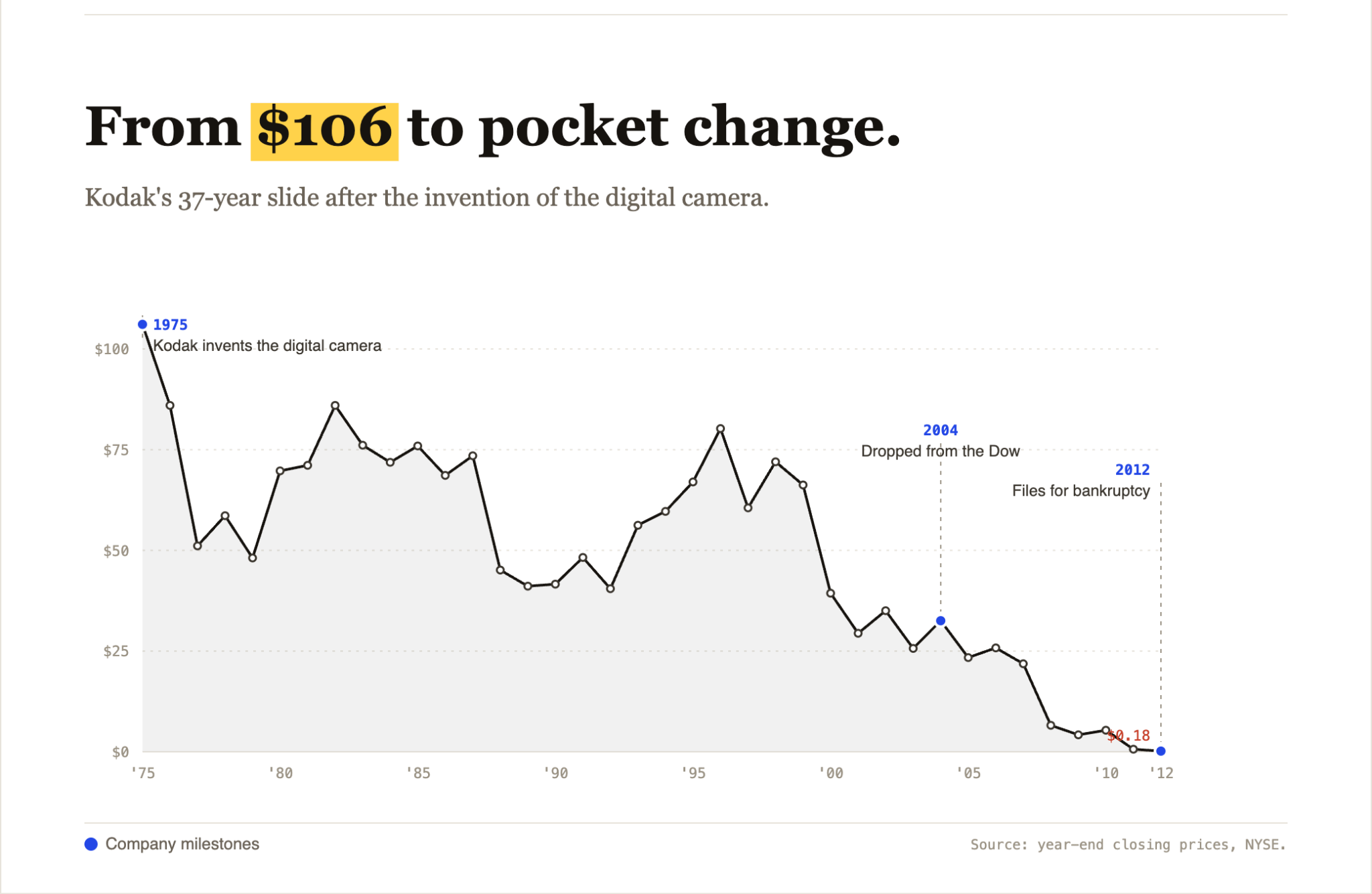

The speed with which you can move capital in traditional markets has seen extremes across the spectrum. In 1975, Kodak’s own engineer built the first digital camera. The market took another 25 years to punish the stock considerably. The price fell from a peak of $100+ in 1975 to under $40 in 2000. It then moved to zero only in 2012, when it filed for bankruptcy.

Phonemaker BlackBerry’s market share also grew for two full years after the iPhone launched, from 9.6% in 2007 to nearly 20% in 2009. Although everyone had seen the iPhone, the market still waited for BlackBerry’s revenue to slip.

The traditional world has even seen the other extreme. When the CEO of US educational services provider Chegg admitted on a May 2023 earnings call that ChatGPT was hurting new customer growth, the stock fell 47% on that day. Chegg’s revenue at that point was down just ~6-7%.

So, the difference between old and new markets is not the willingness to act early. Markets have always tried to price the future if they had enough information.

Chegg’s investors needed the company’s CEO to confirm the extent of the damage during a scheduled call before they could pull their money out. In the smartphone market, investors waited for signs that the iPhone was taking over from its competitors before acting. The market moved only after the signal became credible. For a long time, information availability has been a bottleneck in traditional markets. In the case of public companies, the information was made available when the company chose to share press releases or four times a year during their quarterly earnings. Private competitors reported nothing at all. Analysts would downgrade a company much later.

Crypto removes this bottleneck.

Eliminating the Bottleneck

Every protocol’s revenue, fees, deposits, and user flows are recorded on a public ledger and updated in real time. Nobody has to wait for an earnings call to know how much money a business makes. Anyone with a Dune dashboard or a DeFiLlama tab can see it in the frequency with which these platforms update their datasets. When a layer commoditises and a new player launches something in the adjacent layer expected to accrue more value, the revenue at stake for the incumbent is clearly visible on dashboards.

Over the past three months, my colleagues and I have written about layer after layer of this industry turning into a commodity. Stablecoin issuance, lending infrastructure, blockchains themselves. Each layer is getting attacked by cheaper, modular alternatives, and value keeps migrating to whichever layer stays scarce. That means the repricing trigger and a credible competitor showing up at an existing layer happen every few weeks.

Read: From Issuance to Infrastructure

In such environments, capital can move on the announcement because investors can immediately do the math on the revenue and market share at stake, without waiting for any analyst reports or earnings.

Take Circle for instance.

On June 3, CRCL’s share price fell 11% when reports of a Visa-Mastercard-Stripe stablecoin partnership first surfaced. On June 30, when the 140-firm consortium made OUSD official, it fell 16%. To be fair, another factor could also have driven the fall. FTSE Russell removed Circle from its growth indices on the same day, forcing index funds to sell. But the direction for Circle was apparent almost a month before the index exclusion was announced. Anyone could see what OUSD was attacking. Reserve income accounted for 99% of Circle’s revenue in 2024, and the consortium’s pitch was to return nearly all of that yield to its partners. The market did not need to wait for a single dollar to leave USDC.

A week later, Circle won approval for a national trust bank charter, signalling an improving operating story. But the issuance layer is commoditising, and the capital parked in CRCL will not wait for earnings to move elsewhere.

Transparency of information is just one half of what contributes to faster capital reallocation in crypto. The other half is the tools that make taking an action possible after having access to information.

This is where crypto’s market structure does what traditional markets cannot.

Think about what it takes to express a new opinion in traditional finance. If you hold a mutual fund and change your mind, you redeem at the end-of-day NAV and wait for the cash to settle. If you hold an ETF, you can sell intraday, but only during the six-and-a-half hours the exchange is open, five days a week. If your thesis involves a private company, there is often no instrument at all. You wait for a funding round or a tender offer. And if you are a limited partner in a venture fund, your capital is locked for ten years. You can change your mind, but good luck with moving your money.

Every one of these frictions delays repricing. Even though investors have new information that could convince them otherwise, the infrastructure prevents the free reallocation of capital.

Crypto markets run around the clock, so no opinion has to wait for an opening bell. Settlement is near-instant, so capital that exits one thesis is available for the next one within minutes. And the industry keeps building new instruments to express increasingly specific views.

Spot markets let you back a protocol. Perps let you hold a leveraged short or long position in any traditional or crypto asset or commodity, like gold or oil, without owning the underlying assets. Prediction markets let you price an event, like whether a stablecoin bill passes, separately from pricing the companies affected by it.

Hyperliquid’s permissionless markets have processed around $270 billion since last October, with 99% of that in non-crypto assets. When crude oil moved on Middle East headlines one weekend, Hyperliquid’s perps had priced most of the move before CME even reopened.

Read: Every Exchange Is an ‘Everything Exchange’

Put transparent information together with instruments that let anyone act on it immediately, and you get repricing capabilities that traditional markets can never offer.

Earlier this month, Robinhood made Lighter its in-app perpetuals engine and put $11 million of LIT in front of its 28 million funded accounts. Immediately, the market moved significant capital into the new entrant’s ecosystem.

LIT rose 50% in two weeks simply because investors reviewed a distribution deal and decided to reallocate capital.

Read: Building a Financial Supermarket

This changes the job of everyone allocating capital.

I feel this discipline travels beyond liquid markets. Private valuations famously lag public repricing by quarters, which is how venture funds carried their 2021 valuations deep into 2022. But using crypto infrastructure, liquid markets can also mark illiquid markets in real time.

Read: The Unbundled Term Sheet

The Commoditisation Era

Commoditisation has been the operating condition of every industry. Every few months or years, especially in a maturing industry like crypto, we see various incumbent layers get commoditised due to the concentration of competitors around a single stack within an ecosystem. As competition increases, that layer becomes less valuable, and value shifts to adjacent layers with fewer competitors. The competition then migrates to that new layer. This is what has been happening for years, and this is how industries evolve.

We saw it with open-source software, and now we’re seeing it happen in crypto. Stablecoin issuance, lending infrastructure, exchange venues, and the blockchains themselves - we have covered each of these layers in the past three months. We wrote about how they are being targeted by a cheaper, modular alternative, and every incumbent margin is being eaten away by others. In an industry built on open-source code and permissionless entry, no layer stays scarce for long.

A market where the playground and the reward are migrating often from one layer to another also needs to enable faster and more frequent capital movement between those layers. You cannot penalise the investors for wanting to reallocate capital, lest they move to more efficient and freer markets. The transparency and instruments that blockchains enable allow this precise movement with little to no friction.

This is why I agree with Jeffrey Wurgler’s yardstick to measure a developed market - one that enables its constituents to quickly pull money out of the declining industries and reallocate it into the growing ones. By that measure, this is the most developed capital market ever built.

While equity markets also enable quick reallocation of capital, as we saw in Chegg’s case, the difference between traditional markets and crypto lies in what follows. Crypto compresses the entire process of rotating funds into a single sitting.

The investor who sold CRCL on June 30 could have done so using the equity in the traditional markets. But that could have been done only during market hours. The same investor could also have expressed their opinion on Circle by trading its perpetual contract on Hyperliquid or by betting against the company using an event contract on a prediction market. Both these options are always on and wouldn’t have required the investor to wait for the market to open.

This is not to say that crypto investors will always get their quicker reallocation decisions right. High speed could mean more mistakes. But I’d gladly welcome the ability to make quicker decisions with better information and be occasionally wrong, rather than being shut off from the information flow and being late to decision-making due to market frictions.

Read: Netting Is the Moat

I don’t think there’s a greater liberation for investors in a free market than being empowered to access important information at any time and act on it using the right tools at their disposal.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.